Happy New Year, everyone! Welcome to the year of the horse. Markets are off to a strong start and have not shied away from early geopolitical shenanigans. The going appears to be good to firm as we come out of the gate in January, and runners and riders are expecting a fast race.

Ok, enough horsing around. January means many of us have NISA investments to allocate. It’s time to make some decisions.

I just scanned through my 2025 New Year post, Snakes and Elephants, and what do you know? This time last year, USD/JPY was around ¥158. Japanese retail investors were largely ignoring the bull market in local stocks and piling into US companies. And Bitcoin was trading at around $93,000.

Great Scott!

At least stocks are a good bit higher than they were this time last year. You would never guess the whole “Liberation Day” debacle happened unless you were there. If your 2025 NISA allocations are not in profit, something went very wrong…

The difference with Bitcoin is that last year, it was at $93k on the way up. Now, it’s around the same price on the way back down. At least that’s what I think, although many will disagree. But let’s leave the magic internet money for another post.

What is the outlook for equities in 2026?

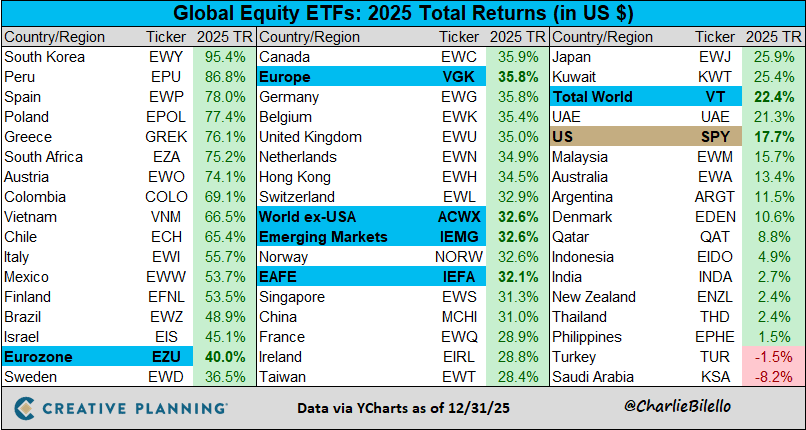

The Bloomberg Outlook always provides a nice window into what Wall Street expects in the year ahead. In short, pretty much everyone is optimistic, and the AI boom continues to be the main story. The Fed is expected to continue to loosen monetary policy, and Trump and Bessent are also standing by to man the liquidity pump.

The leaders of Japan’s securities firms are also primed for another big year in domestic stocks, as per this NHK article. However, the Japan Times reports here that Japanese retail investors are still more interested in US stocks. It looks like Japanese stocks remain under-owned.

If, like me, you enjoy a little crypto and spice with your macro commentary, Arthur Hayes’ latest post is a fun read. He sees the Trump admin running the economy hot in 2026, whilst simultaneously trying to contain inflation by holding gas prices down. That Venezuelan oil may have a purpose, huh?

Suffice to say that everyone is sufficiently bulled up that we should be at least a little worried. Risk lurks in the AI bubble, excessive government debt, BOJ policy and the yen carry trade, rising bond yields, geopolitical crises, and who knows where else!

We all love a challenge, don’t we?

My themes for 2026, which I outlined in my previous post, are mostly unchanged

For Japan:

- Japan’s base interest rate is 0.75%, and inflation is around 3%, so we have a real rate of negative 2.25%

- The BOJ can maybe squeeze in one more hike to 1%, so real rates could go to negative 2%

- This is still very accommodative monetary policy and will support asset prices

- The weak yen will persist

- Rice isn’t getting any cheaper, and people’s spending power will continue to decline

By the way, I feel like that last point is going to be critical for the Takaichi administration. People are feeling the pinch, and if prices continue to rise, I expect that beautiful approval rate to take a beating. Complaining about bad foreigners will only distract the public for so long…

Some more general themes:

- Trump’s new Fed pick will likely force lower rates

- Trump will want to pump the stock market ahead of the midterms

- However, the AI trade will continue to come under scrutiny

- The debasement trade is very much still in play – own hard assets

- Bitcoin bear market – an opportunity to accumulate

I’ll come back to some of these in future posts.

So, what to do with ¥3.6 million?

Of course, I can’t give broad advice here, but I can tell you my own personal plan for NISA this year. Bear in mind that what works for me may not work for you, and we may have different goals and risk profiles. If you need help figuring out what is best for you, remember that I offer a coaching service.

I view NISA as a long-term investment. I want to mess with it as little as possible. If I make a bad pick, sure, I will drop it and reallocate later, but I prefer it to be set and forget.

Therefore, I will stick with last year’s plan of allocating most of Growth NISA to ETFs. I will continue to pick stocks in my taxable account, mainly because I like doing so, not because I really believe I can outperform. (it’s fun to try, and it works sometimes)

While I will allocate some money to global indices, I want to keep a decent chunk in yen. Converting to dollar assets at these exchange rates is painful!

Here are some ETFs I like:

- 1489 NEXT FUNDS Nikkei 225 High Dividend Yield Stock 50 Index – The S&P 500’s Dividend Yield ended 2025 at 1.15%, its lowest level since 2000. Japan is a dividend paradise, and I love this ETF as a simple way to earn steady dividends without worrying about how a certain company performs over the next decade. For a dividend fund, it has delivered impressive growth these last few years, too.

- 2644 Global X Japan Semiconductor – this will be volatile, but long-term chip demand is only going up

- 1624 NEXT FUNDS TOPIX-17 MACHINERY – this is 25% allocated to Mitsubishi Heavy Industries, so a bit concentrated

- 1627 NEXT FUNDS TOPIX-17 ELECTRIC POWER & GAS – this is a new one for me, and I’m substituting it in for an energy ETF. I’m bullish on power companies.

- 2559 MAXIS World Equity – good old All Country!

- 1545 NEXT FUNDS NASDAQ-100 (Unhedged)

The difficult part is timing. Markets are ripping early in the year, and I would love to catch a dip. But who knows when that will come? I will aim to have Growth fully allocated by the 30 March ex-dividend date for Japanese stocks. Maybe Trump can then crash everything in April again for a bit more déjà vu…

Tsumitate, I will keep the same at 40% JPX 400, 30% All Country, 30% NASDAQ. Average in and chill.

How about you? Do you have a plan in place, or are you still mulling the options? I would love to hear what other people are doing.

Wishing everyone all the best for 2026. Let’s make it a great year!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Discover more from Smart Money Asia

Subscribe to get the latest posts sent to your email.