I haven’t had much to say on markets for a while. We clearly entered the dumbest timeline, and no amount of TACO is likely to pull us back out of it.

Speaking of tacos, and to keep this post light, my friend recently introduced me to Taco Fanatico. We went to the Shibuya branch – there’s another in Naka-Meguro and even one in Nagoya. Cold beer and tacos definitely beat trying to trade this market…

If I’m not mistaken, said market is almost entirely driven by Trump’s social media posts rather than actual events. And, once more, I could be wrong, but the great dealmaker appears to be negotiating with himself. The Iranians have probably read the Chris Voss book. Trump doesn’t strike me as much of a reader…

You have probably had enough armchair geopolitics, so I won’t add to the discourse. Here’s BlackRock Chairman Larry Fink with two extreme scenarios:

“GLOBAL RECESSION”

The man who manages $11 trillion just warned the world what’s going to happen if Trump doesn’t make a DEAL, now.

A total wipeout.

Larry Fink, CEO of BlackRock, the largest asset manager in human history explains to the BBC how that occurs 👇🏼 pic.twitter.com/HqYrOhwj8x

In short, either the war ends, and things go “back to normal”, and markets revert to being insane in a good way. Or we get $150 oil for an extended period and a global recession.

Hope for the best and plan for the worst. Short-term investors would want to be defensively positioned. Long-term investors can, and probably will have to, endure some pain. A globally diversified portfolio, perhaps with satellite holdings in hard assets, is not going to be a cake walk, but you don’t have to look at it every day.

I think I summed up my views on how to plan effectively in noisy markets in my Back to basics post.

Asian economies in particular are in a precarious position. Japan is better prepared than some other countries, although the prospect of higher inflation, low growth and a floundering yen is not exactly mouthwatering.

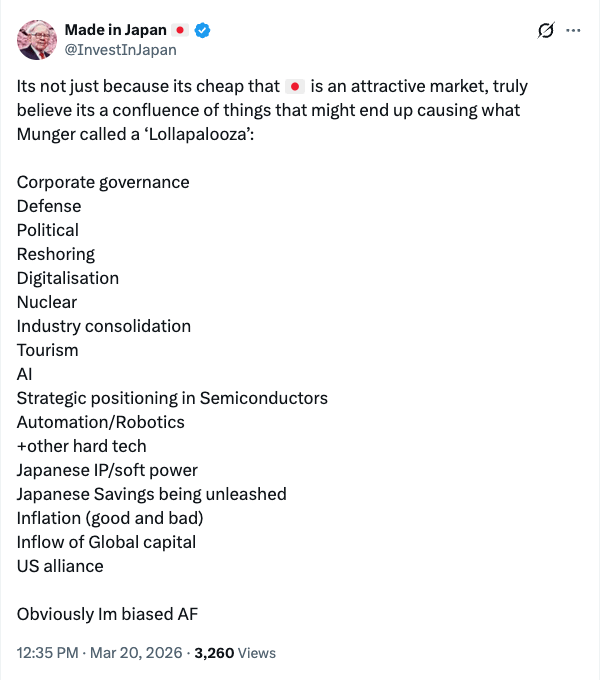

That said, the Japanese stock market still has a lot going for it, and the opportunity is nicely summed up here:

I may also be biased, but with many people trapped in yen, the investment options are not too shabby.

I’ve been buying some stocks on the heavy red days, but am exercising caution. I even bought a little Bitcoin, despite the nagging feeling that lower prices await.

Be careful out there. It’s a great time to touch grass, admire the sakura and eat tacos.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Well, that’s month one of 2026 done. We’ve seen stocks near record highs, the yen up and down, metals explode upwards and then hit the ceiling hard, crypto confirm a bear market, Trump & Co. lecture the WEF, and so much more. Remember Greenland? What happened to that? How about Venezuela? The Maduro raid was only a month ago!

It’s pretty much impossible to make responsible financial planning decisions day to day without a solid framework. There is simply too much noise. I realise I am part of the problem, as I try to write content that is current and engaging. So, perhaps it’s time to take a step back and review the basics.

You’ve probably heard all this before. If you read this blog regularly, you most certainly have come across this information multiple times. Sometimes you just have to put in the reps, so bear with me.

Protect yourself and your family

Start with a solid foundation, so you can handle the typical curveballs that life throws at you without having to cancel plans and unwind investments.

Pay off high-interest debt – get rid of that credit card debt asap

Emergency cash reserve – 3 to 6 months’ expenses minimum. More if you have a fluctuating income or don’t feel secure in your job. You want to be able to eat and pay bills if you suddenly lose your income. How long will it take you to find another job? That’s how long you want to cover. This should be cash in the bank – liquid and easy to access.

Basic insurance – health, income protection in case you are sick/injured and unable to work. If you have any significant debt, you may need life cover so your dependents don’t get shouldered with it if the worst happens. If you are unsure what you need, get someone to help you figure it out.

Some kind of pension – don’t overthink this. If you are employed, you probably have it in place. We’re not trying to cover your whole retirement here. To begin with, you should at least be contributing a small amount of money each month to an investment plan with a long-term focus.

Own assets

I heard a campaigning politician complain that while shareholder dividends have risen considerably over the previous 10 years, wages have barely moved. He’s absolutely right.

If the onset of inflation in Japan hasn’t convinced you of the need to own assets, learn the lesson soon. That politician doesn’t actually have a plan to fix anything.

Let’s not argue about stocks, bonds, real estate, commodities, Bitcoin, etc. These are all just ways to protect and increase your purchasing power. Cash is getting eaten alive, and it’s only getting worse. Owning as many of these different assets as you can is the only way to beat inflation.

Bear in mind that volatility is normal and should be expected. Price swings are not risk; being forced to sell or owning too little of anything real is.

Know your time horizon

Asset allocation will vary depending on how long you intend to hold the investment. As a rough guide:

Short-term money (0-3 years) – focus on capital preservation. Cash only for anything shorter than 12 months.

Medium term (3-10 years) – balanced/growth

Long term (10+years) – maximum growth

Understand and plan in your base currency

You need to build assets in the currency you plan to spend the money in eventually. Otherwise, you are exposed to currency risk. The weakening of the yen over the last few years should have driven this lesson home.

There is no point building up yen assets if you are going to spend the money outside Japan. It’s perfectly normal to have more than one base currency. If your future spending currency is unclear, diversifying across currencies is usually better than betting on one.

Three stagesof personal financial planning

Accumulation – spend less than you earn and invest the difference into stocks and other high-growth assets. If asset prices decline, don’t panic and keep buying. In fact, buy more if you can.

Diversification – broaden your asset mix so you own a range of assets across the risk curve. Protect capital, whilst continuing to accumulate.

Distribution – lower the risk and focus on income generation from your accumulated assets.

Fill up tax-advantaged accounts first

Don’t spend months agonising over one investment product versus another. You can roughly prioritise in this order:

Employer matched contributions (if applicable)

Tax-free growth

Tax-deferred investments

As a rule of thumb, take “free money” first, then tax-free growth, then tax deferral.

In Japan, NISA and iDeCo are the key vehicles to understand. These are typically accumulation-stage tools.

Big lump sum investments call for diversification

Dumping a large amount of cash into a single asset class involves significant timing risk. A diversified core/satellite allocation is a good way to gain exposure to higher-risk assets without overdoing it.

Know when to get help

Some people enjoy organising their finances and are good at it. Some hate it and are generally poor at it. Understand where you are on the scale and don’t be afraid to get help.

Some people are more likely to require specialist help, in no particular order:

People with complicated cross-border issues

High-net-worth people who have covered all the basics and need more focused advice

US citizens living abroad – it’s complex!

People dealing with succession planning/inheritance

Remember: Consistency beats optimisation. A good plan you stick to beats a perfect plan you abandon.

You are probably aware that I offer a fee-based coaching service. I have deliberately kept prices low to keep it accessible to as many people as possible. In many cases, the value I provide significantly exceeds the fees I charge. You can read reviews of the service here.

In closing, yesterday the Nikkei 225 index surged almost 4% to a record high in anticipation of an LDP victory in this weekend’s election. Tons of stocks were up big on the day. The day before that, the same index rose in the morning and fell dramatically in the afternoon. A reminder that it’s impossible to guess short-term moves. For someone in the accumulation phase, both days were irrelevant.

Zoom out, cover the basics and make sure you own assets.

The rest will figure itself out.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Happy New Year, everyone! Welcome to the year of the horse. Markets are off to a strong start and have not shied away from early geopolitical shenanigans. The going appears to be good to firm as we come out of the gate in January, and runners and riders are expecting a fast race.

Ok, enough horsing around. January means many of us have NISA investments to allocate. It’s time to make some decisions.

I just scanned through my 2025 New Year post, Snakes and Elephants, and what do you know? This time last year, USD/JPY was around ¥158. Japanese retail investors were largely ignoring the bull market in local stocks and piling into US companies. And Bitcoin was trading at around $93,000.

Great Scott!

At least stocks are a good bit higher than they were this time last year. You would never guess the whole “Liberation Day” debacle happened unless you were there. If your 2025 NISA allocations are not in profit, something went very wrong…

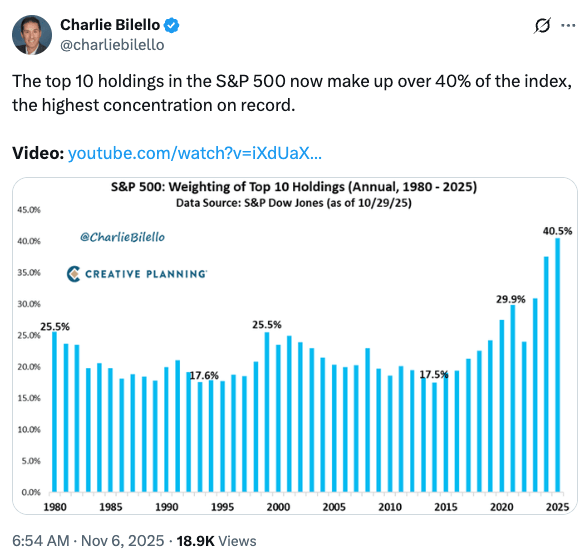

From @CharlieBilello

The difference with Bitcoin is that last year, it was at $93k on the way up. Now, it’s around the same price on the way back down. At least that’s what I think, although many will disagree. But let’s leave the magic internet money for another post.

What is the outlook for equities in 2026?

The Bloomberg Outlook always provides a nice window into what Wall Street expects in the year ahead. In short, pretty much everyone is optimistic, and the AI boom continues to be the main story. The Fed is expected to continue to loosen monetary policy, and Trump and Bessent are also standing by to man the liquidity pump.

The leaders of Japan’s securities firms are also primed for another big year in domestic stocks, as per this NHK article. However, the Japan Times reports here that Japanese retail investors are still more interested in US stocks. It looks like Japanese stocks remain under-owned.

If, like me, you enjoy a little crypto and spice with your macro commentary, Arthur Hayes’ latest post is a fun read. He sees the Trump admin running the economy hot in 2026, whilst simultaneously trying to contain inflation by holding gas prices down. That Venezuelan oil may have a purpose, huh?

Suffice to say that everyone is sufficiently bulled up that we should be at least a little worried. Risk lurks in the AI bubble, excessive government debt, BOJ policy and the yen carry trade, rising bond yields, geopolitical crises, and who knows where else!

We all love a challenge, don’t we?

My themes for 2026, which I outlined in my previous post, are mostly unchanged

For Japan:

Japan’s base interest rate is 0.75%, and inflation is around 3%, so we have a real rate of negative 2.25%

The BOJ can maybe squeeze in one more hike to 1%, so real rates could go to negative 2%

This is still very accommodative monetary policy and will support asset prices

The weak yen will persist

Rice isn’t getting any cheaper, and people’s spending power will continue to decline

By the way, I feel like that last point is going to be critical for the Takaichi administration. People are feeling the pinch, and if prices continue to rise, I expect that beautiful approval rate to take a beating. Complaining about bad foreigners will only distract the public for so long…

Some more general themes:

Trump’s new Fed pick will likely force lower rates

Trump will want to pump the stock market ahead of the midterms

However, the AI trade will continue to come under scrutiny

The debasement trade is very much still in play – own hard assets

Bitcoin bear market – an opportunity to accumulate

I’ll come back to some of these in future posts.

So, what to do with ¥3.6 million?

Of course, I can’t give broad advice here, but I can tell you my own personal plan for NISA this year. Bear in mind that what works for me may not work for you, and we may have different goals and risk profiles. If you need help figuring out what is best for you, remember that I offer a coaching service.

I view NISA as a long-term investment. I want to mess with it as little as possible. If I make a bad pick, sure, I will drop it and reallocate later, but I prefer it to be set and forget.

Therefore, I will stick with last year’s plan of allocating most of Growth NISA to ETFs. I will continue to pick stocks in my taxable account, mainly because I like doing so, not because I really believe I can outperform. (it’s fun to try, and it works sometimes)

While I will allocate some money to global indices, I want to keep a decent chunk in yen. Converting to dollar assets at these exchange rates is painful!

Here are some ETFs I like:

1489 NEXT FUNDS Nikkei 225 High Dividend Yield Stock 50 Index – The S&P 500’s Dividend Yield ended 2025 at 1.15%, its lowest level since 2000.Japan is a dividend paradise, andI love this ETF as a simple way to earn steady dividends without worrying about how a certain company performs over the next decade. For a dividend fund, it has delivered impressive growth these last few years, too.

2644 Global X Japan Semiconductor – this will be volatile, but long-term chip demand is only going up

1624 NEXT FUNDS TOPIX-17 MACHINERY – this is 25% allocated to Mitsubishi Heavy Industries, so a bit concentrated

1627 NEXT FUNDS TOPIX-17 ELECTRIC POWER & GAS – this is a new one for me, and I’m substituting it in for an energy ETF. I’m bullish on power companies.

2559 MAXIS World Equity – good old All Country!

1545 NEXT FUNDS NASDAQ-100 (Unhedged)

The difficult part is timing. Markets are ripping early in the year, and I would love to catch a dip. But who knows when that will come? I will aim to have Growth fully allocated by the 30 March ex-dividend date for Japanese stocks. Maybe Trump can then crash everything in April again for a bit more déjà vu…

Tsumitate, I will keep the same at 40% JPX 400, 30% All Country, 30% NASDAQ. Average in and chill.

How about you? Do you have a plan in place, or are you still mulling the options? I would love to hear what other people are doing.

Wishing everyone all the best for 2026. Let’s make it a great year!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I came back from the gym this morning and found my wife at her desk.

“Wow, my stocks are up again!”

This is good news.

“But why are they going up so much? News on the economy doesn’t seem so great.”

I begin an explanation of how low interest rates have finally reignited inflation in Japan and fueled a boom in stocks. And despite the recent rate hike by the Bank of Japan, real rates remain negative, which means the price of things, including assets, will continue to rise.

Her eyes quickly glaze over, and she goes back to work. I put some coffee on. Then I begin writing this, in case someone is actually interested!

USD/JPY is at ¥157. GBP/JPY is ¥210!!!

Last week’s BOJ rate hike was viewed mainly as an effort to prop up the currency. But it seems unlikely to halt the slide back to ¥160. Could we go further than that next year?

Here’s a quick reminder about the bind the central bank finds itself in, from my January 2023 post How screwed is the yen?:

The BOJ is caught in a spiral of rising bond yields and a falling yen. And between the bond market and the yen, it can only save one. The programs you would have to enact to save the yen are the exact opposite of the programs you would have to enact to save the bonds. To save the currency, you have to raise rates. To save the bond market, you need to keep rates low.

Last week’s rate hike was a band-aid. Many were hoping for at least a short-term bounce in the yen, but it didn’t come. The BOJ can’t manage an aggressive hiking cycle without destroying the bond market and taking down the banks, pension funds and insurance companies that own the bonds.

This is all very depressing, I know. However, I imagine many of us will be looking to allocate money to NISA, etc, next year and need to begin thinking what to do with it. I haven’t made any decisions myself yet, but I’m beginning to put together a list of themes that will influence these decisions:

Themes for 2026

Japan’s base interest rate is 0.75%, inflation is around 3%, so we have a real rate of negative 2.25%

The BOJ can maybe squeeze in one more hike to 1%, so real rates could go to negative 2%

This is still very accommodative monetary policy and will support asset prices

The weak yen will persist and perhaps go beyond 160

Rice isn’t getting any cheaper, and people’s spending power will continue to decline

To be clear, I’m not in the doomer “Japan has reached the end of the road” camp. Japan is the world heavyweight champion of muddling through with extraordinary monetary policy. There’s still a lot of road to kick this can down. However, those who do not own financial assets will struggle. It’s not going to be pretty.

Outside Japan, things could get pretty spicy, too.

Better have a plan to not get knocked out!

A few additional themes:

Trump’s new Fed pick will likely force lower rates

Trump will want to pump the stock market ahead of the midterms

However, the AI trade will continue to come under scrutiny

The debasement trade is very much still in play – own hard assets

Bitcoin bear market – an opportunity to accumulate

I will think on this some more and come back with a plan for 2026 in the next few weeks. Let’s see if the yen breaches the ¥160 mark before the year’s end.

Thanks for reading. Wishing you all a wonderful Christmas!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Markets are not looking so hot right now. I really hate to be bearish, but it’s becoming unavoidable.

Last week, Bitcoin made its first daily close below $100,000 in 188 days. Then yesterday it closed below the 50-day moving average on the weekly chart. This is always bad news for bulls. Some of the people who were telling us the 4-year cycle is over are still holding out for a reversal, but they are probably grasping at straws.

We are so done. Thank you for playing.

I know it’s unlike me to be so negative, but when a situation changes, it’s important to confront reality quickly. Crypto is heading into a bear market, and it’s right on schedule.

Initially, Bitcoin is acting as the pressure release valve as investors lose faith in an overheated risk environment. You will note how, over the last week or so, Bitcoin is lower when you wake up. Asia propped up the price in the daytime, and then America sold hard while we slept. Now Asia is selling, too.

Worse still, BTC tends to lead equities, and in my humble opinion, BTC is heading lower.

Stocks are already wobbling. In particular, the AI trade is coming under increased scrutiny. Nvidia earnings are due on Wednesday. I don’t think there are numbers big enough to satisfy the masses this time, although the numbers will likely be impressive regardless.

Burry put on his Nvidia/Palantir short and then closed his fund. Now he doesn’t have to worry about investors trying to pull their money when the market moves against him. People are debating whether he is actually any good at calling this stuff, which is a valid question. It’s such an obvious trade that you wonder if it can really be that simple, especially with Trump there to pump the markets every time they stumble.

But it doesn’t look great to me. In the short term, at least, I’m siding with the bears.

Time preference is key

It’s ok to be bearish, but the big question is: over what timeframe?

BTC is a good starting point for this discussion, as it is highly sensitive to both global liquidity and overall risk sentiment.

When Bitcoin topped in November 2021, it was just as the Federal Reserve pivoted to begin a brutal tightening regime. Interestingly enough, in November 2025, the Fed is going in the opposite direction. In fact, the market was pricing in a further rate cut in December until the US government shutdown delayed the data and muddied the waters. Uncertainty around rates is a huge factor in sparking the sudden loss of appetite for risk.

The liquidity picture for 2026 actually looks pretty rosy. Trump is effectively going to gain control over the Fed, and he has the midterm elections to pump the market for. On the flip side of that lies a slowing US economy.

Bitcoin’s level of institutional adoption was meagre in 2021/2022. In fact, it turned out the industry was on the brink of collapse. And collapse it did: Terra/Luna, Celsius, Blockfi, 3AC, and, of course, FTX all fell during the bear market.

The picture is very different now. US Bitcoin ETFs have almost $120 billion in assets under management. $72 billion of that is in BlackRock’s IBIT alone. What’s more, the Trump administration is pro-crypto. This is not an industry on the brink of collapse any more. It’s just going to need to take a breather for a while.

Plan for the worst

The typical bear market drawdown from the peak for Bitcoin is 80%. So, worst case, we are going back to $25,000. Ouch! Not pleasant at all, but I would not bet against this outcome.

If ETFs and institutional adoption, plus a favourable liquidity cycle count for anything, which I think they do, we may not go that low. Personally, I’m not really interested in bidding $90k. I’ll get interested at lower levels. $50k seems a bit more like it. (this is my finger in the air, best guess if you are wondering how I got this number)

Here’s a little perspective:

What about stocks?

Nvidia’s P/E ratio is around 53. Investors are willing to pay that amount for each dollar of the company’s earnings. I probably don’t need to tell you that future earnings expectations are a little on the high side. The Magnificent 7’s average P/E ratio is around 28 to 35. Those expectations may well be due for a sharp adjustment.

The other 493 stocks in the S&P 500 are not looking so bad, although they could get dragged down somewhat in a Mag 7 correction.

Global stocks, Japan included, are unlikely to emerge unscathed, but we could well be looking at an interesting buying opportunity.

Personally, I kind of like the idea of reducing US exposure (particularly Mag 7) and increasing Japan. The only problem is then you get trapped in yen. Finance Minister Katayama is making the usual concerned noises about exchange rates, while taking absolutely no action to counter the yen’s decline. Real interest rates in Japan remain negative, and as long as they persist, the currency will continue to struggle.

Negative real rates are a boon for stocks, though. If rates somehow ever turn positive, it’s time to rethink.

All in all, it comes down to where you are in the financial planning process. I covered this in the Burry post, but here it is again in simpler form.

I see three key stages in the personal finance journey:

Accumulation – spend less than you earn and invest the difference into stocks and other high-growth assets. If asset prices decline, don’t panic and keep buying. In fact, buy more if you can.

Diversification – a mix of protecting capital, whilst continuing to accumulate. The key to knowing when to diversify comes down to three factors:

a) The data tells you – you hit your number and simply don’t need as much risk any more

b) You become conscious of the amount of money you have at risk and start thinking about what to do

c) Asset prices are considerably higher than the average price you paid when accumulating. Despite the wobbles, we are still in this zone for anyone who has been accumulating for a while. It may not last much longer, however…

3. Distribution – you begin living off the income generated from your accumulated assets, or simply spending the money

If you are in stage 1 or 3 and are properly allocated, a stock market correction should not bother you too much. If you are at stage 2 but have not diversified yet, the current window of opportunity may be about to close for a while. Don’t panic, but perhaps give it some thought.

Personally, I have been selling stocks that have done well over the short term, particularly tech/semi/AI-related stuff. A few Japanese tech stocks I owned got a big boost when PM Takaichi was elected and are probably due for a reality check.

In other business

My next casual meetup, billed as the Nikkei ¥50,000 party, is on 26 November from 7pm at Hobgoblin Roppongi. Everyone is welcome. You don’t have to talk about investing, and you don’t have to drink unless you want to. Some of us may need to!

Before you ask, yes, the event will go ahead even if the Nikkei is below ¥50,000. That is an achievement unlocked, and I’m sure we’ll be back above that level in due course.

Don’t get too bearish!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s been another interesting week. ‘Big Short’ legend Michael Burry returned to X to call out the AI bubble, posting charts that question whether the ongoing mega AI capex boom really matches demand. Burry pops up every now and then to predict disaster, and his hit rate post-2008 is not all that spectacular. However, he followed up by filing his investment firm’s 13F 11 days early, showing that he is short 1 million Nvidia shares and 5 million Palantir shares.

Money where his mouth is.

The market took notice and US tech stocks tumbled on 4 November. Japanese stocks followed suit, with Softbank Group dumping almost -17% over 2 days. This comes at a time when the US government shutdown is blocking the liquidity faucet and tightening things up considerably.

Crypto didn’t like it either, but hey…

Predictably, President Trump issued some positive comments about stocks and Bitcoin overnight, and the situation calmed down. Every time I think this market is ready to begin its descent into hell, I’m reminded that the guy in charge of America has a vested interest in keeping it above ground…

Clearly, Burry is hitting a nerve with AI bubble enjoyers. Here’s a great thread from Marko Bjegovic covering why he is probably correct.

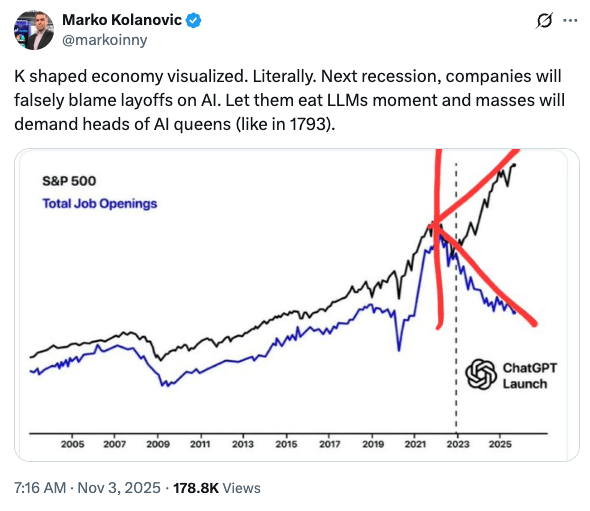

The ‘K-shaped’ economy

You are probably hearing this term lately. The K-shape represents the latest expression of wealth inequality. Essentially, high earners and large corporations are getting richer as asset prices rise, while low-income households and small businesses, the lower leg of the K, are struggling to get by.

High-end products are selling, while companies like Chipotle are finding their customers poorer and less inclined to visit.

Here’s another way of looking at the K-shape, from a different Marko:

Speaking of liquidity and the AI bubble, Ray Dalio just posted about how the Fed is stimulating at an odd time. I’m not sure the Fed is really beginning QE, as he says, but it is certainly ending QT, cutting rates and taking an expansionary stance. This is something it would generally do when the economy is in trouble. Instead, the backdrop for the Fed’s easing is high asset valuations, a relatively strong economy, inflation above target and abundant credit. Not to mention a bubble in AI-related stocks – the elephant in the room, so to speak.

The Trump administration is taking a bold and probably reckless bet on growth, and particularly AI growth. What could go wrong???

Time to take profit?

We’ve been talking about a melt-up before a melt-down, but that’s by no means guaranteed, and we’ve already melted up a lot.

Stock investors, belonging to the top leg of the K, have done very well, but are now faced with a choice: remain invested and ride through the bubble or protect capital. As Michael Burry experienced in 2008, bubbles can keep inflating and punishing shorts for a long time before they finally pop. Younger investors can probably handle the drawdown, provided they are disciplined enough not to sell the bust. We all know the drill when panic hits: as the last desperate few capitulate, central banks will cut rates, stimulate, and markets will surge back over the next 12-18 months.

People who are getting closer to spending their investment money should probably think more carefully. There may not be a better opportunity to take risk off the table and diversify for some time. Nobody ever went broke taking profit, especially around all-time highs.

For people in between, US treasuries are holding up as a safe haven as well as anything else at this time. Spreading some of the risk also serves an often overlooked purpose: offering the opportunity to rebalance and buy the bottom in stocks if we do suffer a crash. I stand by my belief that anyone with a meaningful amount of money should be well diversified at a time like this.

The stock market is not the economy

Here in Japan, we are enjoying the Nikkei holding above the ¥50,000 mark. That doesn’t mean we escaped the K-shaped economy. In a rare quiet moment the other evening, I was thinking about Japan’s economy and why interest rates don’t seem to go up much. Aside from the rich asset holders, many people are struggling. Wages still lag inflation. 5kg of rice is almost ¥5,000. The lower/middle classes do not have a lot of money to spend.

Fewer people spending money is bad for the economy. The general expectation seems to be that interest rates will rise gradually. They certainly won’t rise quickly. Higher rates would mean higher interest payments on government debt. PM Takaichi is focused on growth, not inflation.

Should we really expect a meaningful rise in interest rates? I simply can’t see it.

If rates can’t rise, then the yen remains weak, prices increase, stocks and Tokyo property appreciate, and low-income families continue to struggle.

If all this is true, then what’s the trade?

Own dollars, own financial assets, own hard assets, and be kind…

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I woke up last Saturday morning and, as is my habit, checked on the overnight market movements. I did a double-take and wondered what the hell had happened. Bitcoin, perhaps the nimblest indicator of global risk appetite, had dumped heavily. Several possible scenarios ran through my mind, but I knew it could only mean one thing…

Donald Trump has posted something!

Bingo! After market hours on a Friday, America’s fearless leader had somehow mangled a Chinese announcement on rare earth exports and sent out a post threatening further 100% tariffs on China. After all the TACO earlier this year, I had forgotten about the trade war!

Had stock markets been open, they would not have liked it at all. As they were closed, crypto bore the brunt, and anyone unfortunate enough to be awake got to witness the biggest liquidation cascade of all time. Bitcoin fell to around $104,000 initially before bouncing. Alts were nuked without mercy, with $ATOM token getting as close to zero as you can really get without going negative.

Something in the range of $18.7 billion in positions got liquidated in a matter of minutes, and around $560 billion was wiped from the total crypto market cap. Fun times!

I won’t get into the whole conspiracy theory of what happened. Suffice to say, a very large and very suspicious short position appeared in the market shortly before the fun began. This seems to be the only person who made money that day. It could be a coincidence, of course. I guess we will never know…

Japan is moving to ban insider trading in crypto, by the way. Seems like a good call.

Bitcoin hodlers would be a little concerned to see the price fall so quickly, but most take it in their stride. Leveraged traders, however, some of whom don’t even own Bitcoin, did not make out so well. Many got a lesson in risk management they will never forget.

Of course, by the US open on Monday morning, Trump had already straightened things out, and stocks acted like nothing had ever happened.

It’s always the leverage

Most people should stay away from leverage. Hell, even skilled traders should handle it with care. And yet, Volatility Shares just filed for a total of 27 leveraged 3x and 5x single asset ETFs. If approved, every Robinhooder will be able to go 5x long Nvidia, Palantir, XRP and more. What could possibly go wrong?

Wall of worry

We’re so back! Add to this the growing concern over the AI-driven boom and whether it is, in fact, a bubble, and you have to wonder if the Q4 melt-up might be cancelled.

The AI bubble talk is understandable. OpenAI has around $1.5 trillion in AI build-out plans. This for an unprofitable company with only $13 billion in annual revenue. Both smart money and dumb money alike are positioned for a bullish Q4. Tech stocks sure have a long way to fall if investors lose their nerve.

A week or two ago, the CEO of Goldman Sachs warned that a stock market correction could occur in the next 12-24 months. Thanks for the deep insight, bro! Jamie Dimon is talking about gold possibly going to $5,000 or even $10,000.

Throw in the US government’s shutdown, and you may wonder how stocks can possibly rise further. Surely the Bitcoin bull run is over, too?

While Trump was busy TACOing, Jerome Powell came out on Tuesday and said that “the downside risks to employment appear to have risen.” That appears to imply a further rate cut at the Fed’s end-of-month meeting. More importantly, JPow signalled the end of the Fed’s balance sheet runoff. If quantitative tightening is really over and liquidity flows, the wall of worry could melt rapidly.

I don’t know what’s going to happen, and you certainly shouldn’t be making investment decisions based on my offhand opinions, but if we get a strong earnings season, I still see a bullish Q4 and then trouble on the horizon in 2026. It’s never dull, is it?

Yes, Prime Minister

Organising a Prime Minister seems to be a tough gig these days. France had a guy quit and then get reappointed in the same week! Here in Japan, Sanae Takaichi went from being a done deal to less than Liz Truss in a couple of days. Now the LDP is courting the opposition, and it’s looking like they might find the votes to anoint the country’s first female Prime Minister after all. Who knows?

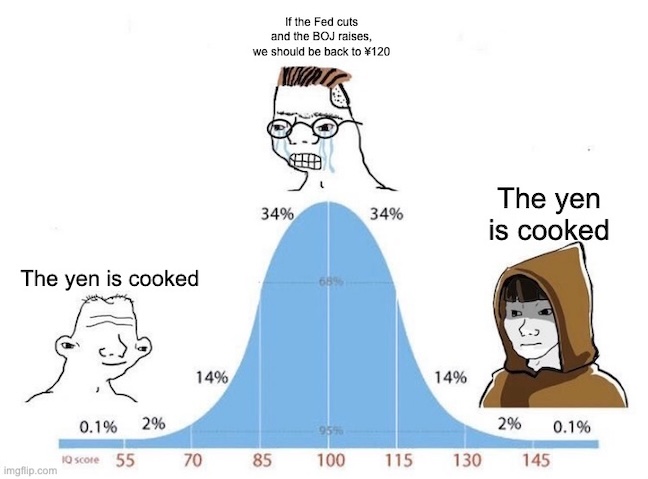

The market has already tipped its hand if the deal gets done. JP stocks up and yen down. I will unapologetically cheer for our iron lady just because I want my Nikkei ¥50,000 party. The yen is cooked anyway.

A diversified portfolio matched to your base currency and risk profile with satellite holdings in debasement assets.

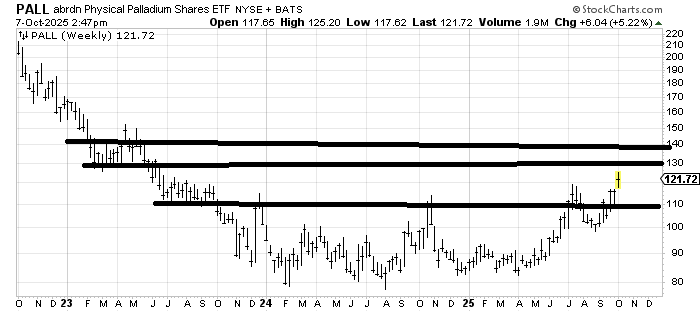

I sound like a broken record, don’t I? By the way, I found a Japan Physical Palladium ETF (1543). It’s amazing what is available these days. Don’t do anything I wouldn’t do!

Thank you for your attention to this matter.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

You can’t time the market. Except those times when you can. Last week, I wrote a post called Melt Up? Maybe I got lucky, but the meltup began right after and is now in full swing. Gold, Bitcoin and of course, Japanese stocks.

Not that I’m claiming clairvoyance here. I had no idea how the market would react to the LDP leadership vote. Generally, I discount politics as it has far less effect on asset prices than people think. At first, I thought the market reaction was relief that the younger, less experienced guy didn’t get in, but clearly it’s not that. It’s all about the new leader.

I won’t delve into political analysis. I don’t have any edge here. Takaichi’s economic stance is perceived as expansionary, and there seems to be an expectation that she will go full Abenomics on us. That remains to be seen, but here are a few observations:

Taro Aso was clearly instrumental in getting Takaichi elected and will be a key figure in the administration. He opposes ‘modern monetary theory’ and argues for fiscal discipline. Watch the yen over the coming months to find out who is really in charge.

When Abenomics was implemented, USD/JPY was at 80 and inflation was negative. Now we have the dollar at 152 and 3% inflation. It’s a very different world. You can’t just cut rates to zero and reimplement QE without inflation blazing out of control.

The BOJ may not be entirely free from political interference, but it will make its own decisions. It may or may not hike at the next meeting, but it’s not going to go the other way any time soon. No doubt, Chairman Ueda’s job just got a little more complicated, though.

I’ll stop there. Prime Ministers don’t seem to last very long these days, so we should probably give it 6 months or so before expecting a clear indication of where this will land. For now, you can probably give up on any hopes of a stronger yen. And you’d better own stocks and hard assets.

The meltup continues. I joked about having a Nikkei ¥50,000 party on X, but I think we should do it. It may be soon, so get ready!

Running it hot

If you are seeing posts and mentions about the ‘debasement trade’, it’s no wonder.

I’ve been harping on about monetary debasement for some time. People seem to be getting the idea. I’m seeing more and more people who don’t own gold capitulating and buying it at all-time highs. They should have owned it earlier, but that doesn’t make them wrong for getting some now.

Reminder: if you run a diversified portfolio, you will already have a 5-10% allocation to gold. You don’t have to play catch-up. People who only own stocks are learning this now.

It’s clearly a sign that people’s portfolios are at all-time highs. We should probably be a little careful about getting too greedy, but it’s a wonderful time to consider how to get joy out of the money we have worked for and taken risk to grow.

I ordered the orange iPhone. It’s due to be delivered in early November. I wasn’t planning on becoming a walking top signal, but maybe I’m about to…

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I am reading “When Genius Failed: The Rise and Fall of Long-Term Capital Management”. It’s the remarkable story of a ’90s hedge fund comprising a group of big-brained academics, including Nobel Prize winners, who were so convinced that their models were infallible that they built a gigantic book of highly leveraged derivative trades. Even if you’re not familiar with the story, you can imagine how that ended.

The smart money doesn’t always win.

One of my favourite books is Jon Krakauer’s “Into Thin Air”. LTCM is like the hedge fund version of that cautionary tale. Hubris and leverage are a dangerous combination. The academics somehow convinced themselves that they had modelled out every outcome, and even if things went bad, there would always be enough liquidity to get out of their positions. Of course, ‘one in a million’ events happen more frequently than we expect, and when they do, nobody is around to buy what you desparately need to sell.

At least we learn our lessons, right? Well, LTCM blew up in 1998, and it was only 10 years later that Bear Stearns, which was closely linked to the fund, faced its own meltdown.

There’s a lot to be said for keeping things simple. Viva le dumb money!

Wait, isn’t this site supposed to be SMART Money Asia?

This is easily the greatest meme ever created. It applies to so many areas of life, and none more than investing. The LTCM guys were just too far out on the right of the curve that they no longer lived in reality.

Generally, the smart money and the dumb money follow the same strategy. They buy risk assets and sit on them. In my previous post, Liquid Refreshment, I covered how tech stocks and Bitcoin are the two things that outperform currency debasement. And what do the Robinhood degenerate gamblers do? They buy Mag 7 and IBIT and print money. When these assets dip, they buy more! What are the older, wiser retirement accounts buying? NASDAQ and IBIT, by the looks of it!

Wait, is the diversified portfolio guy telling us to just buy tech stocks and Bitcoin?

I have always said, if it’s a meaningful amount of money, you should have a core diversified portfolio weighted toward your base currency for about 80% of your wealth. You can allocate 20% or so to satellite holdings to take advantage of opportunities for higher returns. This is where you can go hard on tech stocks, gold, commodities and Bitcoin/crypto as you wish.

Overthinking and mid-curving are the killers. See my post, It’s going up forever, Laura, on why dumb money wins in the end.

I see that USD/JPY is back at ¥150. Let’s do the meme:

Simple!

Of course, mid-curve guy is right. Short-term, barring any crazy events (which happen a lot!), the yen should strengthen against the dollar. However, if you are doing long-term planning and trying to figure out how currency could affect you, it’s pretty clear that the country with the worst debt/demographics profile is going to lose against the country with the global reserve currency.

Plan accordingly.

Trump wants rates lower, and Powell won’t play ball. So, Trump and Bessent will find ways to work around Powell and add liquidity regardless. This is bullish for stocks. If there is some kind of panic and a dip in stocks in the meantime, they will turn on the fire hose. Back up the truck and buy the dip!

The TSE apply pressure to listed companies to improve their governanace and return capital to shareholders – it’s a great time to own Japanese stocks if you have a JPY base currency need! (not so great if you don’t, see above)

Every four years, Bitcoin goes down around 80%. Then it spends about a year floundering around and recovering slightly, and the next two years in a powerful bull market. If it goes down 80% next year, you swing like Happy Gilmore!

See how it works? Dumb money stays winning!

Have a great weekend.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I keep seeing posts declaring the 60/40 portfolio dead. No sh*t, Sherlock! Markowitz’s Modern Portfolio Theory dates back to 1952. I learned that 60/40 was no longer relevant in 2005. Where the hell have you been?

In case you are not familiar with it, the 60/40 refers to the traditional portfolio strategy that allocates 60% to stocks and 40% to bonds. The stock part aims for long-term growth while the bonds smooth out the volatility in rough periods.

Markowitz advanced this idea by blending a range of assets to produce a more efficient portfolio, recognising that the typical investor wants reasonable returns without excessive risk. See my post on Asset Allocation for more on this.

Can’t I just long equities?

Yes, it’s perfectly acceptable to just average into one or two stock ETFs and hold them for the long term, especially if you’re young. In fact, you can do that and read no further – you don’t need any help!

However, if you believe in passive investing and market indexing, which many people do these days, you must understand that the market encompasses more than just stocks.

Also, if you are investing a significant amount of money, it’s unwise to be 100% invested in one asset class, unless you have specific knowledge and overwhelming conviction. (which, by definition, a passive investor does not)

What’s a lot of money then? Great question! It’s different for everyone, but let me put it this way: If you are a passive investor, 100% in stocks, and you are starting to get concerned about the damage a market crash could do to your net worth, you might be getting close!

The funny thing about the 60/40 idea is that young people these days are probably already allocated 60/40, but to tech stocks and crypto!

Yeah, crypto, so where does that fit in?

This question is doing the rounds. If crypto is a new asset class, then where does it fit in a diversified portfolio? How big should the allocation be?

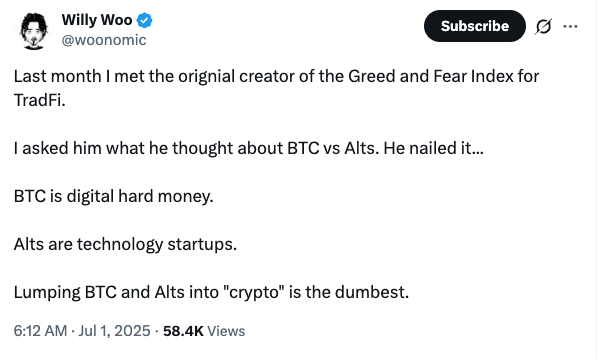

— The Wolf Of All Streets (@scottmelker) July 1, 2025

We can argue all day about whether the allocation should be closer to 10% or 40%. It clearly depends on an individual’s situation, risk profile, level of conviction, etc. The notable thing about this article is how it mixes up the whole Bitcoin vs. crypto terminology.

It mentions Bitcoin to start, but then it refers to crypto. So you should be putting 10-40% of your portfolio in what exactly? Bitcoin ETFs? Cryptocurrencies? Which ones? It’s not very clear.

I mean, they’re all the same thing, right?

Not even close! And ETH is the second-largest digital asset. Think how many coins have gone to zero since 2017! In my opinion, if you’re going to allocate part of your portfolio to this asset class, you need to get smart about it.

Here’s a pretty solid definition:

I’m not saying you can’t have mad conviction on a particular coin and hold it as an investment. If you have that level of certainty, then go for it. Hardcore XRP hodlers don’t care what I think, and they shouldn’t. They believe in the coin. But should the average investor put 10% of their net worth into it? Of course not!

The mainstream media are leading lambs to the slaughter if they can’t get their terminology straight.

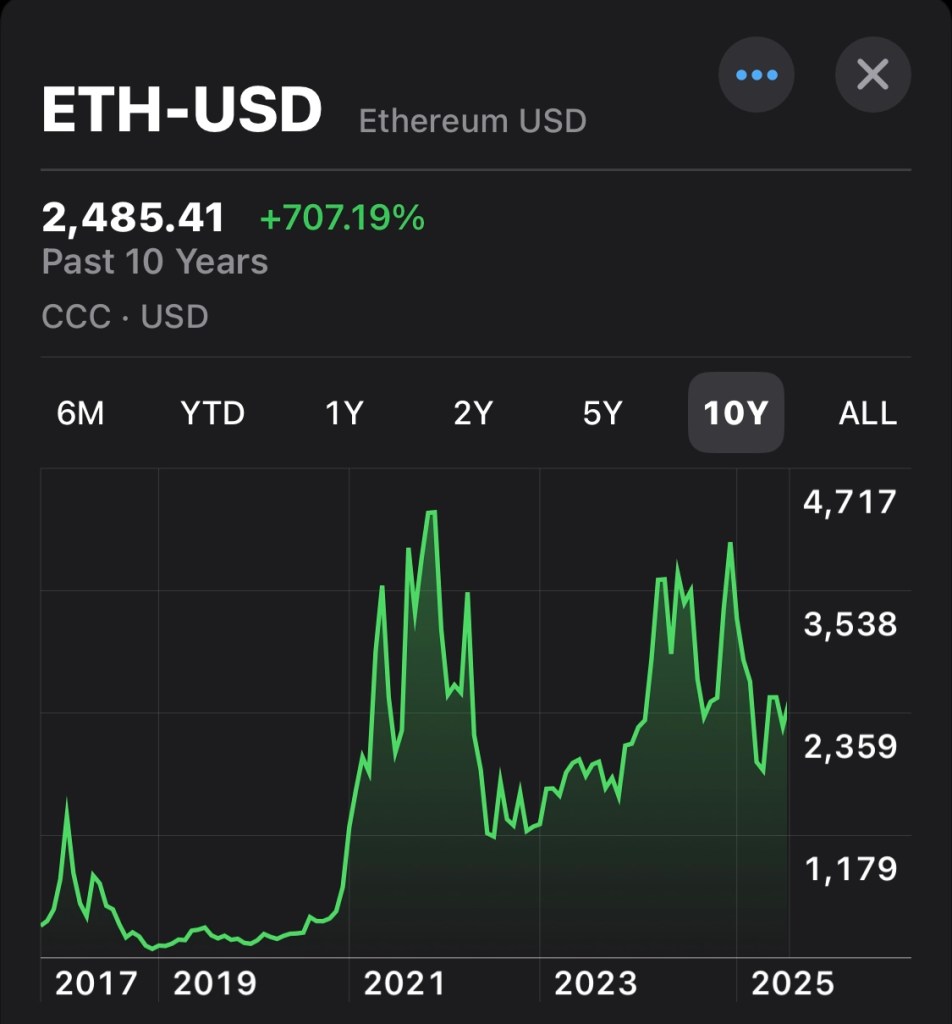

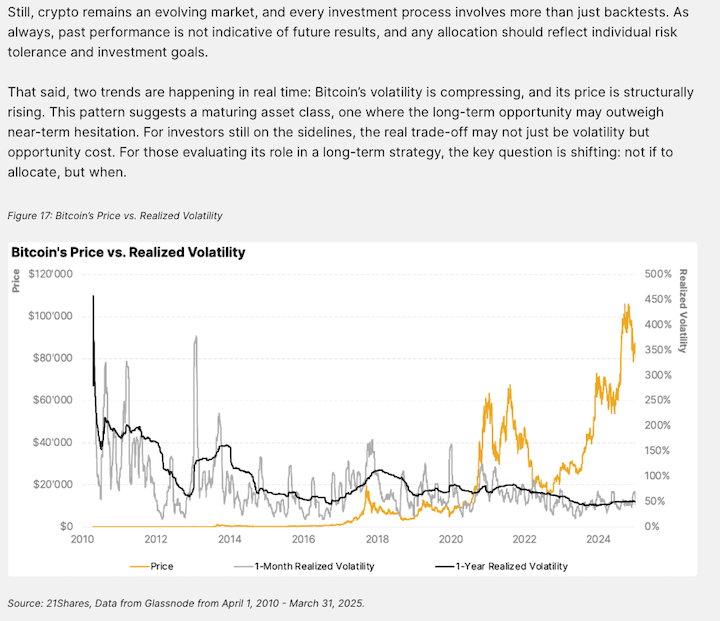

Here’s the only truly investable cryptoasset in my humble opinion. Doesn’t it look beautiful?

Uncorrelated assets for the win

The modern portfolio enhances 60/40 by adding assets that are uncorrelated or only lightly correlated to stocks and bonds. That’s how you achieve better risk-adjusted returns. (similar or better returns with less risk) Back in 2005, I never imagined a shiny new, uncorrelated asset would emerge. It really is a remarkable thing.

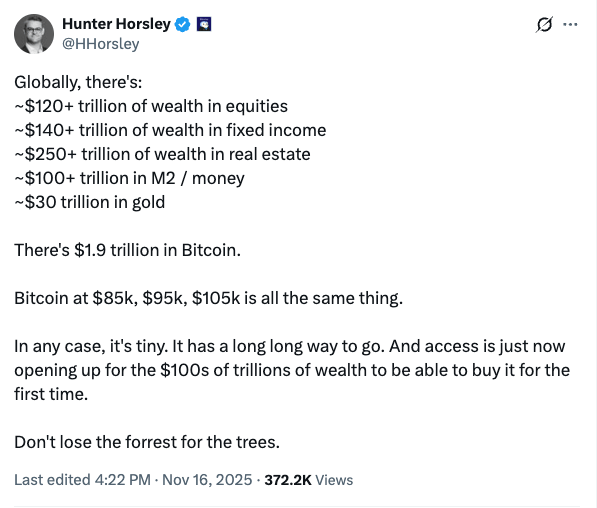

Here’s a quick summary: between April 2022 and March 2025, Bitcoin’s correlation to the rest of the asset universe was 36%. People like to compare Bitcoin to tech stocks, but its correlation to them was only 40%. These levels are significantly lower than traditional assets’ correlation to each other, which typically comes in at around 60-70%. This makes Bitcoin an ideal asset to add to a diversified portfolio in order to beef up returns without meaningfully increasing risk.

What makes Bitcoin especially interesting is how sometimes it behaves like a risk asset, like equities, and other times, it acts as a defensive asset, like gold. Over time, it is expected to become more of a gold-like store of value asset.

“This makes Bitcoin unlike any other asset in the market. It is structurally independent, behaviorally adaptive, and still offers significant asymmetric upside relative to legacy safe-haven assets. For portfolio construction, Bitcoin stands out as both a potential long-term hedge, and a high-impact diversifier at present.”

Adding a 1% allocation to Bitcoin to a modern portfolio over the 3 years resulted in stronger risk-adjusted returns. (It improved both cumulative returns and shape ratios)

Adding Bitcoin did not increase downside risk.

When scaling up to a 5% Bitcoin allocation, the risk-adjusted returns were even stronger, and the volatility remained manageable. Interestingly, they also tried a 3% allocation to the top 5 cryptoassets and achieved a similar uplift in performance without greatly increasing the risk.

So what’s the conclusion to be drawn here? You don’t have to go 40% into Bitcoin! Just a modest allocation increases portfolio efficiency without meaningfully increasing risk.

What are we trying to do again?

The whole point of investing is to beat inflation in your base currency. Doing it most efficiently with the least amount of risk is just being smart.

You can be overweight certain satellite holdings if you have a high level of conviction in them.

I still run a boring diversified portfolio, despite currently exceeding the recommended daily dosage of Bitcoin and Japanese stocks.

What’s my level of certainty?

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.