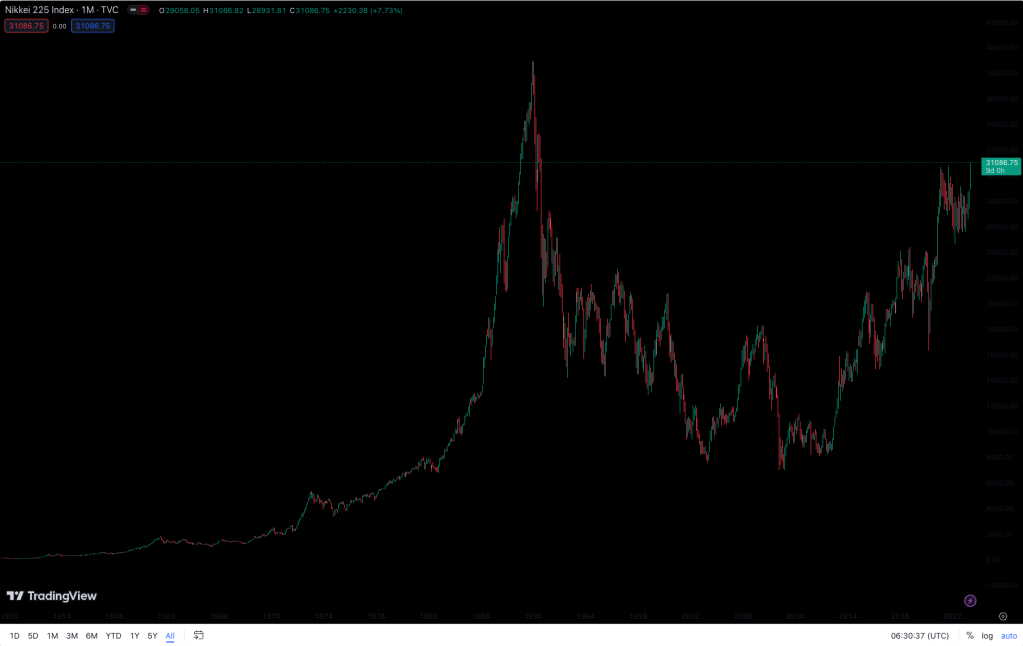

Japanese stocks have broken out, with both the TOPIX and the Nikkei 225 at levels not seen since August 1990. The inbound tourism revival is in full swing and foreign investors, including the great Warren Buffett, are pouring in. So is it too late to get involved?

After a volatile year for stocks in 2022 and a big drop in the yen, it feels like there is a lot of money sitting on the sidelines. And while ‘scared money don’t make money’, Japanese stocks have been quietly putting together a world-beating two quarters. Here is a selection of year-to-date performance numbers:

Nikkei 225 +19.1%, Toyota +7.5%, Honda +30.6%, Fast Retailing +26.7%, ANA Holdings +12.8%, Keisei Electric Railway +44.6%, Kyoto Hotel Ltd +9.25%, Panasonic +32.8%, JFE Holdings +17%, Marubeni Corp +31.4%, Hub Co Ltd +28% (yeah boiiii!), Japan Tobacco +16.6%, Takeda Pharmaceutical +10.8%, Yaskawa Electric +38.2%.

You get the picture. Japanese stocks are on a tear and not many people saw it coming. Not so the eternal Japan Optimist, Jesper Koll. I had to smile at the title of his recent post ‘We’re all bullish Japan now…’ I’ve seen countless bullish articles on Japanese stocks this last week – suddenly everyone is jumping on the train.

Jesper has of course been riding this train for some time and does a great job in his post of identifying the reasons for the surge in Japanese risk assets. If there’s one lesson that we all should learn from the past few years, it’s that liquidity drives markets. And as developed markets go, Japan is the last remaining source of cheap money. As the US and European central banks raise rates to fight off inflation, the Bank of Japan has, predictably, kept things very easy. There was a slight blip as a new governor took over at the BOJ and a host of people, who should know better, speculated that he would be forced into tightening monetary policy and blowing up the bond market just to fit their narrative. Ueda-san quickly put such rumours to rest and confirmed that policy will remain easy for the foreseeable future.

Jesper rightly points out other factors in the rise of risk assets in Japan: inflationary fiscal policy, a refreshing wave of pro-shareholder regulation, the expansion of NISA, increased business investment and a rising corporate metabolism. To that, we can add a few sector-specific catalysts: the weak yen providing a tailwind for exporters, Chinas’s economic reopening boosting commodities and shipping-related business, and the inbound tourism revival pushing up travel-related stocks.

However, none of this means much without that steady stream of delicious liquidity; mmmm zero interest rates and yield curve control are still on the menu!

A lot has been made of Berkshire Hathaway’s investments in Japan’s big five trading companies. And without wanting to diminish the fact that one of the world’s greatest living investors is buying in Japan, a lot of the coverage ignores the blindingly obvious: Warren pigged out at the last cheap money buffet in the world! He issued debt in yen at around 1% to buy quality companies that pay 4% income. It’s an exquisite arbitrage, but hardly a ringing endorsement of corporate Japan. If interest rates remain high in the US and low in Japan, you can bet he will be back. That man can’t turn a good deal down!

So, the big question is, if you don’t have much exposure to Japanese stocks already, is it too late? Once more it’s fascinating, and somewhat alarming, to see almost total consensus from commentators: the market is going to keep going up! I’m not one to fight the trend, but when everyone thinks one thing is going to happen it’s usually time to open your eyes to the exact opposite scenario…

Quoting Jesper himself here: ‘after more than thirty years, a positive break-out above the historic “Bubble Peak” of 40,000 on the NIKKEI stock index is finally becoming a realistic prospect over the next 15-18 months.’

So let’s be cautiously optimistic here, while keeping in mind the second part of Jesper’s post, what could go wrong? If you’re serious about owning Japanese stocks, I urge you to read the post yourself, but clearly, the number one thing that could derail this rally is inflation refusing to die down as expected, forcing the BOJ to take action on yield curve control and interest rates. My personal take on this is that any attempt to ‘normalise’ rates will be met with chaos and a hasty U-turn, but the damage will get done very quickly amongst the chaos. There’s obviously an argument here for long-term investors to ride out the storm and wait for the rebound, but I would prefer not to ride into that storm with too much JP stock exposure myself.

So if you own JP stocks already, enjoy the ride, but keep an eye on those inflation numbers and an ear to any rumblings from the BOJ. If you are planning on getting in now, then you are probably not too late but you don’t have a lot of cushion on the downside, so act accordingly.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.