I always wondered if this day would come, but here we are. This will be my final post on this blog.

Don’t worry, I am not leaving Japan or retiring. I’ve been fortunate to join Leo Wealth, initially to support their Japan expansion and, in time, to help build out their wealth management business here, subject to the appropriate regulatory approvals.

My relationship with Leo Wealth goes back a long way. I first met founder Jessica Cutrera in 2003, and we worked together for several years. In all my time in this industry, I have never met anyone with a higher level of skill, integrity, and commitment to serving clients. When she asked me to join the firm, I was delighted to accept.

Leo already operates a successful wealth management, tax planning, and investment business in Hong Kong and the US, alongside a highly regarded tax compliance and consulting practice in Japan. Work is now underway to expand the wealth business into Japan, with plans to apply for Discretionary Investment Management and Investment Advisory licenses with the Kanto Finance Bureau in the coming months.

Many wealth managers claim independence. However, Leo is a true fiduciary, meaning we sit firmly on the side of our clients. Please visit the website to learn more about what we do.

I have been writing here for 9 years. What started as simple financial planning tips gradually evolved into my (occasionally over-opinionated) views on markets, investments, asset allocation, crypto, and much more. Thank you to everyone who has read, guest posted, and engaged over the years, and a special shout-out to those who joined the meetups along the way.

If you would like to keep up with my work, I’ll now be contributing to Leo Wealth’s Insights page, alongside a highly experienced team of professionals. The depth of expertise within the firm has genuinely impressed me, and I’d encourage you to bookmark the page and follow along.

As a starting point, here are two excellent Japan tax articles from my Tokyo-based colleague Thomas Lu:

Leo Wealth combines deep expertise with a genuinely approachable team, so please don’t hesitate to get in touch if you have questions or would like to start a conversation. I will also continue my coaching work under the Leo banner, and we are already helping clients in areas that don’t require regulatory approval while our licenses are being put in place.

You can reach me at: martin.phillips@leowealth.global

Finally, thank you again for reading over the years. If our paths cross, the drinks are on me.

I haven’t had much to say on markets for a while. We clearly entered the dumbest timeline, and no amount of TACO is likely to pull us back out of it.

Speaking of tacos, and to keep this post light, my friend recently introduced me to Taco Fanatico. We went to the Shibuya branch – there’s another in Naka-Meguro and even one in Nagoya. Cold beer and tacos definitely beat trying to trade this market…

If I’m not mistaken, said market is almost entirely driven by Trump’s social media posts rather than actual events. And, once more, I could be wrong, but the great dealmaker appears to be negotiating with himself. The Iranians have probably read the Chris Voss book. Trump doesn’t strike me as much of a reader…

You have probably had enough armchair geopolitics, so I won’t add to the discourse. Here’s BlackRock Chairman Larry Fink with two extreme scenarios:

“GLOBAL RECESSION”

The man who manages $11 trillion just warned the world what’s going to happen if Trump doesn’t make a DEAL, now.

A total wipeout.

Larry Fink, CEO of BlackRock, the largest asset manager in human history explains to the BBC how that occurs 👇🏼 pic.twitter.com/HqYrOhwj8x

In short, either the war ends, and things go “back to normal”, and markets revert to being insane in a good way. Or we get $150 oil for an extended period and a global recession.

Hope for the best and plan for the worst. Short-term investors would want to be defensively positioned. Long-term investors can, and probably will have to, endure some pain. A globally diversified portfolio, perhaps with satellite holdings in hard assets, is not going to be a cake walk, but you don’t have to look at it every day.

I think I summed up my views on how to plan effectively in noisy markets in my Back to basics post.

Asian economies in particular are in a precarious position. Japan is better prepared than some other countries, although the prospect of higher inflation, low growth and a floundering yen is not exactly mouthwatering.

That said, the Japanese stock market still has a lot going for it, and the opportunity is nicely summed up here:

I may also be biased, but with many people trapped in yen, the investment options are not too shabby.

I’ve been buying some stocks on the heavy red days, but am exercising caution. I even bought a little Bitcoin, despite the nagging feeling that lower prices await.

Be careful out there. It’s a great time to touch grass, admire the sakura and eat tacos.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I don’t cover property so much on this site, so today I’m happy to introduce a guest post from Jin’s Homes, a boutique real estate firm focused on the execution of short-term rental investments in Tokyo. The firm is led by Yoshihiro Jinzaki (“Jin”, Founder & CEO). Born and raised in Japan in an international environment, Jin is a native English speaker with a global mindset and a practical understanding of Japanese social norms, local expectations, and regulatory realities.

I met Jin at an event recently and had a really good chat with him. He’s friendly, engaging and is the perfect guide to Tokyo’s short-term rental market. I hope you enjoy this post:

Most professionals and investors in Japan consider property investment at some point – and then hesitate.

Financing conditions for investment properties are typically stricter than for primary residences. Compared to using a residential mortgage, investment loans often require higher equity and carry less favorable terms. At the same time, yields in Tokyo appear relatively low.

As a result, investors frequently look toward suburban areas in search of higher ROI.

But suburban investments come with their own concerns:

Will occupancy remain stable?

Will the asset hold its value long term?

Will resale liquidity be strong enough?

Faced with this trade-off, many potential investors ultimately decide not to invest at all.

A Different Approach: Short-Term Rental

One strategy that has gained increasing attention is licensed short-term rental (commonly known as minpaku).

A short-term rental operated by Jin’s Homes

In Tokyo’s main residential and commuter areas – including both central wards and well-connected cities within the Greater Tokyo area – properly structured short-term rental properties can meaningfully outperform traditional long-term leases in net income terms – often in the range of 1.5–2x when structured correctly.

Because of this income profile, short-term rental has attracted attention not only from domestic investors but also overseas non-residents whose only option is to purchase in cash.

The appeal is straightforward: enhanced income potential within areas that still maintain strong asset stability.

A Tailwind: Tourism as a National Priority

Tourism is one of Japan’s strategic growth industries. The government continues to actively promote inbound travel, and international visitor numbers have reached record highs.

At the same time, developing large-scale hotels in major cities is capital-intensive and increasingly difficult due to land constraints and rising construction costs.

In that context, small-scale licensed accommodations – when compliant and professionally managed – play a complementary role in meeting demand.

A short-term rental operated by Jin’s Homes

This does not mean every property is suitable.

But it does suggest that well-positioned short-term rental assets are operating within a structurally supported market.

The Real Concerns

Of course, short-term rental is not without challenges.

Investors typically worry about three things:

Can the property obtain the necessary licenses?

Will the projected returns actually materialize – and allow the capital invested to be recovered as expected?

Can the operation maintain good relationships with neighbors and remain stable long term?

In Japan, licensing requires coordination between multiple authorities – including the public health center, fire department, and building department. Each has its own standards, and approval must be obtained from all.

For those whose first language is not Japanese, navigating this process can be particularly complex.

Even after licensing, sustainable income depends heavily on professional setup, compliance discipline, and operational management. Poorly managed properties can damage both returns and community relationships.

Short-term rental is not simply about listing a property online.

It requires clear planning before purchase and disciplined management after launch.

A Turnkey Approach for Foreign Investors

For investors who prefer not to navigate the system alone, Jin’s Homes offers an integrated approach tailored to international clients.

Jin’s Homes works specifically with international investors, handling:

• Narrowing down viable property options based on licensing feasibility and projected profitability

• Pre-purchase regulatory consultation to reconfirm approval potential

• Bilingual brokerage and transaction support

• End-to-end project management covering permit acquisition, design, and launch

• Direct operational management and proactive neighborhood relationship building

We operate under a structured management framework designed to cover the full lifecycle of a short-term rental investment – from compliance to daily operations – allowing investors to remain focused on strategy rather than execution.

Since launch, every guest stay has been rated five stars – a measurable indicator of operational consistency.

Why Structure Matters

The difference between an average short-term rental and a strong, sustainable one often comes down to:

Selecting the right property from the beginning

Verifying licensing feasibility before purchase

Designing for the target guest demographic

Maintaining proactive communication with neighbors

Managing operations with professional standards

When these elements align, the income profile of Tokyo real estate can shift meaningfully – while still preserving the underlying stability of the asset.

If you are exploring whether this approach could fit into your broader property strategy, an initial feasibility discussion may help clarify what is realistically achievable before capital is committed.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

AI has been the relentless driver of markets for several years now. Over the last few weeks, however, the tone has changed, and investors are dumping stocks in companies that may be at risk from AI tools. “Shoot first and ask questions later” is how analysts describe the action.

What is happening?

The AI scare trade is the rapid repricing of companies based on the perceived risk that generative AI will destroy their business model.

The narrative has shifted noticeably from AI as a productivity driver to AI as ruthless disruptor of whole swathes of the corporate landscape. First, it was software companies, then payments. Now, consulting and even cybersecurity are apparently on the brink of obsolescence.

Much of this is clearly overdone. And some of it probably isn’t. The job now seems to be to identify which services are genuinely under threat and which are merely suffering collateral damage. IBM shares plunged -13% on 24 February after Anthropic said its Claude Code tool could modernise Cobol, an old programming language running on IBM machines. So, is IBM done now?

IGV (the iShares software ETF) is down almost -20% in the last month. In Japan, Sansan Inc (4443) is down -36% over the same period. Are these stocks falling because earnings will collapse? Or because multiples are contracting due to uncertainty?

I think it’s important to read this stuff because, whether it’s big or not, something is definitely happening.

The Citrini article in particular struck a nerve. It was deliberately positioned as a possible scenario, rather than a prediction. The people writing it off as doomerism are probably more afraid than they will admit. What makes the AI scare trade different from past sector rotations is that many investors feel personally exposed. When the technology threatens your own profession, the fear feels more real.

And the market hates the uncertainty.

How to position

So how should we, as investors, navigate these uncharted waters? Shooting first and asking questions later is probably not a smart approach. I don’t necessarily have the answers, but here are a few thoughts:

If you are in the accumulation phase and mostly averaging into index funds and passive ETFs, there is no need to make any big changes. The indices themselves do a good job of allocating more cash to the winners than the losers. A few software companies may drop out of the S&P 500 over time, but they will be replaced by growing companies.

For more active investors, particularly those who like to pick stocks, it’s a good idea to separate out the genuine risks and opportunities:

Direct displacement risk – code generation, content creation (ouch!), basic legal/admin work

Margin compression risk – services that become cheaper, but not obsolete

AI beneficiaries – infrastructure, energy, chips, data centres, automation

It’s productive to focus on number 3, I think. If AI makes software 10x cheaper, demand for compute, electricity and physical infrastructure likely rises rather than falls.

In the chaos of the last few weeks, I heard about logistics stocks selling off. These are exactly the kind of companies that are likely to incorporate AI and deploy it to streamline processes and boost efficiency.

I saw a client last week whose company does commissioning for data centres. They are the guys who go in and check that everything works before the operation begins. They are jammed with work and can barely keep up.

Where is the power going to come from to run these places? What infrastructure needs to be built? Who makes the wiring, and where do the raw materials come from?

What stocks have been oversold, but clearly are not going away? Meta, Microsoft and Amazon have all weakened on concerns about their massive AI capex. Is the concern justified, or is this just another buy-the-dip opportunity? It’s not the first time these companies’ heavy investment has been called into question, but look at their long-term performance.

That’s the Crowdstrike CEO, by the way. He might be sweating the stock price a bit, but surely we’re a long way off from vibe-coding cybersecurity platforms.

As always, diversification is the name of the game for large sums of money.

In many ways, the AI scare trade reminds me of last year’s Sell America trade. It was a thing for a while, but then the panic died down.

Stay curious, keep reading, and don’t get too bearish.

It’s one thing to outline extreme scenarios. It’s quite another to position your entire portfolio around them.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

So, the Bitcoin 4-year cycle is alive and well. Who’d have thought it? I asked ChatGPT how to say “I told you so” without being annoying, and it just laughed at me.

I did tell you so, though…

I wrote my last Bitcoin is dead post on June 6 2022. FTX hadn’t even happened by that point. If you are thinking of jumping in to buy the dip today, let that be a warning.

Everything you need to know is in that post.

The typical drawdown from the peak is 80%. That would take us to around $25,000. The people who spent 2025 saying the 4-year cycle is dead, and the bull market is just starting, were trying to pick a bottom at $72k yesterday. Now they’re staring at $62k. It’s only February, and the fear-and-greed index is at 9!

So, don’t expect a V-shaped recovery next month.

I don’t know if we see $25k, but I reckon we see low $40s. That’s a good spot to start accumulating. Of course, those kinds of prices could blow something up, and then we really would visit Goblin Town.

Those who know will hold their nose and load up. For most people, buying the deadest asset in the world will seem entirely too dumb. First, you get price-based capitulation. Then you get time-based capitulation. It will probably take a good chunk of 2027 before we start looking bullish again.

I don’t make the rules.

Japan’s crypto tax doesn’t change until next year. Not many people will be in profit by then! Adjusted for stock splits, my average Metaplanet entry price in 2024 was ¥55. I might get interested again in a few months.

Let’s keep this one short. There isn’t much more to say. If you felt like you missed Bitcoin, here’s another opportunity. Every single talking head will tell you you’re an idiot for buying it this year. You have to turn those voices into beautiful music. Or be brave. Or whatever it takes.

Accumulate responsibly. Never allow yourself to become a forced seller. Buy low and sell high.

See you on the other side.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Well, that’s month one of 2026 done. We’ve seen stocks near record highs, the yen up and down, metals explode upwards and then hit the ceiling hard, crypto confirm a bear market, Trump & Co. lecture the WEF, and so much more. Remember Greenland? What happened to that? How about Venezuela? The Maduro raid was only a month ago!

It’s pretty much impossible to make responsible financial planning decisions day to day without a solid framework. There is simply too much noise. I realise I am part of the problem, as I try to write content that is current and engaging. So, perhaps it’s time to take a step back and review the basics.

You’ve probably heard all this before. If you read this blog regularly, you most certainly have come across this information multiple times. Sometimes you just have to put in the reps, so bear with me.

Protect yourself and your family

Start with a solid foundation, so you can handle the typical curveballs that life throws at you without having to cancel plans and unwind investments.

Pay off high-interest debt – get rid of that credit card debt asap

Emergency cash reserve – 3 to 6 months’ expenses minimum. More if you have a fluctuating income or don’t feel secure in your job. You want to be able to eat and pay bills if you suddenly lose your income. How long will it take you to find another job? That’s how long you want to cover. This should be cash in the bank – liquid and easy to access.

Basic insurance – health, income protection in case you are sick/injured and unable to work. If you have any significant debt, you may need life cover so your dependents don’t get shouldered with it if the worst happens. If you are unsure what you need, get someone to help you figure it out.

Some kind of pension – don’t overthink this. If you are employed, you probably have it in place. We’re not trying to cover your whole retirement here. To begin with, you should at least be contributing a small amount of money each month to an investment plan with a long-term focus.

Own assets

I heard a campaigning politician complain that while shareholder dividends have risen considerably over the previous 10 years, wages have barely moved. He’s absolutely right.

If the onset of inflation in Japan hasn’t convinced you of the need to own assets, learn the lesson soon. That politician doesn’t actually have a plan to fix anything.

Let’s not argue about stocks, bonds, real estate, commodities, Bitcoin, etc. These are all just ways to protect and increase your purchasing power. Cash is getting eaten alive, and it’s only getting worse. Owning as many of these different assets as you can is the only way to beat inflation.

Bear in mind that volatility is normal and should be expected. Price swings are not risk; being forced to sell or owning too little of anything real is.

Know your time horizon

Asset allocation will vary depending on how long you intend to hold the investment. As a rough guide:

Short-term money (0-3 years) – focus on capital preservation. Cash only for anything shorter than 12 months.

Medium term (3-10 years) – balanced/growth

Long term (10+years) – maximum growth

Understand and plan in your base currency

You need to build assets in the currency you plan to spend the money in eventually. Otherwise, you are exposed to currency risk. The weakening of the yen over the last few years should have driven this lesson home.

There is no point building up yen assets if you are going to spend the money outside Japan. It’s perfectly normal to have more than one base currency. If your future spending currency is unclear, diversifying across currencies is usually better than betting on one.

Three stagesof personal financial planning

Accumulation – spend less than you earn and invest the difference into stocks and other high-growth assets. If asset prices decline, don’t panic and keep buying. In fact, buy more if you can.

Diversification – broaden your asset mix so you own a range of assets across the risk curve. Protect capital, whilst continuing to accumulate.

Distribution – lower the risk and focus on income generation from your accumulated assets.

Fill up tax-advantaged accounts first

Don’t spend months agonising over one investment product versus another. You can roughly prioritise in this order:

Employer matched contributions (if applicable)

Tax-free growth

Tax-deferred investments

As a rule of thumb, take “free money” first, then tax-free growth, then tax deferral.

In Japan, NISA and iDeCo are the key vehicles to understand. These are typically accumulation-stage tools.

Big lump sum investments call for diversification

Dumping a large amount of cash into a single asset class involves significant timing risk. A diversified core/satellite allocation is a good way to gain exposure to higher-risk assets without overdoing it.

Know when to get help

Some people enjoy organising their finances and are good at it. Some hate it and are generally poor at it. Understand where you are on the scale and don’t be afraid to get help.

Some people are more likely to require specialist help, in no particular order:

People with complicated cross-border issues

High-net-worth people who have covered all the basics and need more focused advice

US citizens living abroad – it’s complex!

People dealing with succession planning/inheritance

Remember: Consistency beats optimisation. A good plan you stick to beats a perfect plan you abandon.

You are probably aware that I offer a fee-based coaching service. I have deliberately kept prices low to keep it accessible to as many people as possible. In many cases, the value I provide significantly exceeds the fees I charge. You can read reviews of the service here.

In closing, yesterday the Nikkei 225 index surged almost 4% to a record high in anticipation of an LDP victory in this weekend’s election. Tons of stocks were up big on the day. The day before that, the same index rose in the morning and fell dramatically in the afternoon. A reminder that it’s impossible to guess short-term moves. For someone in the accumulation phase, both days were irrelevant.

Zoom out, cover the basics and make sure you own assets.

The rest will figure itself out.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I’m kind of bullish on stablecoins. And I’m not sure if I’m bullish enough.

It may seem odd to be excited about tokens with a fixed value, but hear me out: 24/7 tokenised stock trading is coming on all your favourite stock and crypto apps. We can argue about whether this is a good thing or not later, but it’s coming regardless. Larry Fink is all over it for starters.

If you have never transacted in stablecoins, it can be scary at first, particularly with large dollar amounts. One mistake in the address field and your coins are ejected into the ether, never to be recovered. It’s a good idea to send a small test transaction first. However, once you get used to it, you will never want to make an overseas bank transfer again. Scan a QR code or copy the deposit address, click, click, click, send, and within a few minutes, the money reaches its destination, anywhere in the world at any time of the day, for very little cost.

So, how is someone going to get money into their trading account on a Sunday afternoon to go 10x long Nvidia when the banks are closed?

Stablecoins.

I realise this is a pretty flimsy investment thesis, so I’m partly writing this post to discover if there is more to it than that. Let’s examine the evidence and see where it goes.

Exhibit A: The GENIUS Act

The US has made significant inroads in stablecoin regulation. The Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act) was signed into law last year to establish a federal regulatory framework for “payment stablecoins.” It’s designed to bring clarity and oversight to a market that had grown rapidly outside traditional financial regulation.

It excludes these tokens from being treated as securities or commodities

It requires stablecoin issuers to hold 1:1 reserves in liquid, low-risk assets (like cash or short-term U.S. Treasuries)

It prevents stablecoin issuers from paying interest or yield to holders simply for holding the coin

It becomes effective in early 2027

So a stablecoin is essentially a digital token that does not fluctuate in value. The issuer must back every stablecoin issued with real assets, such as cash or bonds.

Here’s where it gets interesting – stablecoin issuers are purchasing yield-generating assets like U.S. Treasuries. In unregulated jurisdictions, they can pass part of this yield on to the stablecoin holders. So, owners can earn interest on their stablecoin holdings.

The banks don’t like this at all because the yields on stablecoins are higher than banks are willing to pay their customers. They are worried that stablecoins will pull deposits away from them. The pushback on stablecoin yield is particularly strong from regional banks. The big banks aren’t so concerned because they are all busy creating their own stablecoins.

This post from Patrick @Stillm4n provides an excellent summary of the banking industry’s concerns and attempts to estimate the size of the “systemic risk” to the banks. It also comes with a memorable quote:

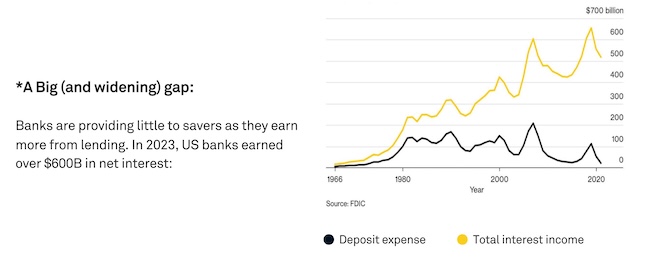

The graph below is from Patrick’s post. No wonder the banks are concerned about losing these fat margins…

Exhibit B: Tether

Tether is the world’s largest stablecoin issuer. Its USDT token has a market cap of around $186 billion. Its reserve composition has been in question for years – no crypto market cycle passes without a round of Tether FUD. (Fear, Uncertainty and Doubt)

In short, Tether’s assets probably outweigh its liabilities. However, Tether is not a listed company and therefore harder to scrutinise than its regulated competitor Circle (CRCL). So the Tether FUD is unlikely to die despite reported assets that include large holdings of U.S. Treasuries, gold, Bitcoin, secured loans, and other instruments. It also recently launched USAT, a U.S.-compliant stablecoin aiming to satisfy the GENIUS Act requirements.

Yields on Tether’s USDT generally range between 2% and 8.8% APY on most reputable platforms, though some specialised DEFI platforms are offering up to 15-22% APR for longer-term, locked-up deposits.

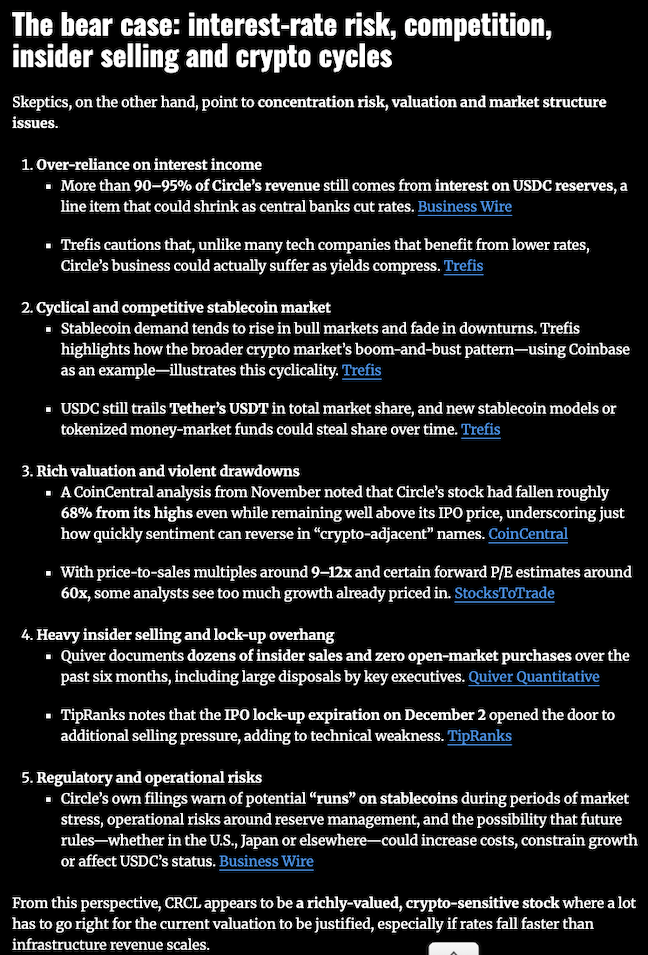

Exhibit C: Circle Internet Group(USDC)

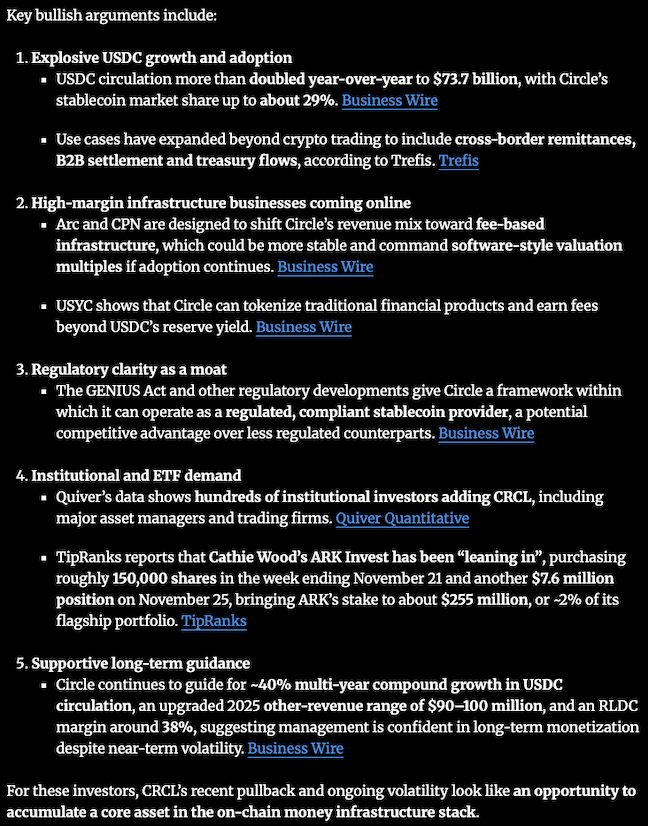

Following its May 2025 IPO, Circle’s NYSE-listed stock (CRCL) now provides a publicly traded way to gain exposure to stablecoin growth via equity rather than direct crypto ownership, which may appeal to traditional investors.

After ripping post-IPO, the stock has pretty much been down only. The bad news is that many see it as a pure crypto stock, so with crypto in a bear market, it is liable to sell off further. The good news is that means there is an opportunity to accumulate it at low prices. I own some already, but was a bit too early initially. It looks more attractive now.

The bull/bear case is nicely laid out in this article:

Exhibit D: The stablecoin landscape in Japan

Surprisingly, Japan has made rapid progress in stablecoin regulation:

Stablecoins are regulated under the Payment Services Act (PSA) as “Electronic Payment Instruments”

Issuance is limited to licensed banks, trust companies, and certain money transfer agents, fostering safety and consumer protection

Recent PSA amendments allow stablecoin issuers to back tokens with up to 50% low-risk liquid assets (e.g., government bonds) rather than 100% demand deposits

Japan’s FSA is consulting on strict reserve bond standards, demanding high credit ratings and minimum issuance levels for eligible backing bonds

Large Japanese banks (MUFG, SMBC, Mizuho) are running stablecoin pilots regulated by the FSA

Circle’s USDC has been approved for use in Japan and is listed on exchanges like SBI VC Trade.

Along with the Megabanks, SBI Holdings, Monex Group and GMO Internet Group are all getting into stablecoins in one way or another. I own most of these already, so I guess I have some pretty good Japan exposure, although I bought these stocks for other reasons.

In summary:

U.S. stablecoin regulation (GENIUS Act) legitimises digital dollars, but bans yield to holders, reflecting bank concerns about competitive deposit flight

Tether remains dominant, but transparency and reserve composition controversies linger

Circle (USDC) offers a more conservative reserve model with strong regulatory alignment and an equity play via CRCL

Japan’s stablecoin framework is progressive and is expanding opportunities for institutional and retail engagement

So, all in all, I’m bullish on stablecoin infrastructure, but not to the point of betting the farm on it. I think this year offers a great opportunity to get some more CRCL exposure.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

We’re only halfway through January, and it already feels like we have lived through a year’s worth of crazy news. Maduro has been ousted, Iran is in turmoil, Mexico and Colombia are on alert, the Europeans are mobilising to protect Greenland, and the chair of the Federal Reserve released a video accusing Trump of bringing criminal charges against him because he refused to bend to his will and lower interest rates quickly enough.

And, despite all of this, many markets are near all-time highs. There really has never been a world leader capable of instigating so much chaos, whilst simultaneously making markets stand up and dance for him.

If you are not convinced by now that Trump is going to pump liquidity and juice the stock market as hard as he can this year, I don’t know what to say.

Likewise, Prime Minister Takaichi. With such a strong approval rating, calling a snap election seems like a calculated risk. The market reaction tells you everything you need to know about her economic policies. Yen down, stocks up. She is going for growth, and that means yen debasement and more inflation coming.

Metals are sounding the alarm on all of this. Bitcoin is also finally starting to respond. The debasement trade is far from dead.

Here are a few thoughts on where this could be going:

Stocks

Mag 7 appears to be cooling somewhat, allowing the S&P 493 to catch up a bit. I’m even hearing American commentators discuss emerging markets. This is probably healthy, although the AI trade is by no means over and data centre spending is not slowing down.

Taiwan Semiconductor reported Q4 earnings this week that beat analyst expectations. Trump just announced a trade deal with Taiwan that will boost investment in the US semiconductor industry, and the deal sees the “reciprocal” tariff rate on Taiwanese goods drop from 20% to 15%.

The biggest short-term threat to stocks is the U.S. Supreme Court’s expected ruling on the legality of the Trump tariffs. If the court rules against these duties, expect all kinds of confusion.

Longer term, it’s hard to be bearish with Trump preparing to install the next Fed chair to do his bidding and midterms looming.

I guess the thing that could derail the Japan bull market would be the LDP performing poorly in the upcoming election and Takaichi being forced out as a result. Conversely, expect another yen down/stocks up surge if she wins a clear mandate.

Metals

The metals trade may not be done, but it’s surely in the late innings. People are starting to ask about copper and palladium. A while back, I put some of my old savings plan into a gold mining fund, and when I checked yesterday, the thing has more than tripled. Half of that went right into bonds for the time being.

If you’ve been in metals, well done! I have no idea if it’s over, but it’s not a bad time to trim some exposure.

There was a report on the 10pm news two nights ago about precious metals: Gold and silver jewellery are selling well in Japan. Dentists are losing money on 銀歯 (silver fillings), which are actually made from a mix of silver, palladium and gold. One dentist interviewed said that some people are even trying to sell their fillings! People are walking around with a hedge against yen debasement in their mouths…

If you are thinking of getting into silver right now, that’s FOMO.

The metals people on X are starting to sound like the crypto bros in a bull market. There are definite signs of euphoria, which means the reversal will likely be brutal when it comes.

Bitcoin

I’m talking Bitcoin, not crypto, as I can only think of a handful of coins that might do well IF Bitcoin gets back over $100k.

There’s an ongoing debate about whether the four-year cycle is dead. I’m not convinced it is, but at the same time, the liquidity backdrop for Bitcoin looks ridiculously good.

Here’s my best effort at a cheat sheet:

If you own Bitcoin, I’m assuming you are long-term bullish. If not, what the hell are you doing in it? I remain bullish on long time frames.

If you believe the 4-year cycle is alive and well, and 2026 will see the usual brutal bear market, prepare some dry powder. The chance to accumulate cheaply is coming.

If you think we bottomed already, you want to accumulate as much as you can under $100k.

If you’re not sure, DCA is the way. Just buy a little at regular intervals and pay as little attention as possible to short-term price fluctuations.

I don’t see a lot of fiscal responsibility coming out of America and Japan in the near future. Long live the debasement trade!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

The whole generative AI thing is pretty weird, but I think I’m starting to get it: Some people are using AI to generate torrents of slop. Other people are using it as a tool to learn and get stuff done. I want to be the latter and avoid the former as much as possible.

The thing I initially found LLMs to be useful for was taking a long, information-dense document, perhaps written in Japanese, and getting a nice, concise summary in English. In particular, I used it to read the earnings reports of companies I was interested in investing in. However, here’s the catch: I’m not a stock analyst. So, often, even with a nice summary, I couldn’t decide if a stock I liked was actually a good investment.

I recently got around to reading Peter Lynch’s excellent One Up On Wall Street. It’s a fabulous book, written for retail investors. If I were to really simplify the book’s content, it would be:

1) How to find great investment opportunities simply by looking around you and finding companies you already know offering products you love

2) How to analyse the company’s financial disclosures to figure out if it’s really a good investment

Of course, there is more to the book than that. But these two things alone made it a hugely worthwhile read.

Now, investing in individual stocks is not for everyone. It’s not even necessary. As I write this, the Nikkei 225 index just hit a new all-time high. It’s up almost +50% over the last two years alone. The S&P 500 is up almost as much over the same period. There is nothing wrong with just owning the index and spending your time doing something else. Just don’t make the “something else” generating AI slop posts on LinkedIn or whatever. Please…

Where am I going with this? Oh, yes. After reading the Peter Lynch book, I realised that I could use some of the techniques in there to identify stocks I’m interested in and then use some of the questions Lynch asks to get AI to help me better understand those companies’ earnings reports.

I’ll give you an example, which I may regret. But it’s a stock I actually bought recently using this method.

As I get older, I notice a lot of people around me are wearing spectacles. Some need them permanently, while others, like my wife, can no longer read what’s on their phone without them. Japan’s ageing population problem is well-documented. I guess a lot of these oldies need glasses. Perhaps that’s why there are glasses shops EVERYWHERE!

Like everywhere. Along busy roads, in department stores, in malls. There are tons of eyewear shops.

I often find myself perusing this Trading View list of Japanese stocks. I like how you can use the tabs to sort and view a list of stocks with the most cash or the highest dividend. A few weeks back, I was looking at the list of oversold stocks and I noticed JINS Holdings (3046). And yes, they sell spectacles. I was in one of their shops with my wife just the other day, and it was really busy. Their specs are high quality and low price. And their stock took a beating over the last few months.

So, I decided to see how Peter Lynch works with ChatGPT. I downloaded the latest company earnings report and fed it to the machine. Instead of just asking for a summary and trying to figure it out myself, I asked ChatGPT to provide a summary that focused on answering some Peter Lynch-style questions:

What’s the recent growth in earnings?

What’s the P/E ratio relative to historic levels?

What makes the stock a good buy now?

Are existing stores in profit?

Where’s the expansion coming from?

What’s the debt situation?

How will they finance growth without selling lots of new shares and diluting the earnings?

Are insiders buying?

How does the stock price look versus the earnings over the last 5 years?

What are the dividends, and have they always been paid?

What percentage of shares are owned by institutions?

I won’t post all of the answers I got here. You can try it yourself if you want to. Suffice to say that the information I got was way more useful than a plain summary of the earnings report.

Later, I also asked ChatGPT to search the web and try to identify possible reasons why the stock is down so much recently.

Asking it to give a web-sourced breakdown of the reasons why the stock might be down was deliberate. You’re not supposed to ask LLMs to think. That’s not what they do. In fact, I find that if you do ask them to think, they tend to go out of their way to confirm your bias and tell you whatever it is you want to hear.

So, anyway, long story short, I bought the stock on Xmas Day. It’s down -6.5% since then lol. And it’s down almost -4% today, a day where the Nikkei surged over 3% to another all-time high. (earnings miss haha!)

So, I may be an idiot. But it’s probably a little early to judge.

My point here isn’t so much about whether this approach works in this particular instance. I enjoy picking stocks, but am aware that I am weak when it comes to analysis. Asking good questions is a life skill that can be applied to many disciplines. Peter Lynch is very good at asking questions about company financials. And LLMs can answer those questions in seconds by reading the earnings report, leaving you with valuable time to do something else.

Don’t try this at home. Or do, but don’t blame me if it doesn’t work. The usual disclaimers apply. If you do try it, please let me know how it goes, what you learned and what other questions you came up with.

Let’s revisit JINS later this year and see how it works out. I’ll be trying more of this to get a larger sample size.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Happy New Year, everyone! Welcome to the year of the horse. Markets are off to a strong start and have not shied away from early geopolitical shenanigans. The going appears to be good to firm as we come out of the gate in January, and runners and riders are expecting a fast race.

Ok, enough horsing around. January means many of us have NISA investments to allocate. It’s time to make some decisions.

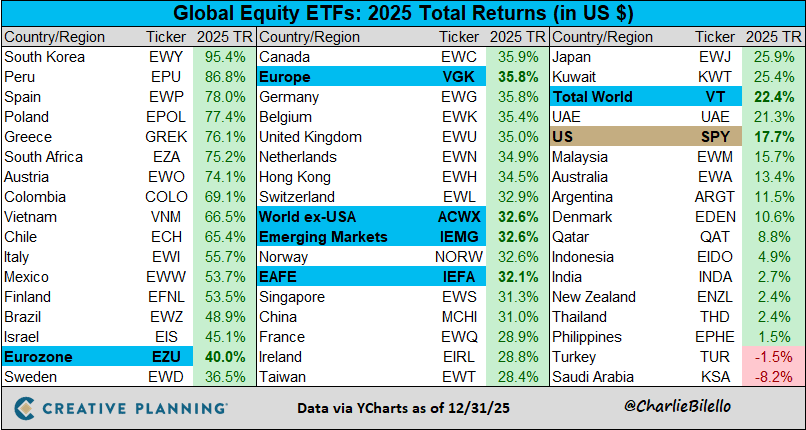

I just scanned through my 2025 New Year post, Snakes and Elephants, and what do you know? This time last year, USD/JPY was around ¥158. Japanese retail investors were largely ignoring the bull market in local stocks and piling into US companies. And Bitcoin was trading at around $93,000.

Great Scott!

At least stocks are a good bit higher than they were this time last year. You would never guess the whole “Liberation Day” debacle happened unless you were there. If your 2025 NISA allocations are not in profit, something went very wrong…

From @CharlieBilello

The difference with Bitcoin is that last year, it was at $93k on the way up. Now, it’s around the same price on the way back down. At least that’s what I think, although many will disagree. But let’s leave the magic internet money for another post.

What is the outlook for equities in 2026?

The Bloomberg Outlook always provides a nice window into what Wall Street expects in the year ahead. In short, pretty much everyone is optimistic, and the AI boom continues to be the main story. The Fed is expected to continue to loosen monetary policy, and Trump and Bessent are also standing by to man the liquidity pump.

The leaders of Japan’s securities firms are also primed for another big year in domestic stocks, as per this NHK article. However, the Japan Times reports here that Japanese retail investors are still more interested in US stocks. It looks like Japanese stocks remain under-owned.

If, like me, you enjoy a little crypto and spice with your macro commentary, Arthur Hayes’ latest post is a fun read. He sees the Trump admin running the economy hot in 2026, whilst simultaneously trying to contain inflation by holding gas prices down. That Venezuelan oil may have a purpose, huh?

Suffice to say that everyone is sufficiently bulled up that we should be at least a little worried. Risk lurks in the AI bubble, excessive government debt, BOJ policy and the yen carry trade, rising bond yields, geopolitical crises, and who knows where else!

We all love a challenge, don’t we?

My themes for 2026, which I outlined in my previous post, are mostly unchanged

For Japan:

Japan’s base interest rate is 0.75%, and inflation is around 3%, so we have a real rate of negative 2.25%

The BOJ can maybe squeeze in one more hike to 1%, so real rates could go to negative 2%

This is still very accommodative monetary policy and will support asset prices

The weak yen will persist

Rice isn’t getting any cheaper, and people’s spending power will continue to decline

By the way, I feel like that last point is going to be critical for the Takaichi administration. People are feeling the pinch, and if prices continue to rise, I expect that beautiful approval rate to take a beating. Complaining about bad foreigners will only distract the public for so long…

Some more general themes:

Trump’s new Fed pick will likely force lower rates

Trump will want to pump the stock market ahead of the midterms

However, the AI trade will continue to come under scrutiny

The debasement trade is very much still in play – own hard assets

Bitcoin bear market – an opportunity to accumulate

I’ll come back to some of these in future posts.

So, what to do with ¥3.6 million?

Of course, I can’t give broad advice here, but I can tell you my own personal plan for NISA this year. Bear in mind that what works for me may not work for you, and we may have different goals and risk profiles. If you need help figuring out what is best for you, remember that I offer a coaching service.

I view NISA as a long-term investment. I want to mess with it as little as possible. If I make a bad pick, sure, I will drop it and reallocate later, but I prefer it to be set and forget.

Therefore, I will stick with last year’s plan of allocating most of Growth NISA to ETFs. I will continue to pick stocks in my taxable account, mainly because I like doing so, not because I really believe I can outperform. (it’s fun to try, and it works sometimes)

While I will allocate some money to global indices, I want to keep a decent chunk in yen. Converting to dollar assets at these exchange rates is painful!

Here are some ETFs I like:

1489 NEXT FUNDS Nikkei 225 High Dividend Yield Stock 50 Index – The S&P 500’s Dividend Yield ended 2025 at 1.15%, its lowest level since 2000.Japan is a dividend paradise, andI love this ETF as a simple way to earn steady dividends without worrying about how a certain company performs over the next decade. For a dividend fund, it has delivered impressive growth these last few years, too.

2644 Global X Japan Semiconductor – this will be volatile, but long-term chip demand is only going up

1624 NEXT FUNDS TOPIX-17 MACHINERY – this is 25% allocated to Mitsubishi Heavy Industries, so a bit concentrated

1627 NEXT FUNDS TOPIX-17 ELECTRIC POWER & GAS – this is a new one for me, and I’m substituting it in for an energy ETF. I’m bullish on power companies.

2559 MAXIS World Equity – good old All Country!

1545 NEXT FUNDS NASDAQ-100 (Unhedged)

The difficult part is timing. Markets are ripping early in the year, and I would love to catch a dip. But who knows when that will come? I will aim to have Growth fully allocated by the 30 March ex-dividend date for Japanese stocks. Maybe Trump can then crash everything in April again for a bit more déjà vu…

Tsumitate, I will keep the same at 40% JPX 400, 30% All Country, 30% NASDAQ. Average in and chill.

How about you? Do you have a plan in place, or are you still mulling the options? I would love to hear what other people are doing.

Wishing everyone all the best for 2026. Let’s make it a great year!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.