The hot summer months usually mark a quiet period for markets, but there are no signs of a lull so far this year.

While the upper house election last weekend likely had a limited impact on stocks, the trade deal announced shortly after certainly got things moving. The Nikkei 225 index surged over 3% on 23 July and is creeping up on ¥42,000 as I type today.

Shigeru Ishiba may have lost his ‘mandate from heaven’, but the Japanese auto industry is saved!

Perception really is a funny thing. Automaker stocks surged yesterday as investors cheered a 10% ‘reduction’ in US import tariffs from the 25% touted by Trump. However, before Trump took office, the tariff on cars was 2.5%. So there has actually been a 12.5% increase. Trump’s big stick negotiation tactics may be crude, but they appear to be working.

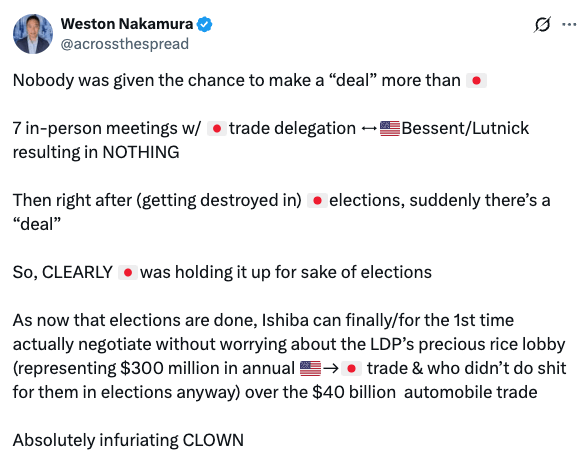

By the way, Weston Nakamura isn’t buying the coincidental timing of the trade deal announcement.

Probably the biggest pressure release for markets will be the end of tariff uncertainty. If Trump can secure a similar deal with the EU, then we are likely through the worst of it.

He’ll still have to come up with a pretty big distraction from the Epstein files, though, so we should stay on our toes.

Anyway, moving swiftly on

I find a lot of people struggle to understand the concept of currency debasement. If this is you, I highly recommend this episode of Forward Guidance with Raoul Pal and Julien Bittel:

You only actually need to listen to the first 10 minutes to get the picture, although it’s all good stuff.

A quick summary:

Governments restructured their debts after the ‘debt jubilee’ that followed the 2008 financial crisis, forming an almost perfect 4-year liquidity cycle

We’re in the 4th year of that cycle now, where the larger part of the debt is due

The liquidity that gets added never really gets taken back and is rising at a rate of around 8% per year

That is about the rate of debasement of fiat currency

If you divide an asset by the rate of global liquidity, you find out it’s true performance vs debasment

The S&P 500 is basically flat, same with other countries’ indexes

Gold is also flat, as it should be

The only assets that outperform debasement are tech stocks and crypto

Governments are now just servicing their debt. i.e. paying interest and not repaying the principal. GDP is falling due to the declining birth rate and shrinking labour force. And so, governments are debasing currency to pay for the debt.

Until political parties appear that are willing to tackle this problem, elections and politics are pretty much meaningless when it comes to investing. And, of course, no party wants to deal with the giant elephant in the room as it will mean years, likely decades of pain. That’s the reality. If you don’t want your spending power to get eroded over time, you need to be invested appropriately.

Now, should you only own tech stocks and crypto? Clearly not. But, in my humble opinion, you would be crazy not to have an allocation to them.

Incidentally, the Bitcoin 4-year cycle dovetails remarkably neatly with the 4-year liquidity cycle. I have come to realise that this is also not a coincidence. In fact, BTC lags global M2 money supply by around 90 days. Here is Julien Bittel’s chart of projected M2 from back in May:

Are you surprised that BTC is now near $120k? You shouldn’t be!

Now imagine if the Fed cuts rates in the next few months…

As long as that M2 line keeps going up, expect risk assets to follow. If you see it turn down later this year, that’s the purest signal possible that the Bitcoin bull market is nearing its end.

Inject that chart directly into my veins!

If you want to get deep into the weeds on liquidity, Arthur Hayes writes some entertaining posts. His latest is here. Be warned, Arthur is a liquidity/crypto uberbull.

Meanwhile, here in Japan, stocks are in celebration mode. I don’t see any reason to fade the mood, although my bullishness is always tempered by the fact that I’m living right here next to the canary in the debt/demographics coalmine.

You can only worry so much, though. Stay cool, and if the world ends, it will probably be a great time to buy stocks!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I’ve been getting asked about Bitcoin storage lately, so I thought I’d write a post on the topic. People rightly point out that one of the major obstacles to mainstream adoption of BTC is how difficult it is for the average person to store it safely. It’s actually one of the reasons I believe we are still relatively early in the adoption cycle, as it’s simply a problem waiting to be solved. Or at least made easier.

People have perhaps become all too accustomed to handing their assets over to ‘trusted third parties’ for safekeeping. Looking after your own Bitcoin keys is a degree of responsibility that most people are simply not used to taking on. It’s actually one of the things that fascinates me about the asset class – you have the choice of how much you want to actually be in control of your money. Custodial services are going to become more sophisticated going forward, but there will always be purists who want to manage their own keys.

What keys?

Non-Bitcoin people are probably already confused by the term ‘keys’. Put simply, you do not actually store Bitcoin itself. You store the private cryptographic keys that give you permission to access that Bitcoin. If you do not have access to your own keys, the coins can be taken from you – hence the mantra that forms the title of this post.

This doesn’t necessarily have to be done online. You can simply write your keys down on a piece of paper. If you are lucky enough to have a photographic memory, you can even store them in your head! Most people are going to want to use some kind of wallet, though.

Exchange risk

People generally purchase Bitcoin on an exchange. It’s very tempting to just leave it sitting right there. After all, it’s password protected, and you have set up 2FA. What could go wrong?

Exchanges get hacked. It’s happened many times before, with some of the biggest hacks occurring in Japan. Non-Bitcoin people may even have heard of Mt Gox, which went down back in 2014. It was by no means the last exchange to get hacked, with Coincheck suffering an attack in 2018 and DMM getting hacked more recently. Exchanges may also fail due to fraud and mismanagement, as FTX did in 2022.

Japan is interesting, as the FSA is incredibly strict and requires exchanges to keep enough reserves to cover customers in case of a hack. It’s actually one of the few countries in the world where you stand a reasonable chance of getting your money back in the event of a breach. But do you really want to take the chance?

What about small amounts?

If you only have a small exposure to Bitcoin, buying a cold storage wallet, setting it up and managing it seems like a lot of hassle. I get why people sometimes just leave coins on the exchange. However, everyone has a point where the amount of money becomes too big to stomach a loss, especially from a well-documented risk that you should have known better about taking. It’s really up to you to decide when you have reached that point.

Here’s the thing, though: people tend to think in terms of today’s value. They look at the amount of BTC they have and today’s price and say, “ok, I’m not going to go to the trouble of moving my coins off the exchange for this trivial amount”. What I would encourage people to do is think in terms of potential future value – if you lose your Bitcoin today, it’s gone. If the BTC price rises to $1 million per coin in ten years, how mad are you going to be that you didn’t protect it???

If it’s on the exchange, not your keys, not your cheese. North Korean hackers will never stop trying to get it!

Here are a few things to consider if you have decided it’s time to start looking after your holdings:

Online/offline

The first tradeoff comes with online vs. offline wallets, sometimes also referred to as hot and cold wallets.

It’s pretty simple: if your wallet is on a device that is connected to the internet (hot), it’s very convenient to use, but more susceptible to an attack. That’s why you hear Bitcoiners talk about putting their coins in cold storage. Take the keys offline, and it is much more difficult for a bad actor to get to them.

Custodial/Non-custodial

Once you have decided you want to get your keys offline, your next choice is whether to get a third party to handle it for you or do it yourself.

Of course, custodial services mean trusting someone else to manage your keys. The good ones will do this very well, perhaps better than you can yourself, but they won’t do it for free. You have to be very careful choosing a custodian and making sure that they really have your coins in cold storage and are not, in fact, lending them out to other parties and putting them at risk. Do your homework! If something doesn’t add up, there will be a reason. If a custodian is offering you a high rate of interest on your BTC, for instance, you are going to want to know where that yield is coming from and whether your coins are being put at risk to generate it.

Maybe custodial isn’t the easy route after all – it does require significant due diligence. Even after that, you have to trust the custodian to do what they say they will do.

Non-custodial cold storage

What most Bitcoiners have already figured out is that if you want a job done properly, you should do it yourself! Assuming we are not just writing our keys on paper or memorising them, this means purchasing a hardware wallet.

There are many hardware wallets available. The two best-known are made by Trezor and Ledger. I have used both and prefer Trezor, but it’s just my personal preference.

In terms of how to use these devices, I will try to keep it simple for now: buy one and follow the instructions to set it up! Tech-savvy people will find it easy. If you live in the world and have set up new computers, phones and other devices, it’s not going to be too difficult. Getting your ageing parents to use one might be a stretch…

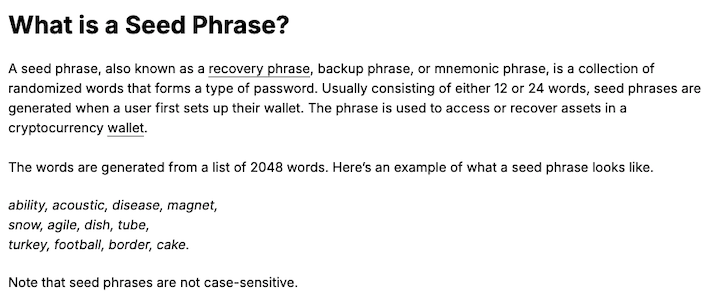

When you set up your device, you will be guided through the process of generating a seed phrase. Here’s a definition from the Leger website:

You will want to handle your seed phrase properly. It essentially functions as a master key to access your private keys. And, if you lose or damage your hardware wallet, you can use the seed phrase to recover your keys on a new device.

Some basic rules:

Do not share your seed phrase with anyone

Do not store it online – this is not an email password that you put in a Google document or in a made-up contact in your address book! If anyone gets access to your seed phrase, they can steal your funds!

Do not type your seed phrase into anything other than your device, no matter who asks you to do so! If you keep everything safe, you will rarely need to use it at all.

Beware of emails from Trezor or Ledger saying there is a problem with your device and you need to follow a link, plug it in and enter your seed phrase to protect your funds! These emails are scams and will result in your wallet getting drained – no matter how real they may look, do not click anything!

I know this sounds a little scary, but welcome to taking responsibility for your own money! You also need to be careful accessing hardware provider websites, too – bookmark the link and access from there. These days, people tend to just Google ‘Trezor’ and click the top result – scammers work hard to get fake websites to the top of the rankings to catch people who do this. (This goes for any website, but especially where there is money or your private data at risk)

You should write your seed phrase down and store it somewhere safe. There are numerous devices available that are more sturdy than a piece of paper. I have had my wife walk in on me as I am punching a seed phrase into a metal plate – that wasn’t a simple conversation, but it was easier than explaining that the keys to my crypto ended up in the bin by accident…

Consult the experts

I am probably relatively crypto security savvy. But I am by no means an expert. I highly recommend that you consult the experts if you are going to self-custody your coins. Fortunately, I have just the guy for you!

Jameson Lopp has put together a trove of useful Bitcoin information on his website. He has tested and written up most of the Bitcoin wallets there are and published the information here: Recommended Bitcoin Wallets

He has also tested most of the seed backup devices – to destruction in some cases! His basic conclusion is that the more bells and whistles a backup device has, the more chances you have to mess it up. It’s hard to beat the simplicity of punching the phrase into a piece of metal!

Lopp is Co-founder & Chief Security Officer of Casa Hodl, which offers a range of solutions to help people store their Bitcoin more effectively. I’m not going to try to explain multisig here, but in a nutshell, it is a level of security which requires more than one user to approve a transaction using private keys. As the numbers get bigger, paying for better security begins to make sense.

Anyway, I’m not here to sell Casa’s services; I’m saying that Jameson Lopp has already done most of the research for you and generously published it on his website so you can learn. Check out his site and follow him on X @lopp

My two cents

As you have probably realised, some people possess far greater knowledge on storing Bitcoin and crypto than I do. However, if you want to know how I organise it, I can tell you.

Like with investments, I take a diversified approach. I think it’s important to learn how to take responsibility and self-custody, so I do that. However, I also live in a wooden house in an earthquake-prone country, and I am not entirely confident in looking after all of my Bitcoin. So, I also use Xapo Bank for third-party custody. I have written about them here: Banking your Bitcoin

If you ever decide to open an account with Xapo Bank, please use my referral code (SMM-XAT-EJG) or the referral link in that post. I have an ‘influencer’ deal with them, and I am surely the worst influencer they have ever had!!! It would be nice to actually help them get a customer now and then, and it won’t cost you any more than it would if you went directly to them. I am very comfortable recommending them.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I keep seeing posts declaring the 60/40 portfolio dead. No sh*t, Sherlock! Markowitz’s Modern Portfolio Theory dates back to 1952. I learned that 60/40 was no longer relevant in 2005. Where the hell have you been?

In case you are not familiar with it, the 60/40 refers to the traditional portfolio strategy that allocates 60% to stocks and 40% to bonds. The stock part aims for long-term growth while the bonds smooth out the volatility in rough periods.

Markowitz advanced this idea by blending a range of assets to produce a more efficient portfolio, recognising that the typical investor wants reasonable returns without excessive risk. See my post on Asset Allocation for more on this.

Can’t I just long equities?

Yes, it’s perfectly acceptable to just average into one or two stock ETFs and hold them for the long term, especially if you’re young. In fact, you can do that and read no further – you don’t need any help!

However, if you believe in passive investing and market indexing, which many people do these days, you must understand that the market encompasses more than just stocks.

Also, if you are investing a significant amount of money, it’s unwise to be 100% invested in one asset class, unless you have specific knowledge and overwhelming conviction. (which, by definition, a passive investor does not)

What’s a lot of money then? Great question! It’s different for everyone, but let me put it this way: If you are a passive investor, 100% in stocks, and you are starting to get concerned about the damage a market crash could do to your net worth, you might be getting close!

The funny thing about the 60/40 idea is that young people these days are probably already allocated 60/40, but to tech stocks and crypto!

Yeah, crypto, so where does that fit in?

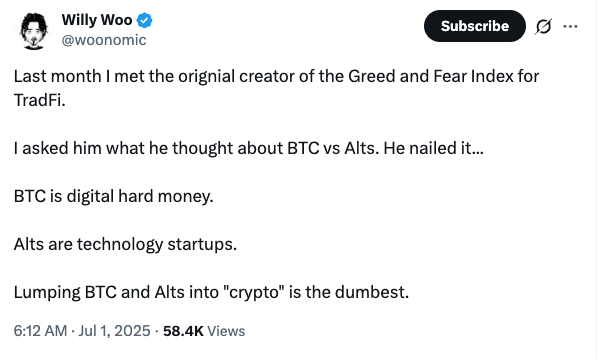

This question is doing the rounds. If crypto is a new asset class, then where does it fit in a diversified portfolio? How big should the allocation be?

— The Wolf Of All Streets (@scottmelker) July 1, 2025

We can argue all day about whether the allocation should be closer to 10% or 40%. It clearly depends on an individual’s situation, risk profile, level of conviction, etc. The notable thing about this article is how it mixes up the whole Bitcoin vs. crypto terminology.

It mentions Bitcoin to start, but then it refers to crypto. So you should be putting 10-40% of your portfolio in what exactly? Bitcoin ETFs? Cryptocurrencies? Which ones? It’s not very clear.

I mean, they’re all the same thing, right?

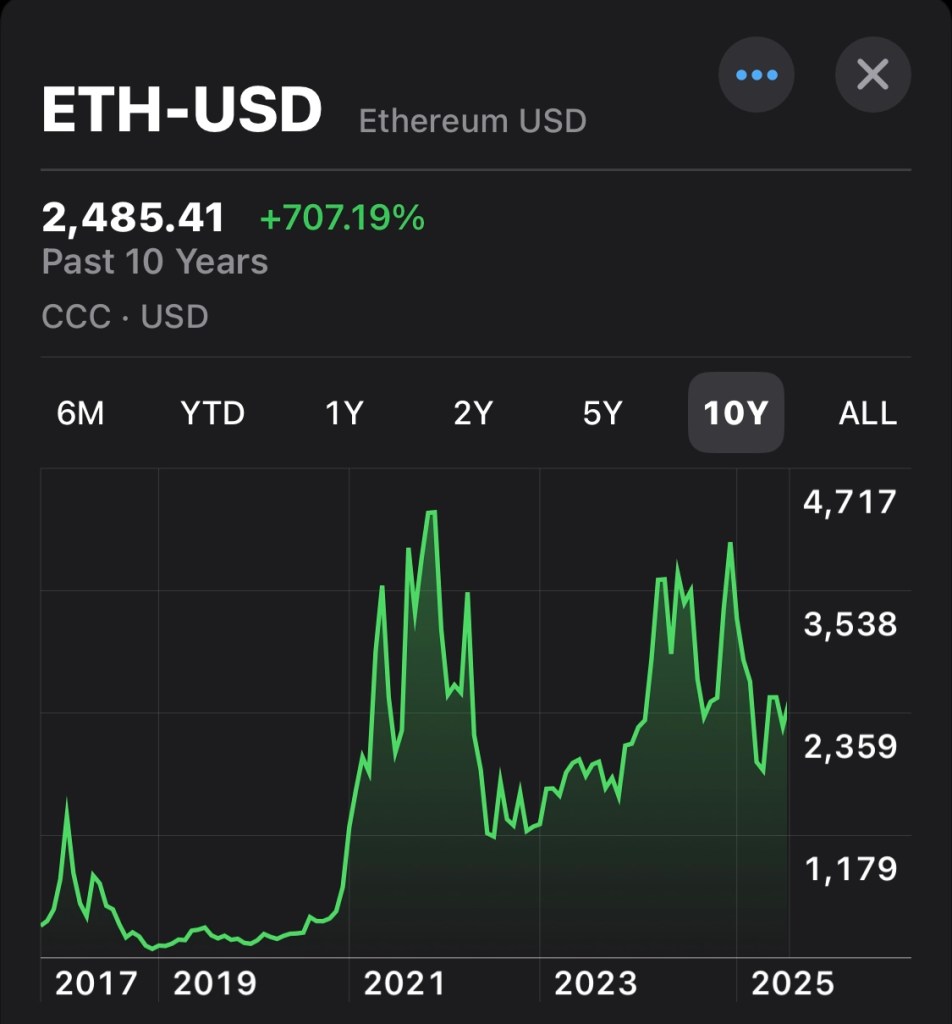

Not even close! And ETH is the second-largest digital asset. Think how many coins have gone to zero since 2017! In my opinion, if you’re going to allocate part of your portfolio to this asset class, you need to get smart about it.

Here’s a pretty solid definition:

I’m not saying you can’t have mad conviction on a particular coin and hold it as an investment. If you have that level of certainty, then go for it. Hardcore XRP hodlers don’t care what I think, and they shouldn’t. They believe in the coin. But should the average investor put 10% of their net worth into it? Of course not!

The mainstream media are leading lambs to the slaughter if they can’t get their terminology straight.

Here’s the only truly investable cryptoasset in my humble opinion. Doesn’t it look beautiful?

Uncorrelated assets for the win

The modern portfolio enhances 60/40 by adding assets that are uncorrelated or only lightly correlated to stocks and bonds. That’s how you achieve better risk-adjusted returns. (similar or better returns with less risk) Back in 2005, I never imagined a shiny new, uncorrelated asset would emerge. It really is a remarkable thing.

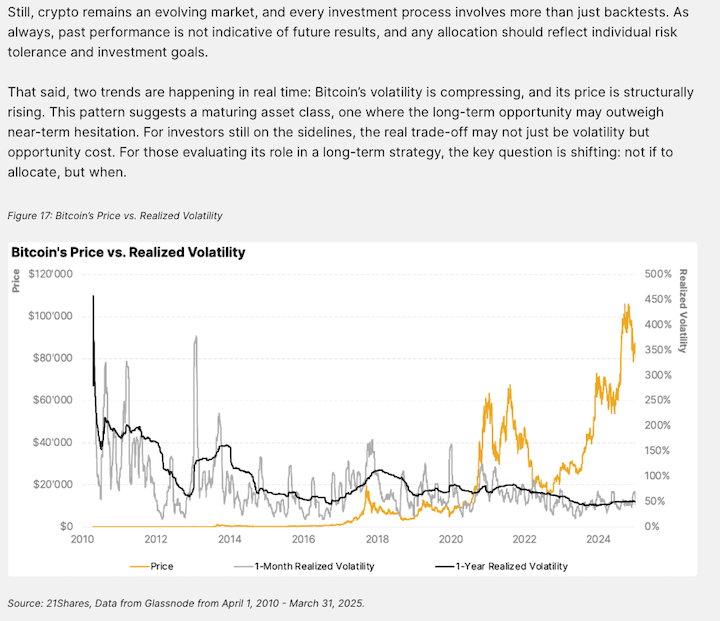

Here’s a quick summary: between April 2022 and March 2025, Bitcoin’s correlation to the rest of the asset universe was 36%. People like to compare Bitcoin to tech stocks, but its correlation to them was only 40%. These levels are significantly lower than traditional assets’ correlation to each other, which typically comes in at around 60-70%. This makes Bitcoin an ideal asset to add to a diversified portfolio in order to beef up returns without meaningfully increasing risk.

What makes Bitcoin especially interesting is how sometimes it behaves like a risk asset, like equities, and other times, it acts as a defensive asset, like gold. Over time, it is expected to become more of a gold-like store of value asset.

“This makes Bitcoin unlike any other asset in the market. It is structurally independent, behaviorally adaptive, and still offers significant asymmetric upside relative to legacy safe-haven assets. For portfolio construction, Bitcoin stands out as both a potential long-term hedge, and a high-impact diversifier at present.”

Adding a 1% allocation to Bitcoin to a modern portfolio over the 3 years resulted in stronger risk-adjusted returns. (It improved both cumulative returns and shape ratios)

Adding Bitcoin did not increase downside risk.

When scaling up to a 5% Bitcoin allocation, the risk-adjusted returns were even stronger, and the volatility remained manageable. Interestingly, they also tried a 3% allocation to the top 5 cryptoassets and achieved a similar uplift in performance without greatly increasing the risk.

So what’s the conclusion to be drawn here? You don’t have to go 40% into Bitcoin! Just a modest allocation increases portfolio efficiency without meaningfully increasing risk.

What are we trying to do again?

The whole point of investing is to beat inflation in your base currency. Doing it most efficiently with the least amount of risk is just being smart.

You can be overweight certain satellite holdings if you have a high level of conviction in them.

I still run a boring diversified portfolio, despite currently exceeding the recommended daily dosage of Bitcoin and Japanese stocks.

What’s my level of certainty?

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.