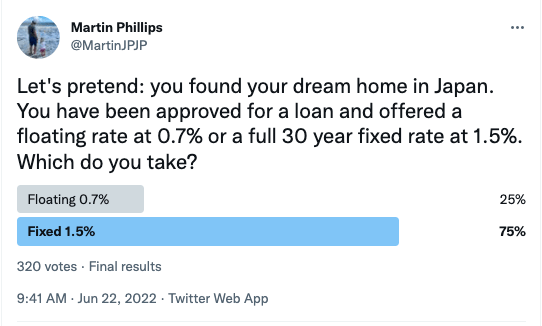

Things are heating up in Japan in more ways than one. Scrolling through Twitter I have recently seen a lot of chatter about what is happening to the yen and the Japanese economy, so I tried a little sentiment check and ran a Twitter poll as follows:

I was genuinely surprised to see fixed win this one so easily. Of course there is no wrong answer, and your choice depends a lot on your attitude to risk and overall financial confidence. However, there is also an element of prediction involved. Will mortgage rates increase in the years to come? If so, by how much? If rates pop up over 1.5%, you’re suddenly going to wish you had taken that fixed rate deal. A variable rate mortgage in the US is around 5.2% now and rising. Imagine that in Japan! Seven years ago, when we bought our house, my wife and I bit the bank’s hand off for a floating rate loan. No way were rates going up in our lifetime! I’m fairly sure we would still make the same choice now, but we would certainly think about it a little more…

So why the hesitation? Everyone knows that interest rates in Japan have been near zero for a quarter of a century, and raising them, even a little, would lead to financial chaos. Well, as the US and Europe are raising rates in order to fight inflation, suddenly all eyes are on the one country that hasn’t blinked yet. And right there in the spotlight is Haruhiko Kuroda, Governor of the Bank of Japan. Since his nomination in 2013, Kuroda has spearheaded the BOJ’s loose monetary policy and, despite accusations from the west of deliberately weakening the yen to favor Japanese exporters, he has always maintained that his policy goal is the break out of deflation by targeting the magic 2% inflation level. In pursuit of this target the Bank of Japan has employed both quantitive and qualitative easing, meaning it has not only purchased vast quantities of government bonds, but also stocks and REITs. 2016 saw the start of yield curve control and negative interest rates. Yes everything but the kitchen sink has been thrown at the deflation problem and guess what? It finally worked!

You would think that reaching the holy grail of 2% inflation (actually it stands at 2.5% right now) would be greeted with celebrations, however over the past 25 years the Japanese populace has gotten rather used to things staying much the same price. Wages have also remained stagnant, making people rather sensitive to price hikes, as Kuroda himself found recently after remarking that households were “becoming more accepting of price rises”. The rebuke from the public was swift and clear: times are tough in the households of Japan.

And so the global media has begun to speculate over what comes next. The rise in rates in the US in particular has made the yen less attractive and it has quickly slid as far as 136 yen to the dollar, a 24 year low. What’s more, Japanese bond yields have been surging, with the Bank of Japan deploying vast amounts of money to defend its 0.25% yield curve control target. It appears that Kuroda-san can save the bond market or the yen, but not both. Given the massive JGB holdings held in pensions alone, you can bet it will be the bond market.

Now it’s being reported that a $127 billion hedge fund called BlueBay is attempting to pull a Soros by attacking the BOJ’s yield curve control position in an effort to force it to adjust its monetary policy.

It all sounds a little scary, doesn’t it?

It is not, however, the BOJ’s first rodeo. Betting against the central bank has long been known as the widowmaker trade. And many widows have been made in the last 20 years. It turns out that bringing a knife to a bazooka fight is not a smart move.

Japan’s debt to GDP is estimated to be around 248%, the highest in the world. Proponents of Modern Monetary Theory (MMT) will argue that as long as the fiscal deficit spending leads to an increase in the share of GDP retained by households, the funding of the debt is not an issue. However, who trusts the government to make sure the money ends up in the right places? After all, this is the country that just spent 1.42 trillion yen on the Olympics. How many households felt the benefit of that I wonder? And what is the the next sector up for a big spending spree in Japan? Defense…

So can you really just keep printing more money to pay back the debt? It looks like we are going to find out at some point, but we may be surprised how long this seemingly unsustainable status-quo can be maintained. Fresh after making a killing betting on the European debt crisis a decade or so ago, Kyle Bass turned his attention to the widowmaker trade, memorably declaring investing in Japanese stocks as “picking up dimes in front of a bulldozer”. However the bulldozer still hasn’t rumbled into town and Kyle has moved on to other trades. Inflation at 2.5% hardly calls for drastic action when the US is at 8.5%, but that can change.

So if you have a floating rate mortgage can you relax for now? Most likely yes, you have nothing to worry about in the near future. The BOJ is clearly ready to do whatever it takes to keep rates where they are. At some point further down the line though, that could lead to a continued weakening of the yen, which in turn would bring a rise in “imported inflation” as the cost of foreign goods would continue to grow in yen terms. If that gets bad enough then something drastic will have to be done…

In the short term, a drop in inflation later this year would certainly take the pressure off Kuroda-san somewhat, and Jerome Powell too for that matter!

Let’s all hope “This is fine”…

My Twitter poll, of course, only offered two options and, as people rightly pointed out in the comments, you can mix fixed and floating rate mortgages. 10 years fixed and floating after that is quite typical in Japan. If you do have a floating rate, it is always a good idea to save up money separately so you have the option to pay the loan off quicker if rates were to rise. For fixed rate mortgages you can also check if you are eligible for Flat 35.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.