Inflation has been on a lot of investor’s minds recently. Every time the Federal Reserve’s Jay Powell speaks he us under intense pressure to clarify his expectations for inflation, and how the US central bank would react to it. Amidst the ongoing re-opening of America, and indeed much of the world, inflation seems to be the one thing that could derail the stock market. The massive stimulus following the 2008 Global Financial Crisis was just in the process of being tapered when Covid-19 hit, and since then we have seen some $10 trillion in government stimulus globally. That’s already triple the total stimulus for the 2008-2009 recession. When national debts and the supply of money are increased at this rate, there is always going to be an effect on the value of money somewhere down the line.

Inflation can be defined as the rise in the cost of goods and services over time, but a better way to understand it is the decline of purchasing power of a given currency over time. Simply put, the same money buys you less and less.

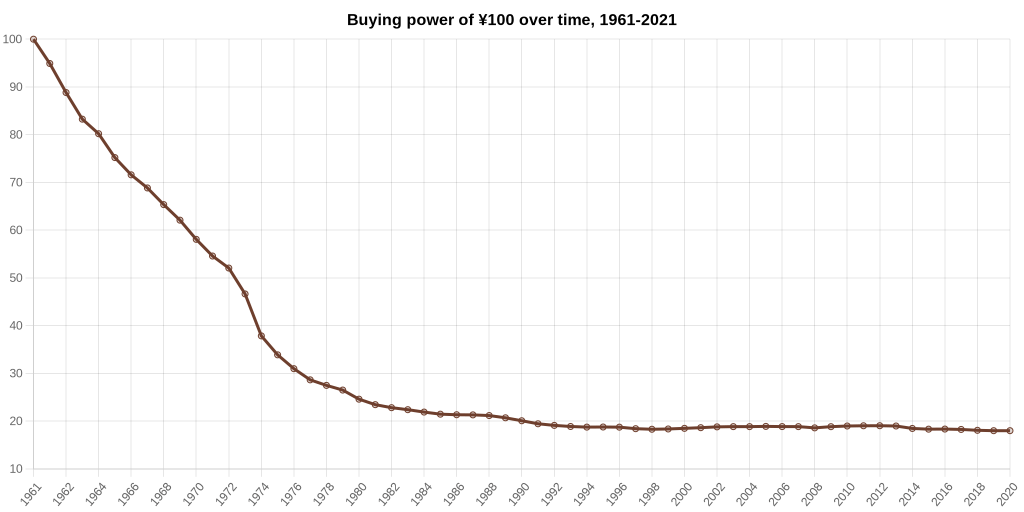

I came across this site, which is a great tool for understanding inflation. Take a look at the Japan Inflation Calculator and you can clearly see how brutal the effect of inflation has been on purchasing power here. 1 yen today is only worth 19% of a yen 60 years ago. And that is in a county that has been battling deflation for the last 30 years…

Japan’s example is a precursor to the ongoing debate as to whether the current scenario is inflationary or deflationary.

I recommend reading this excellent thread by Raoul Pal. Here’s an excerpt:

“In fact with global debts of all forms between $400 trillion net and $1.2 quadrillion gross – the collateral (assets) can NOT be allowed to fall or the system is wiped out. and so the merry game of systematic bailout MUST continue….”

What Raoul describes here will sound familiar to anyone who has been in Japan for a long time: interest rates held at zero and unable to rise, never-ending stimulus, wages stagnant. Official inflation is somehow measured at zero, but every year your money buys you less. What investors in many parts of Europe are facing is not only the devaluation of the currency, but also negative interest rates. Yes, for amounts over €100,000 depositors are paying up to 0.5% per year to keep their money in the bank. Imagine if that was implemented in Japan!

Raoul’s conclusion is that regardless of whether you sit in the inflation or deflation camp, the result is the same: the value of money is falling.

So where does that leave us? If we are working hard, earning as much as possible and trying to plan for our future, what should we be doing?

First of all, if your money is in cash, you are losing purchasing power year on year. If you want to escape this and maintain the value of your hard-earned money you need to invest. I don’t know any other way around this problem, other than making more money, which is great if you have a way to do so.

“Invest wisely. Bonds might be a one year trade but over 5 years you WILL lose. Most equities just allow you to stand still. Tech does better. Crypto much better. Real Estate is a stand still too (except super limited supply). The rarer the asset, the more it rises.“

I don’t disagree with Raoul’s quote above, however for a typical investor allocating to just crypto and tech stocks involves taking on way too much risk. Regardless of how each asset will perform over the next 5 years, diversification is the only way to protect yourself, whilst staying invested. I have covered the basics in numerous other posts: understand your risk profile, figure out your base currency, study up on asset allocation (also here), and, most importantly, take action! Sitting in cash is not a safe strategy over the longer term.

(This post on Japan inflation may be useful too)

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.