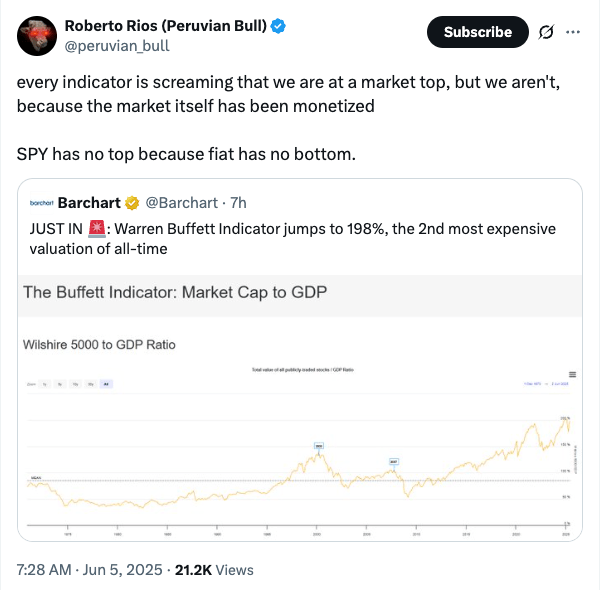

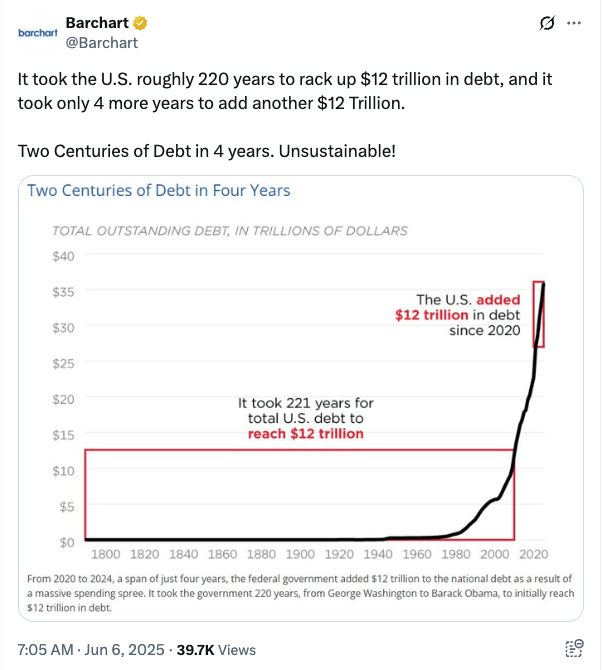

I am starting to see people discussing the idea that the stock market has been so pumped up on debt steroids that it simply won’t be allowed to go down for an extended period again. Normally, this kind of talk would be a massive flashing sell signal, but it’s not an idea that is being broadly discussed. It’s just popping up in pockets here and there.

Of course, stock markets go up and down. In fact, the mighty US market took a hit in April due to the Liberation Day tariff malarkey. But did you notice how quickly it bounced back? Pretty much a V-shaped recovery. Same in March 2020.

I’ve said it before: the money has been funny since the 2008 global financial crisis. Many institutions that should have gone under were propped up at the expense of taxpayers and we’ve been getting screwed ever since. Economies and big business have become addicted to liquidity.

Sounds like tin foil hat stuff?

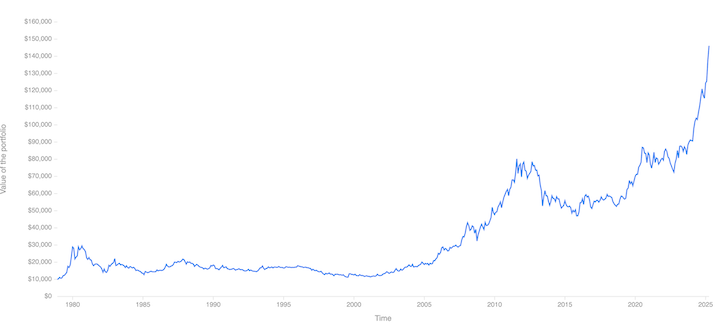

That’s the MSCI World Index. See what happens after the 2008 crash?

Here’s the gold chart for comparison.

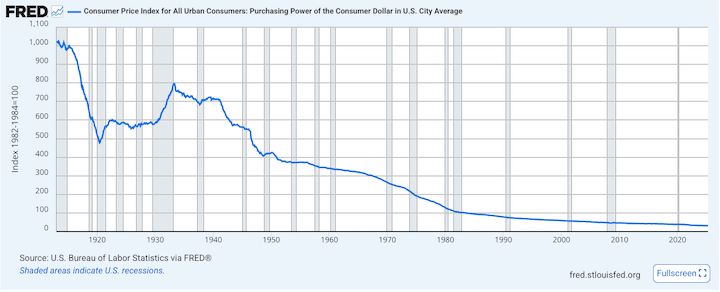

So, are the assets going up, or is the unit of account going down? Check out the purchasing power of a dollar over time.

Ding ding ding ding ding! So, 2008 clearly wasn’t the start of the pattern. It just intensified after that.

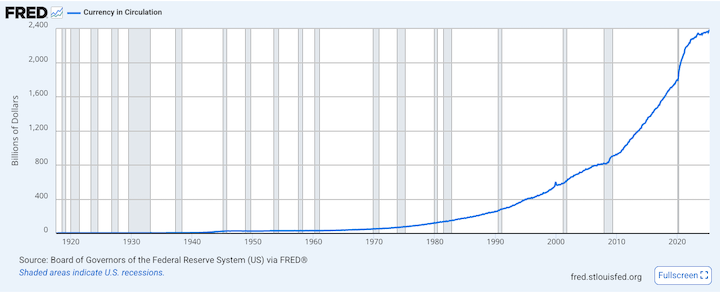

The Federal Reserve of St. Louis puts together some pretty charts, doesn’t it?

Take a look at this one – currency in circulation:

Hello! So, if you keep creating more dollars, the purchasing power of a dollar goes down, and the value of assets and other stuff goes up against your inflated currency. I’m picking on USD here, but everywhere else looks the same. Probably worse.

Here’s a question I get asked a lot: “How do I convince my very conservative partner that we need to invest more?”

Answer: Just teach them that the market is going up forever!

If assets are going up forever, you’d better own some! You probably don’t need to fret too much about timing the market. Just make sure you keep a nice cash reserve so you don’t have to dip into your investments in a crisis, and yolo the rest into stocks, commodities, real estate, bitcoin and anything else that isn’t cash in the bank.

Of course, this is all somewhat tongue-in-cheek. But is it really much more complicated than that?

Please don’t misunderstand. Stocks can still go down 30-50% at any time. Bitcoin can still dump 50-80% and probably will next year. You should be prepared for these outcomes and never let yourself become a forced seller. But, over the long term, these assets go up and to the right because the denominator is cooked. Did you notice how long the whole DOGE ‘let’s reduce wasteful government spending’ drive lasted? It’s not even June, and Elon and Trump are melting down in public.

If you’re wondering why you have to become a money manager just to break even with inflation, here you go:

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

“It never was my thinking that made the big money for me. It always was my sitting. Got that? My sitting tight! It is no trick at all to be right on the market. You always find lots of early bulls in bull markets and early bears in bear markets. I’ve known many men who were right at exactly the right time, and began buying or selling stocks when prices were at the very level which should show the greatest profit. And their experience invariably matched mine–that is, they made no real money out of it. Men who can both be right and sit tight are uncommon.” – Jesse Livermore, in Edwin Lefèvre’s “Reminiscences of a Stock Operator”

We are so back!

Little more than 6 weeks after Donald Trump nuked markets with his “Liberation Day” blusterf**k, stock indices are right back where they started. Congratulations on surviving! The circus is far from over, but it feels like we just went through boot camp on how to operate under this administration. My personal goal from now on is to ignore every word the man says and focus on what actually gets done. There is way too much noise!

Anyway, check in on the doomers. They probably need to come out of the bunker, touch some grass and catch some Vitamin D.

The great dealmaker is in Saudi Arabia now, doing deals, I presume. Note the presence of Nvidia’s Jensen Huang among the tech CEOs there with him – I would not bet against that company to emerge from the chaos stronger than ever.

So what’s going on?

Checking on the news, Nvidia isn’t the only AI/semiconductor play catching a bid. Advantest, Tokyo Electron and Disco are all perking up too.

Softbank Group is also on the rise after posting its first full-year profit in four years.

Department store operator Mitsukoshi Isetan announced an expected net profit of ¥60 billion for the current fiscal year, up 14% year-on-year. Those tourists must be spending hard while we plebs struggle to buy rice!

Things don’t look so rosy for the Japanese auto industry, though, with Honda and Nissan crumbling under the uncertainty around tariffs. There is more than tariffs at play here as both have struggled with sales in the US and China. The two companies abandoned plans to join forces earlier this year and who knows where they go from here. Nissan is clearly worse off and will shut 7 vehicle plants and cut 20,000 jobs globally.

Come for the global recession fears, stay for the long-term debasement of the yen!

USD/JPY is back around ¥147 after the BOJ needed a breather from raising rates. If they are planning to wait for some respite from global economic uncertainty before hiking further, we will be back in the ¥150s soon.

Wakey wakey

“If you own crypto, I can’t stress this enough: the best thing you can do is go to sleep for about 3 months. Block out the noise.” – I wrote this in my opening post of the year in January. There have been many dips and ‘it’s so overs’ since then, and yet here we sit in mid-May with Bitcoin back over $100k.

It’s probably time to start paying attention again. Metaplanet is creeping back towards the highs. I sold half of my holding in the run-up in Jan/Feb, and it’s looking like time to start averaging out the rest. Maybe take out half in the next few weeks and save the rest for Valhalla?

Even Ethereum has woken up!

Alts have been battered in the dips. With a tidal wave of ETF inflows, BTC dominance shows no sign of slowing down. Alt holders would like to see the orange coin break the all-time high and then chill for a while. Will they get their alt season? The exit is narrow and it won’t be open for long…

Where does BTC top? Gun to my head, I say we get a run now, followed by a quiet summer, then one more assault on the summit in autumn.

However, if you are looking to take profit, don’t listen to me or any other people on the internet. Nobody knows anything. The smart money is scaling out already. Execute your plan.

If you are a long-term BTC investor, and for at least part of your stack you should be, all you gotta do is sit tight!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s been a long week. Is it me, or are +/-9% swings on the Nikkei 225 index starting to feel normal? Traders must be loving this – at least the good ones.

I’m not so impressed. Of course, there are buying opportunities, but it gets a bit tiresome when markets swing this wildly based on the pronouncements of one guy who just can’t STFU for 5 minutes.

Click it, I dare you! And don’t get me started with the Simpsons memes.

Where was I? Tapping the sign, right. The free lunch quote has been attributed to Harry Markowitz, although I have heard Ray Dalio say something similar. It’s a drum I have been banging for years, sometimes with minimal effect.

When the stock market is going up, nobody cares about diversification. Why would I want to own bonds and gold and other stuff when stocks are on a tear? Just buy the index and chill, right? It’s easy to forget that stocks take the stairs up and the elevator down.

Until you get a reminder.

In 2002, psychologist Daniel Kahneman won the Nobel Memorial Prize in Economic Sciences for his work on the psychology of judgement and decision making. Kahneman points out that individuals are more depressed with investment losses than they are satisfied with equivalent returns. In other words, people hate losing money considerably more than they like making money.

Big liquidation events are like waking up after a party. It was fun, but now it’s time to sober up and review your time horizon, risk profile and asset allocation.

Are you diversified enough?

If recent events haven’t troubled you, and you have barely looked at your investments, the answer to this question is probably yes. Carry on!

If things have been a little nervy, then maybe you were over-exposed.

Don’t get me wrong, I’m all for buying stock indices and holding them forever. It’s not a bad strategy, as long as you can stomach the downturns. And as long as you don’t need the money soon. And, it’s not like a diversified portfolio doesn’t go down in times like these either. When panic sets in, people will sell anything they can get their hands on, but pretty soon you will see a flight to safety.

An underappreciated aspect of diversification is the opportunity to tactically rebalance and take advantage of market events. I sold some of a gold ETF this week near all-time highs and bought stocks while everyone was puking them. I didn’t need dry powder. Just a little reallocation.

You can’t do that if you don’t own the gold in the first place. You have to find more cash.

A quick thought experiment

If you are reasonably young and earning good money, then the recent market gyrations are just a blip, but do me a favour: imagine you are 65 years old, about to retire, with a nice fat nest egg invested in the MSCI World Stock index.

And the market dumps 20% in a couple of days. It takes a breather over the weekend and then resumes dumping in earnest. 30% of your retirement pot is gone. Financial media is screaming about recession, trade war, deleveraging or whatever it is this time. Remember in March 2020, when the market crashed and we faced the reality that the entire world was about to shut down? The doomer economists are running victory laps, and the market looks like it is never coming back from this.

How do you feel?

Remember that feeling when you are making future investment decisions, especially as you get closer to spending the money.

Of course, what happened after March 2020 was that central banks slashed interest rates and unleashed a tidal wave of stimulus, and the markets came roaring back before the year was even over. But that type of thing comes at a cost – that’s why your hard-earned cash doesn’t buy as much stuff any more…

Ok, so how do we do this diversificationthing?

There are various ways to get yourself a diversified portfolio. How hands-on do you want to be?

For the people who want to put as little effort as possible into it, you can simply buy multi-asset ‘balanced’ mutual funds. I recently came across a collection of Japanese funds that are divided up by age group: “Happy Aging 40”, “Happy Aging 50”, “Happy Aging 60”. The allocations get more conservative the higher the age. These types of funds are available everywhere. Simply dump your money into the fund that fits your time horizon and get back to whatever you’d rather be doing.

In my advisory business, for larger chunks of money, I recommend professionally managed investment portfolios fitted to the client’s base currency and risk profile. Yes, they cost more than an ETF, but they are incredibly well diversified. The asset allocation is reviewed annually, and every quarter the managers implement a ‘tactical overlay’ and buy more of the assets they like and sell some of those they don’t. These guys don’t just buy a broad stock index – they are breaking equity holdings down by style: value, growth, small/large cap, etc. Of course, the entire portfolio is rebalanced annually.

I also recommend a core/satellite approach for even broader diversification. That’s how you slot in the algorithmic trend following strategy that trades stocks, interest rates, currencies, metals and other commodities with very little correlation to any one market. Funnily enough, it likes volatile times like this.

For coaching clients, I take the knowledge I have gained from watching professional money managers and help them develop their own asset allocation using low-cost ETFs. Click the coaching link to find out more.

Keep it simple

Here are a few action points if you want to take on this job yourself:

Separate regular and lump sum money. Regular is the money you invest every month in a pension, savings plan or Tsumitate NISA. If you are relatively young, you can just allocate all of this to stock indices/funds. Let Dollar Cost Averaging do the work for you.

Lump sum money is a chunk of cash you have saved up that you are looking for a better return on. Here, you are going to want more diversification, and you should focus on the currency you are most likely to spend the money in (your base currency). The asset classes you want to look at are: cash, domestic (base currency) bonds, overseas bonds, domestic stocks, overseas stocks, property, and commodities. Hold more stocks if you are young, and more bonds and cash if you plan to spend the money soon. Allocate 70-80% of the lump sum to this broad portfolio, and the remainder can go into satellite holdings to beef up the areas you are most bullish on. For example, if you like Bitcoin, that’s a great satellite holding.

If you are gonna get really serious though, you are going to want to diversify your bonds.

Peace out!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

With markets looking a little shaky of late, it’s worth remembering the old saying that time in the market beats timing the market. With Warren Buffett once more making news in Japan this week, this post and Bullish Batman’s comment tickled me:

I think readers of this site will have at least a basic understanding of the benefits of compounding on investments. That said, it can take some time to actually experience its power. I have noticed that one of my accounts, which started small and took a while to grow, has picked up momentum in the last 12 months. I haven’t added new money to it for a while but have been diligently reinvesting capital gains and dividends, resulting in a significant acceleration in growth.

Here’s the Investopedia definition of compounding:

It’s a great reminder that, although short-term price moves make headlines, we should focus on investing for the long term. Accumulate good assets and hold onto them!

Is Uncle Warren coming back?

Warren Buffett has mastered the art of buying quality stocks and allowing them to compound over the long term. In his recent letter to shareholders, the Berkshire Hathaway CEO commented that he is keen to increase his investment in Japan’s big five trading companies. You may remember that Buffett has been playing a very smart game in Japan, issuing debt at around 1% in yen to buy solid companies that pay around 4% income. Shares in those trading companies surged this week in anticipation that Buffett may be coming back for more.

Despite The Oracle of Omaha’s endorsement, the trading houses still face significant headwinds related to yen movements and Donald Trump’s tariff policies. The US President’s aggressive stance on that issue is unsettling for companies that rely on smooth international trade. It doesn’t seem to worry Buffett too much, though.

Speaking of the yen, on 25 February it hit a four-and-a-half-month high of ¥148 to the dollar. With inflation on the rise, the Bank of Japan will come under pressure to continue to raise rates while the US Federal Reserve has rate cuts on pause for now.

The Corolla index reaches 50%

This is new to me, but this Nikkei Article refers to a Toyota Corolla index. It measures the affordability of a typical mass-produced Japanese car by dividing the price by the average annual income. During the good times, it has been as low as 20% but currently stands at a whopping 50%. For comparison, in the US it is 30%.

This clearly illustrates that, although wages are rising, they are failing to keep pace with inflation in Japan.

Nvidia beats on earnings again

In the US this morning, Nvidia might well have saved markets from severe pain, at least in the short term. The chip powerhouse once more beat analyst’s expectations and issued solid Q1 guidance. The company reported Q4 revenue of $39.3 billion and expects $43 billion plus or minus 2% in Q1. Shares were up +3.7% in anticipation of the report but are down in after-hours trading.

It seems to take a lot to get investors excited these days. Trump is talking about a 25% tariff on chip imports and the AI behemoth is still weathering the DeepSeek storm. You may remember that Nvidia’s previous earnings also beat expectations but the stock fell afterwards.

Is the US economy slowing?

Despite the S&P 500 trading near all-time highs, sentiment in the US is increasingly muted. The downbeat mood is generally attributed to Trump’s tariff talk, however, in this Yahoo Finance article, Neil Dutta argues that it is more likely because the US economy is slowing down. He points to weaker economic data coupled with the Fed’s pause on rate cuts acting as a “passive tightening of monetary policy”.

That argument makes a lot of sense and could also explain why, despite a slew of good news, Bitcoin failed to break back above $100k and has now broken down instead. People who have been ‘waiting for a dip’ are not so keen now they have one. We may have to endure some economic pain to push the Fed to start cutting again before the bull market resumes. (no, I don’t think it’s over)

Also, it’s notable that hedge-fund manager Steve Cohen recently struck a bearish tone for the first time in a few years. You can see a snippet of his interview here. (in case the embedded link below doesn’t work)

Sounds like this is a time to be cautious: cash, bonds, defensive equities with low valuations pic.twitter.com/FCZqCSMvFD

— Michael Fritzell (Asian Century Stocks) (@MikeFritzell) February 24, 2025

Cohen states that he isn’t expecting a disaster, but things could be difficult over the next year or so, and it wouldn’t surprise him to see a significant correction.

All the more reason to keep a long-term view and focus on compounding those assets over time!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I started this site in 2017 and ran out of things to say about the basics of financial planning some time ago. If you are just getting started, I put together a thread of simple financial planning tips from my early posts, which you can view on X here.

The basics don’t change, but the environment can change drastically. If you plan to live in Japan for the long term, you are probably now figuring out how to adjust from living in a country where deflation was the norm to one where prices are rising. Looking into the future, one of the big questions is whether this inflationary environment will stick, or will Japan be back at zero interest rates and falling prices in a few years? How can we plan when we don’t know the variables we will likely deal with?

Prediction is very difficult, especially if it’s about the future. – Niels Bohr

I have a client who was an economist at a financial institution for many years. He told me he always felt it was his job to have a view. For some reason that has stuck with me and I think it is important in my job too. It’s also important not to be wrong, though! I wish I could tell you I have always held the correct view and never been wrong, but I doubt you would believe me. I have, however, gained some experience over the years, which has helped me develop some skills in dealing with the uncertain future we face.

Strong views, loosely held.

Having a view is helpful but you don’t have to marry it. If something changes or evidence comes to light that proves you wrong, you can simply change your view. Don’t get caught up in the social media battle to be right about everything. In just the last few years, people have pivoted from being epidemiologists to vaccine experts to geopolitical analysts to macroeconomists to AI gurus and now, tariff experts.

It’s exhausting.

So, I thought today I would take a look at some basic data about the Japanese economy and share my view on what a person living here should focus on in terms of financial planning and investment.

Debt is a problem

Japan still has a strong, productive economy but it is not expected to grow fast. The predicted real GDP change for 2025 is 1.1%. (IMF) Government debt to GDP is currently 255%. (Trading Economics)

December 2024 CPI (inflation) was 3.6% and, in response, the Bank of Japan recently increased the overnight interest rate to 0.5%. The 10-year yield on government bonds currently stands at around 1.2%.

Japan is clearly not going to grow out of its debt problem. Demographics do not support the level of growth required to meaningfully reduce the size of the mountain. When governments can’t outgrow their debt, they usually end up inflating their way out. I struggle to see how the BOJ leadership can raise rates high enough to head off this outcome but they will of course delay it as long as possible.

It doesn’t look good for the yen

In January 2023, I wrote a post charmingly titled How screwed is the yen? It actually holds up pretty well for a two-year-old post. The problems facing the currency have not changed very much and we are still hanging around at 155 yen to the dollar.

I have re-read this excellent post by Richard Katz several times: The BOJ, the Fed and The Future Of The Yen. He notes that although the gap between US and Japan overnight rates may close, the gap between the two countries’ long-term yields is unlikely to follow suit, meaning the yen probably won’t recover as strongly as some think it will. Here’s an excerpt from that piece:

Some of the issues people in Japan are facing when planning for their financial future are as follows:

Continuing yen weakness

Concern that the pension system will not meet their retirement needs

Rising interest rates, but not rising too far

Negative real rates (interest rates lower than the rate of inflation)

Rising wages but negative real wages relative to inflation

People are already feeling the pinch. If you bought rice recently, you know what I mean. Furthermore, prices of 1,656 food items are set to rise this month according to this Japan Times article.

So, what can we do?

If you are a regular reader, I am probably repeating myself, but here are some action items to consider:

Check your base currency – are you really going to spend all of your future money in Japan? Are there big expenses overseas that you are likely to be on the hook for in future? If so, you need to save and invest some or all of your money in that currency. More on that here: What is your base currency?

JPY cash is trash – even if your base currency is yen, you are going to lose against inflation over time if you keep all of your money in the bank. Sure, you need to keep a liquid emergency cash reserve, but everything else needs to go somewhere more productive. CPI was 3.6% in December. The BOJ’s target inflation rate is 2%. How much is your bank paying you in interest?

Fill up tax-free vehicles first – another no-brainer. If you are eligible for NISA and/or iDeCo, they are the first stop for investment money. NISA especially is an incredible deal as you can access the money freely if you really have to. Bad luck if you are a US citizen – you should explore options for investing back home. And remember, if your spouse is eligible, they should be maxing out tax-advantaged options, too.

Yen-cost average – if you are young, regular investment in a global stock index fund/ETF is a perfectly good strategy. You can worry about diversification later.

Learn to diversify – lump sum investments require more care. And the closer you get to spending your capital, the more you need to protect it. Diversification across asset classes (not geographical areas) is how you do this. Own some bonds, stocks (growth, value, dividend), property (physical or REIT), commodities and alternatives. Use a core/satellite allocation to dial up/down risk.

Lever up – if you are here for the long run, owning property is still better than renting. Even if you are risk averse, I am still seeing 35-year fixed-rate mortgages at under 2%. Floating rates are still well below 1% and, in some cases lower than 0.5%. It is still very cheap to borrow money for a home in Japan.

Stack gold and bitcoin – the two kings of hard assets and possibly the only satellite holdings you need. Average in over time and hold. More here: Facing inflation – the four assets you should own

A fistful of dollars – if you are the entrepreneurial type, I recommend brainstorming ways to earn money in USD. As the global reserve currency, it will be the last one standing in the Fiat race to the bottom. Read up on the dollar milkshake theory. If you can get paid in bitcoin, even better!

To summarise: have a view, make a plan and adjust it as you go. If you need help, don’t be shy about getting some. You will get better at this with practice.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Being a financial planner by trade, I try to organise our financial future as efficiently as possible without going overboard. My wife and I both work and we have a reasonable income. We have a plan, we know what our numbers are for later in life and the big events in between. Most of all, we are flexible in that plan – our core investments are set and forget, but they can be adjusted easily. The tactical stuff is fun for me and I see it as a bit of a challenge.

Of course, things can go wrong: ill health, accidents, economic change and shifts in specific industries. You prepare for these as best you can and get on with living. Eat well, exercise, look both ways crossing the street, buy insurance etc. etc.

However, there are a few bigger things that bother me. I don’t think about them all the time, but they lurk in the back of my mind. For example, I don’t think AI is going to take over my job, but it could change the world considerably – gotta keep up with developments there. I could classify these things as outliers and conspiracies. Some may or may not have a meaningful impact and others feel a little ‘out there’. The best conspiracy theories have an element of truth, though, don’t they?

So, here are a few things I think about and how they relate to money, investing and how big your number should be:

Climate

I must confess, I don’t allow myself to dwell on what we are doing to the planet. We are clearly having an adverse impact and most of the damage is being done by big business interests who will not stop. The paper straws are cute, but they are hardly going to offset the widespread burning of fossil fuels and other environmental destruction. It’s not that I don’t think it’s important – it’s crucial to our survival as a species. I just know there isn’t much I can do about it. I separate our garbage, cut down on plastic and try not to waste resources, but I’m not losing sleep. Half the people in the developed world don’t even believe climate change exists so good luck to us coming together and taking action as a species. Do you remember the Covid mask and vaccine debates?

It is certainly getting hotter though! And it’s hotter for longer than it was before. After 27 years in Japan, it’s noticeable how spring and autumn are shrinking while summer gets longer year by year. What’s that going to be like in 10 years? How about 20?

I hardly think Yokohama will become unlivable in our lifetime but it could become pretty unpleasant. Imagine Japanese summer from April to October! Would that change your planning? Could it mean your ‘number’ needs to be bigger? The ability to escape Kanto, and maybe even Japan, for several months a year could become a key lifestyle choice. Maybe some people will want to escape for good. Wouldn’t that mean that the cooler, more livable climates in the world are going to see an influx of people who can afford to move? Parts of India are already hitting 50°C as a matter of course. That kind of temperature is more manageable in the developed world with aircon but doesn’t higher demand for a cool place mean higher prices?

As we move from climate change to climate crisis, how are governments going to address it? Again, remember Covid? It was all the people’s fault that it was spreading. They had to be stopped from travelling and confined to their homes in some countries.

Climate lockdowns anyone? Do you think they won’t do it?

It’s a dark thought, but people with flexibility financially will fare better than those who are struggling for money. Does that change your number?

Japan’s economic decline

Honestly, this one would bother me more if I was younger. I’m not sure Japan is a place I would be trying to build a life, career or business given the demographics and the economic outlook if I was in my twenties. But I’m not that young any more and I’m happy where I am. I would, however, want my kids to have the opportunity to live and work overseas if they choose.

The yen is a major concern though. My view is that short term it should recover somewhat when America begins cutting rates. I can see it getting to ¥130 or even ¥120 in the next year or so. However, longer term I expect the yen to steadily lose ground, particularly against the dollar. I talked about it in my ‘How screwed is the yen?’ post a year and a half ago. Staying alert for opportunities to earn in other currencies, investing in a combination of domestic and overseas assets and accumulating Bitcoin remain priorities for me.

Financial shenanigans

Grab your tinfoil hats for this one! In simple terms, the money has been funny since the 2008 global financial crisis. A lot of institutions that should have died were propped up at the expense of taxpayers and we’ve been getting screwed ever since. Economies and big business have become addicted to liquidity: cheap money, low rates. Low interest rates foster inflation, which is a tax on us all, but especially a tax on people who do not own financial assets.

Countries have too much debt and are not producing enough to pay it back. Japan is perhaps the worst offender, at least in the developed world. The debt spiral is probably terminal. That’s why the yen is doomed, and after that so are the pound, the euro and the dollar. I covered currency debasement in ‘Harden up your assets.’ There are tools to fight it that need to be deployed. Otherwise, your money buys less and less.

This is why governments are getting interested in the idea of Central Bank Digital Currencies. (CBDCs) At some point, they are going to need to perform a reset and substitute the current failing money with an alternative. And the powers that be never want to waste an opportunity to seize more control.

In essence, CBDCs are just another form of fiat money. But they come with a whole new opportunity for manipulation. Here’s an interesting video of Rishi Sunak being asked how he would enforce national service in the UK:

Controlling ‘access to finance’ is a government wet dream and CBDCs will make it easy. If you think that the possibility of losing permanent residence due to unpaid taxes is bad, wait until they freeze your bank account or apply a negative interest rate to your money until you pay up.

The public is sleepwalking into this one. You can already imagine how half the population won’t have any issue with it at all. ‘If you don’t have anything to hide, why would you need to keep your money private?’ will be the refrain. People who are well off have no concept of how less fortunate people can run into money trouble and fall behind on bills and taxes. The rich just don’t want to pay for a bunch of ‘layabouts and immigrants’.

The Bank of Japan already has a page on its website about Central Bank Digital Currency by the way. Cute, huh? No plans to implement it at present, but they are looking into it…

CBDC is one thing I think is really worth fighting against, but it will most likely be a losing battle. Sooner or later some crisis will come along and CBDC will have to be implemented ‘for our protection’. You can already see it happening with the AML/CFT mission creep.

Call me crazy, but I think that accumulating Bitcoin and other crypto is the best we can do to prepare for what is coming. Any money sitting in the fiat system will be caught in the net. In many countries, people who want to withdraw a few thousand dollars in cash already have to explain to the bank what they are planning to do with it.

Assuming the number will go up

So there it is. Like you didn’t have enough to worry about! From a financial planning perspective, my take on this is that whatever your number is, you will probably need more.

That’s to say, whatever amount of money you think will be enough to secure your future, maybe add another 10-20% for safety.

This is why I recommend dividing investments into core/strategic and satellite/tactical. The long-term strategic investments are focused on hitting the number. The tactical assets are aiming for a little extra. The crypto holdings are a shot at f**k you money.

Number go up. Act accordingly.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Of the six main asset classes, the one that stands out as perhaps the least understood is bonds. Although most people have a general idea of what bonds are and how they fit in an investment portfolio, they are incredibly complex financial instruments and misconceptions abound. I frequently hear people wonder if there is even any need to own them. So, let’s take a look and see if we can get a clearer picture of how bonds work and why they are useful.

Why do bonds exist?

Bonds are used by governments and corporations to raise capital. If a government issues a bond, it is borrowing money from the public to finance itself. Companies issue bonds so that they can expand operations or fund new business ventures. So if you buy a bond, you are loaning a government or a corporation money.

The key components of bonds

Issuer: bonds can be issued by governments or corporations. Each issuer carries a different level of credit risk, with bonds issued by developed world governments considered the safest. Bonds from issuers with a lower credit rating carry more risk of default and pay a higher yield to compensate for that risk.

Coupon rate: this is the annual interest rate paid to bondholders, expressed as a percentage of the bond’s face value. (often referred to as par value) So a bond with a $1,000 face value and a 5% coupon rate pays $50 a year in interest.

Maturity date: bonds have a specified maturity date when the issuer repays the bond’s face value to the bondholder. Maturities can range from a few months to several decades, influencing the bond’s risk and potential return. A 30-year bond is regarded as more risky than a 5-year bond as more factors can affect the issuer’s ability to repay the debt over longer periods.

Market price: the price of a bond in the secondary market can fluctuate based on changes in interest rates, credit quality and market demand. If the bond’s market value is higher than its face value, it is trading at a premium. If it is lower than face value, it is trading at a discount.

Understanding bond prices

Bonds can be bought and sold on the secondary market after they are issued. A bond’s value in this market is determined by its price and yield. The key thing to understand is that a bond’s price moves inversely to its yield. A bond’s price reflects the value of the income it can provide. So, if interest rates are falling, the value of older bonds that were sold in a higher interest rate environment increases and their price goes up. In a rising interest rate environment, older bonds become less valuable as investors would rather buy newer bonds paying higher yields.

You can see this clearly in the performance of the above iShares TLT long-term treasury ETF. After the 2008 financial crisis, interest rates were kept low to stimulate economic recovery. Just as rates began to drift upwards, Covid happened and rates were slashed again. Bond prices increased significantly in this low interest rate environment and so the price of the ETF rose. When the Federal Reserve began raising interest rates in late 2021, bond prices fell heavily and continued to fall throughout the Fed’s tightening cycle, which is now nearing its end.

You could make a pretty strong argument that now is a good time to be buying a long-term treasury ETF like TLT. When the Fed begins cutting rates, bond prices will recover and investors will be able to capture capital gains along with income.

Conversely, having held interest rates low for longer than most other developed countries, Japan is now in a rising interest rate environment as the Bank of Japan attempts to slow down inflation. This means the price of Japanese Government Bonds is likely to fall.

Why own bonds?

Investors may choose to own bonds for a range of reasons. Those reasons include:

Steady income – particularly applicable to retirees and investors who require income for other reasons

Capital preservation – if held to maturity, bonds issued by institutions with strong credit ratings come with a low risk of loss of capital

Portfolio diversification – bonds offer a good counterbalance to equity market volatility

Capital appreciation – as above, bond prices can appreciate when central banks are cutting interest rates

A hedge against economic downturn – in the US and Europe, inflation is cooling and economies are slowing. This means the income from bonds will be able to buy more goods and services, making bonds more attractive

How to buy bonds

For a typical retail investor, there is no need to buy individual bonds. Just like equities, investors can choose from a range of active or passive strategies offered by bond funds or bond ETFs. Generally, a passive ETF provides perfectly adequate exposure to bonds without any stress or hassle. For example, Blackrock’s iShares ETF series offers 135 different bond ETFs – more than enough to build a diversified bond allocation. The fixed income part of a well-diversified portfolio will generally contain a blend of shorter/medium/longer-term government bonds along with an allocation to more risky corporate and emerging market bonds.

Be sure to pay attention to your base currency when you build such a portfolio. If you are planning to spend the money in the UK eventually, you should be looking at UK Gilts as the core of your bond holdings rather than US treasuries. Don’t be afraid to engage professional help if you are not comfortable organising this yourself.

As to whether owning bonds is really necessary or not, that’s obviously an individual call to make. I would comment that if you are young and just getting started with investing a little money every month, averaging 100% into equity ETFs is a perfectly acceptable strategy for the first few years.

However, after you have been investing for some time and have built up a larger pool of capital, it is probably time to start thinking about diversifying into other asset classes to protect against sharp drawdowns in equity markets. Bonds become a useful tool as you shift from an aggressive capital accumulation strategy to a more balanced portfolio that offers growth and income with a degree of capital preservation.

Hopefully, this post goes some way to explaining what bonds are, how they work and the benefits of investing in them. Feel free to comment or send questions any time!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Happy New Year everybody! I hope you all enjoyed a peaceful winter holiday and are back, raring to go and make big things happen.

For some reason, I had a feeling that this was going to be a challenging year and it didn’t really get off to the best start in Japan. For those interested, I was googling around yesterday trying to figure out the best way to donate to disaster relief on the Noto Peninsula. I found this page run by Ishikawa Prefecture. You can download a form here to request a receipt for your donation for tax purposes. Donations qualify for the donation deduction and there is a useful FAQ on the tax treatment of donations here.

So yeah, earthquakes, runway collisions, fires and we’re only a third of the way through January!

From a personal finance and investing perspective, there is some exciting stuff going on though. The New NISA has launched. I logged into my SBI account and it was pretty simple to get started. I have already set up the ‘tsumitate’ allocation and started buying some stocks for the ‘growth’ allocation. Clearly, everyone else is doing the same thing as the Nikkei is pumping so far this year!

I posted a couple of interesting takes on Japan on ‘X’ yesterday: an optimistic look at the year ahead from Jesper Koll and a much darker look at the demographic issues facing Japan from author Nire Shūhei. It always pays to look at both sides.

So how to invest in the year ahead? If you have been reading this blog over time, you will know that I divide investments up into core and satellite allocations. The core is a diversified portfolio weighted heavily to your base currency that just gets rebalanced once a year. This would typically account for around 70-80% of your investments and the idea is to keep adding to it as much as you can. If it’s a bit dull and boring, you are probably doing it right!

The other 20-30% can be allocated to satellite holdings, which may be a little more racy and exhibit a higher risk-return profile. If this part isn’t fun, then you are probably doing it wrong!

Satellite holdings will change over time depending on the economic environment we are in. So how are things looking?

Some thoughts

On the one hand, things look pretty much like they did for most of last year. The Fed funds rate is 5.5%. People who are obviously long risk assets have been trumpeting the start of rate cuts as early as March, but Mr Powell doesn’t look like he’s in much of a hurry to me. Although the Bank of Japan has adjusted its yield curve control policy and allowed long-term interest rates to rise a little, it is still continuing with its negative interest rate policy. There has been a significant amount of speculation, from both within and outside Japan, about when the BOJ will ‘normalise’ rates – I do love this term, like there is a way to return to normal with government debt to GDP at 264%! Gulp…

Despite noises being made about an exit from negative rate policy, it’s notable how quickly these ideas get put on the shelf. Comments I have heard recently include: ‘The earthquake will make it harder to normalise rates’. Probably true, but any excuse to avoid the inevitable. The Labour Ministry’s November report showed that real wages have declined for the past 20 months in a row, so there’s no sign of the mystical ‘virtuous cycle’ of wages outpacing price rises that would signal a move from the central bank.

It’s not going to happen, is it?

So if you’re waiting for the yen to get back to something sensible against the US dollar, good luck! Markets can remain irrational longer than you can remain solvent enough to go on a nice holiday abroad…

Japanese stocks, for the most part, are loving the weak yen. Any company with significant exports and profits abroad will see those profits magnified when converted back to yen. If you’re wondering why your Toyota shares are doing so well, there you are.

What kind of market is this?

Some time ago, I read the book Reminisces of a Stock Operator by Edwin Lefèvre. It’s considered somewhat of a bible by many investors. While there are some interesting tales of hi-jinks and high leverage, there was only really one key thing I got out of the book, but that one thing has stuck with me: Traders and investors should always know if we are in a bull market or a bear market.

It’s always the simple things that have the most impact, right? The protagonist in the book is a stock trader and his big-picture strategy is very simple: If he is in a bull market, he trades with a long bias. If he is in a bear market, he trades with a short bias. If you don’t know what kind of market you are in, you have no business trading, he says. The author coined the phrase ‘bulls and bears make money; pigs get slaughtered’.

Now, if you are a long-term investor, you don’t have to be concerned with trying to short-sell. You are more than likely to get into trouble. Simply replace the terms ‘long’ and ‘short’ with ‘risk-on’ and ‘risk-off’. Again, I am talking about satellite holdings here. You don’t have to overthink the core part of your portfolio.

Bull or bear?

The Nikkei 225 index gained around 28% last year. After such a positive start to the year, it is widely expected to keep on trucking. It’s pretty clear we are currently in a bull market. If you live in Japan and have a need for JPY base currency, then Japanese stocks are a good place to be.

The only question is what could go wrong? What could bring an end to the bull market?

I think the main short-term danger is a recession in the US. Although the financial press continues to focus on the ‘soft landing’ narrative, history tells us that rate-tightening cycles rarely have a happy ending. Depending on the depth of the recession, US stocks could fall anywhere between 20-50%. I don’t see how Japan just keeps sailing on if that happens, no matter how much better value stocks here may be. If you have already loaded up your investments for the year, I don’t think that’s a bad thing but be prepared to navigate some choppy seas. So it may not be a reason to go risk-off, but be prepared for some volatility.

The BOJ is another matter. If they actually did try to raise rates we would probably experience more than a minor squall. My expectation is they daren’t even try but let’s keep an eye on them. At year-end, I was watching a news feature where they interviewed Japanese business leaders and asked them their views on the stock market for 2024. When asked what they thought was the biggest danger to the Nikkei bull market, the majority of them said ‘the election of Donald Trump’. Interesting…my feeling is these guys need to look a little closer to home.

I’m not even going to get into geopolitics. Lots of risk there, but what are you gonna do?

Outside of Japan, US markets are making all-time highs. However, when you look under the hood, the good cheer is really driven by one group of stocks, known as the Magnificent Seven. If this is a new term to you, the stocks are Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. The size of this group is truly staggering – last time I looked, the combined market cap was around $11.7 trillion. That’s about equivalent to the entire stock markets of Japan, the UK and Canada combined! This group returned around 107% in 2023.

So this bull market is clearly a Magnificent Seven bull market, and the narrative driving it is AI. If you own any kind of global stock fund, go and check their top ten holdings. I’ll bet you that these seven stocks feature prominently.

This group of stocks are a must-own. If you feel you don’t own enough of them, a US recession and corresponding sell-off in the stock market could present a nice opportunity.

Emerging markets could be worth a whole new post, but here’s the tldr: everyone is buying India, not China.

US government bonds got clobbered through this rate hike cycle. If you bought them after the clobbering, you will probably do well as rates eventually subside.

I’m from the UK, so I usually keep an eye on the market over there, but wow, that does not look to me like a place I would want to allocate capital unless I was actually moving back there. Everything about it screams bear…

The biggest bull of all

Of course, the heavyweight champion of satellite holdings is my personal favourite. Yes, the Bitcoin-led crypto bull market is upon us. I already wrote the post on that, it’s right here. You know what to do.

Or do you? I saw a great tweet by Tuur Demeester earlier, in which he said that many people will adopt crypto reluctantly. ‘Hate buying’ he calls it. He also points out how the SEC just ‘hate approved’ the spot Bitcoin ETFs. So why are people going to buy something they hate in the end?

The answer, perhaps, lies in the ongoing debasement of Fiat money, which has accelerated considerably since the 2008 financial crisis. Raoul Pal talks about this a lot and has some great charts. You think your stocks are going up, but really it’s just the purchasing power of your money going down, and you are barely breaking even. People are gradually waking up to this. And there are not many assets that are likely to outperform this money debasement over time. Gold is not getting there. Tech stocks will probably do it, and crypto will likely do it too. Maybe you’re not ready yet, but one day you will be, and you might hate it, but you will probably buy it in the end. Better to rip off the band-aid now perhaps?

On that note, I wish you a happy and prosperous 2024!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I have been meaning to write this update for a while. In particular, because people keep finding an article I wrote about the ‘New NISA – Coming in 2024’ and telling me it is out of date, which it most certainly is! You see, that was the old new NISA plan and since then there is a new new NISA plan, which is even bigger and better. Clear? Apologies for the confusion and for my tardiness in updating – the old article will be consigned to the fires of internet hell just as soon as I get this one written and posted.

If you’ve read this blog before, you may be aware that I care very little about product. By that I mean, if you are buying a box to hold things, I don’t care if you get the blue box, the pink box or the rainbow box. It’s just a box, after all! There are a number of NISA products out there offered by online brokerages and banks. I hear even the Japan Post Bank is getting in on the act. My preference would be for the online brokerage accounts, but that’s mainly because I am terminally online and want to minimise time spent ever talking to staff at the bank! If the post office works for you, have at it!

What does get me excited is what you put in the box. That’s where things get interesting. I already wrote a post on How to choose investments for your NISA, so please check that out as a compliment to this post.

So, down to the nitty-gritty. How does the new NISA work? My NISA is with SBI, and they wrote a little guide with some ‘helpful’ graphics – see here. Google translate works ok on the main body of text but the graphics remain in Japanese. I’m really linking to this so you don’t rely entirely on this post to remain correct. Keep an eye on official sources in case something changes before launch.

In short:

You can invest up to ¥3.6 million per year – ¥1.2 million has to be invested in mutual funds, and the remaining ¥2.4 million can be invested freely. That means ETFs and direct stocks are on the menu.

The investment term is unlimited – so ¥3.6 million a year for 5 years = ¥18 million. This is the fastest you can fill it up, but you can actually take as long as you want to reach the ¥18 million limit.

The holding term is forever – there is no limit on how long you can hold the assets in the NISA. As long as you don’t sell, dividends will be paid tax-free and there will be no capital gains tax when you do eventually sell.

All in all, it’s a pretty good deal! I plan to be maxing out my allocation for each of the five years before making any investments into taxable accounts.

If you have an existing NISA, you will not be able to make any new contributions to it after the end of 2023, but you can choose to keep the money invested until the end of the term. For example, if you started a regular NISA this year and invested ¥1.2 million, you can leave that money invested, tax-free, for another four years. Any new contributions will go into the new NISA. If you have a Tsumitate NISA with 15 years remaining, you can choose to leave the money contributed up until the end of 2023 in there for 15 years. Again, from 2024 any new contributions will go to the new NISA.

Investment Strategy

I encourage you to give some thought as to how to allocate the investments in the new NISA. Again, the post I mentioned earlier may help.

There is one trade-off I am particularly focussed on here: growth vs. income. Your forever NISA investment will benefit from not being charged the 20% tax on capital gains or dividends. So which should you try to maximise? The short answer here is probably a combination of both, but let’s do some thinking about it:

For the ¥1.2 million per year that has to be invested in mutual funds, I don’t think it will be possible to generate income. Mutual funds generally re-invest dividends, so they are part of the investment return, but unless they have a distribution share class, they don’t pay dividends out. If anyone finds a mutual fund, available for NISA, that actually pays out dividends, please do chime in – I would be very interested to hear about it. For now, I’m going to assume that such funds are not available. In that case, for the ¥6 million (¥1.2 mill x 5 years) that you invest in mutual funds, it would make sense to go for growth. I will be looking for high-growth-focused funds for this part of the allocation. (note that growth stocks generally pay no/low dividends as any earnings the company makes are reinvested to spur further growth)

For the remaining ¥2.4 million a year, that’s ¥12 million, I am tempted to strongly focus on dividend-paying stocks and/or dividend stock ETFs. If you can generate a 4% dividend return on ¥12 mill, that gives you a tax-free ¥480,000 per year in income alone. And, of course, these stocks will probably also grow in value over time if you are patient. Now, nobody is retiring on ¥480,000 a year but over 25 years, for example, that’s ¥12 mill in your pocket. Not bad, huh?

Of course, there’s a pretty good argument for investing the ¥12 mill into a fund that reinvests the dividends so you get the compounding effect over the term of the NISA. I have no objection to that. I just like the idea of collecting my ¥480k tax-free every year and either spending it or reinvesting it myself.

Also, after a discussion with Ben at Retire Japan, I discovered that under the new NISA rules, you can sell assets and then re-use the tax-exempt amount to invest in a different asset, which is a huge improvement on the current system. Thanks, Ben for pointing that out! See this FAQ on the FSA website.

So those are my thoughts. I would love to hear from anyone who looks at the NISA opportunity differently. Drop me a line or come and tell me I’m wrong on X. (yes, we have to call it that now…)

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

How are people getting their financial advice these days? After 3 years pretty much at home during covid I’m wondering how it all works now. You used to have some bloke at the pub giving you stock tips, now it’s all on Twitter? When I first started in the business I used to call up guys at investment banks who knew way more about finance than me and try to blag them into meeting me. Are people still doing that? Maybe you just dance on TikTok these days?

I don’t have as much time to write this blog as I used to, so I apologise for the big gap between posts. (I wasn’t exactly prolific before, I know) However, if you only have time to write once in a while it does sharpen you up somewhat. So let’s get to the point.

I’m not your financial adviser, but you really need to get things organised. I sound like your dad, don’t I? What are you going to do with your life??? Let’s try and boil it down to the basics. Where are we and what should you be doing?

As WBC’s go, I enjoyed the World Baseball Classic much more than I’m enjoying the World Banking Crisis, but at least we are learning some stuff. The US treasury backstopped the banks. That means everyone else is going to have to backstop their banks or all the money is going to flow to the US as the least risky jurisdiction. Liquidity bottomed in October. If you don’t know what that means, listen to this podcast. The stock market bottomed around then too. Inflation is unlikely to just go away, but the Fed has raised rates about as high as they can go. Maybe another 25 bps in May but that’s about it. That doesn’t mean they will start cutting. We could sit around the 5.25% mark for the rest of the year.

Whichever way you slice it, it doesn’t look good for the yen. I discussed that here. If you are holding yen and not planning to spend yen in the future then you need to seriously consider your options. Drop your phone number in the comments and I will happily call up and shout at you like your dad.

So what should you do? Well, I may have mentioned this before, but you need to figure out your base currency and have a diversified portfolio. Diversified means cash, bonds, equities, property, commodities and alternatives, allocated according to your risk profile. If you are smart, you will want to spice it up a little by taking a core/satellite approach. 70-80% goes into the diversified portfolio, that’s the core. The other 20-30% goes into satellites. The satellites you want to own in this environment are gold and bitcoin. If you think bitcoin is silly then just buy gold. Gold mining stocks are a leveraged play on gold – maybe toss some of those in too. Ideally, your diversified portfolio should be rebalanced once a year so it doesn’t grow three heads and deviate from your risk profile. Clear?

You can either:

Do this yourself

Get someone to help you to do it

Pay an asset manager to do it for you (except maybe the bitcoin part)

Any combination of the above is fine. There’s no shame in wanting to spend your time doing other things and paying someone competent to take care of this for you. Just be aware that for number 3, you will probably need to work with a financial adviser to find the right product and not all financial advisers are the same. Some may not have your best interests at heart.

And that’s it – what was that, like a 3-minute read? I hope the weather forecast is wrong and it doesn’t rain all through cherry blossom season so you can get out and enjoy it. I’m not really going to call you up, but ask me anything, any time. Until next time!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.