Last month, I read a fascinating article about punters in the NFL. What was particularly surprising is how Australians now dominate punting in American football.

I looked up the word ‘punt’ and it has four distinct meanings: a narrow, flat-bottomed boat, to kick a ball upfield, to speculate or gamble and the basic monetary unit of the Republic of Ireland, before the Euro.

You can probably guess which one I’m interested in.

As regular readers will know, I favour a core-satellite approach to asset allocation. The core is a diversified portfolio, mainly denominated in your base currency and matched to your risk profile. Satellite holdings give things an extra spice, or maybe even, an extra kick. If 20% of your investments are in satellites, that 20% may also be broken down into traditional assets, such as commodities, niche stock market sectors – such as biotech, or alternatives. You may even want to take a small portion of the 20% and have a punt on something truly speculative. Imagine if you took a punt on AI a few years back.

The art of the punt is to find a candidate for the next megatrend and allocate a small amount of your wealth to it. If you are wrong, it’s money you can afford to lose. And if you are right, the returns are asymmetrical.

Megatrend:a long-term, large-scale shift that can impact economies, industries, and the way people live. Megatrends can be driven by technological advancements, demographic changes, or global policy shifts. Some examples of megatrends include: the rise of the internet, the ageing population, the shift to renewable energy, rapid urbanization, and technological breakthroughs.

That overview came from Google’s AI, by the way.

Earlier this month, Google caused a stir when it introduced Willow, a state-of-the-art quantum chip. Willow has been in development for 10 years and has reached the stage where it can ‘perform a standard benchmark computation in under five minutes that would take one of today’s fastest supercomputers 10 septillion (that is, 1025) years — a number that vastly exceeds the age of the Universe.’

Does that sound like a megatrend? It sounds like a punt to me! The key thing about technologies like this is that the pace of development is exponential. Nothing happens for years and then massive progress is made in a short period.

A few years back, a friend dragged me to a quantum computing seminar. He was attending to show support to one of the presenters. My friend is a finance pro and I’m a pretty good generalist and I remember clearly how, about a minute and a half into the presentation, we looked at each other like, WTF?????

Needless to say, I will not attempt to explain how QC works. Do your own research, as they say!

Here’s a nice friendly BBC article to get started with.

And, here’s a great thread by Charles Edwards. It helpfully identifies four stocks that punters can buy if they want to get exposure. They are IONQ, RGTI, QUBT and QBTS.

Please note: This is not investment advice. These stocks are a punt! You should not put a large chunk of your net worth into them. Also, they have gone up a lot since the Willow announcement. They will exhibit a ton of volatility and there will probably be better entries in the future. Funnily enough, three of them were down big just last night. I have seen threads detailing how QUBT barely has a business. Three of them might amount to nothing. Maybe all four companies will go bankrupt. However, one of them might develop the ChatGPT of quantum computing.

So, buyer beware. Do as much reading as possible and, if you decide to get involved, only play with money that is truly available for a punt. There is no need to rush into anything and you don’t need to invest a lot to spice up a well-diversified portfolio.

And, unless it’s really your thing, don’t go to any quantum computing seminars!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Happy Friday! I thought I would provide a quick round-up of what is going on in markets. In case you missed it, here’s the most important five minutes of financial commentary I saw this week:

If you don’t know who PTJ is, here is his Wikipedia page. The Tldr is legendary trader and billionaire hedge fund manager.

The message here couldn’t be clearer: ‘All roads lead to inflation.’ Note the mention of Japan around the 4-minute mark. The playbook for how nations get themselves out of debt trouble is to inflate their way out. This is happening. Think what that means for your spending power. Think what it means for the yen…

So what assets does a guy like this own to face down the inflation threat? Bitcoin, gold, commodities and tech stocks. Hard assets and tech stocks. Simple.

I have had numerous conversations this past few weeks along the lines of ‘I want to own gold, but I feel like I’m too late.’ Yes, this is why I preach having the core of your assets in a diversified portfolio instead of just lumping it all into a global stock ETF. If you owned a diversified portfolio, you would have 3-5% in gold, and that part of your portfolio would be up +30% this year already. You wouldn’t have to scramble to buy some now.

This is an excerpt from a post I wrote in March 2023:

‘But global stocks have outperformed a diversified allocation over the last 12 months.’ – yes, there will be times when they will do that and there will be times when they won’t…

Here’s the simplest way I can put it: if you are young and in the process of accumulating wealth, then maybe a 100% stock allocation is ok. If you have already built up a nice nest egg, you need to think seriously about how to keep it. Spread the risk and sleep well at night.

When it comes to the satellite holdings, it’s pretty clear what needs to be beefed up right now: bitcoin, gold, commodities and tech stocks. You might already have commodities in your diversified portfolio, but with inflation looming, it’s time to get some more. Note that PTJ mentions how commodities are still under-owned.

Bitcoin is coiled

The Bitcoin four-year cycle is playing out exactly as expected and we are about to enter the fun phase.

If you are waiting around for a Japan Bitcoin ETF, I wouldn’t hold your breath – see this Financial Times article.

Meanwhile, Microsoft placed an ‘assessment on investing in Bitcoin’ on the voting ballot for its 10 December annual shareholder meeting. The Microsoft board recommends voting against the proposal, deeming it ‘unnecessary’ as the firm’s management ‘already carefully considers this topic’. This is a conversation that will take place in boardrooms of more and more major companies. Note here that Tesla still owns 9,720 BTC.

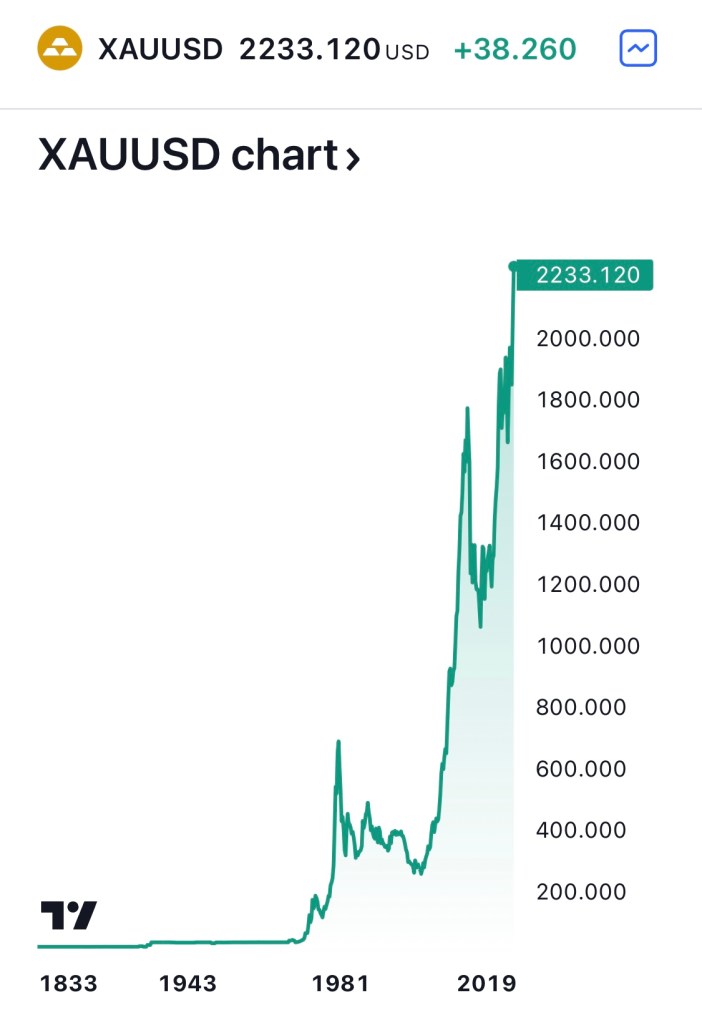

Gold breakout is happening now – are you really late?

Chart of the Week – Gold

Gold is starting to come on the radar for more and more people (after rallying some 60% off the October 2022 low), with financial pundits, hedge fund billionaires, and even mainstream media starting to talk louder about the shiny metal.

Tesla was the first Magnificent 7 company to report earnings this season and it got things off to a good start. The EV manufacturer’s stock just had its best day in the market in over a decade after reporting better-than-expected results. I understand why some people don’t like the CEO, but betting against his companies is a risky business. A +22% gain in a day is going to hurt some short sellers. More on upcoming Mag 7 earnings here.

That’s all I have for today. Wishing everyone a great weekend!

In summary, all roads lead to inflation. A core diversified portfolio and satellite holdings in bitcoin, gold, commodities and tech stocks is the best way to face down the threat to your purchasing power.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I hope you are enjoying Obon and the summer holiday. After a market crash and a Nankai Trough earthquake warning, things feel a little calmer this week. Hopefully, there won’t be any more ‘big events’ in August other than the local matsuri.

However, September is approaching and it feels like that will be the time to get locked in and focused. So here are a few thoughts as we speed into the last four months of the year!

US markets

There is a slew of economic data coming out of America this week, with the Producer Price Index (PPI) coming in a little softer than expected last night. CPI is tonight and another soft print will heighten expectations of a Fed rate cut in September. Toys will be thrown if Chair Powell does not deliver, but I’m also becoming a little more cautious about the outlook for stocks if he does go ahead and cut. History favours a recession scenario at the end of a hiking cycle. A lot of effort has gone into the soft landing narrative, so we should be on our guard. No reason to make adjustments to long-term investments but things rarely go as smoothly as the crowd expects.

That said, the completion of the US election will remove a lot of uncertainty, regardless of who wins.

Yen / Japan stocks

After starting August with a bang, the Bank of Japan has swiftly backed down from any plan to raise rates again this year. They got as far as 0.25% and the stock market melted down. They didn’t even get to the bond market jitters part of the project. I would love to hear from anyone who can explain how the BOJ will go about a meaningful tightening from here. Imagine what rates at 0.5% would look like. How about 1%?

I just saw a Bloomberg headline that said that PM Kishida is stepping down in favour of a leader who is supportive of the central bank’s efforts to normalise policy. Best of luck to whoever picks up that poison chalice!

Let’s just call BS, shall we? You can’t normalise a ponzi.

Nonetheless, if the Fed does begin to cut, the yen should strengthen. I don’t know how far it will get. 130? 120? 100? It doesn’t matter, because once that cycle is over it is only going the other way. You can save the bond market or the currency and no one is sacrificing the bond market.

I have said it before but I’m nothing if not a broken record: if you are going to spend your future money outside of Japan, you should forget about those alluringly cheap Japanese value stocks and get your money out of yen and into your base currency while you have the opportunity.

If you are here for the long haul, by all means, have at it. In the shorter term, Japanese stocks should do ok and I would even be tempted to look for names that will benefit from a stronger yen. Exporters that did well under the weak yen don’t seem such a great idea going forward.

Getting hard

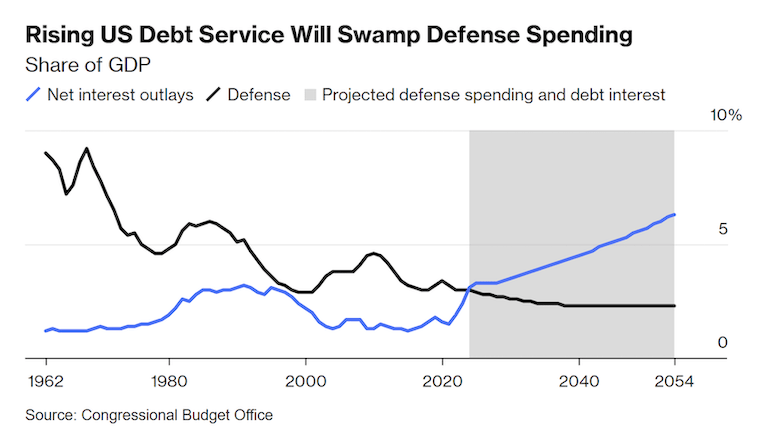

With the US election looming, the cynical among us would be watching out for a liquidity boost to pump up the US stock market. Rather than the Fed, we should probably be looking at the treasury to provide the liquid refreshment. This ‘Bad Gurl Yellen’ piece by Arthur Hayes goes deep into the fountain of liquidity that is about to spring forth. In short, the treasury needs to lower the debt-to-GDP ratio, and it will do so by issuing yet more debt.

The Congressional Budget Office projects that interest payments on America’s debt will total $892 billion in fiscal 2024 and rise significantly in the next decade.

If you are wondering what that looks like, get a load of this chart:

Tell me you’re gonna print more money without saying you’re gonna print more money…

I wrote about currency debasement and and how to protect yourself in Harden up your assets! If you are looking at stocks to plough your hard-earned money into right now, that’s one way to do it but maybe there is a better option.

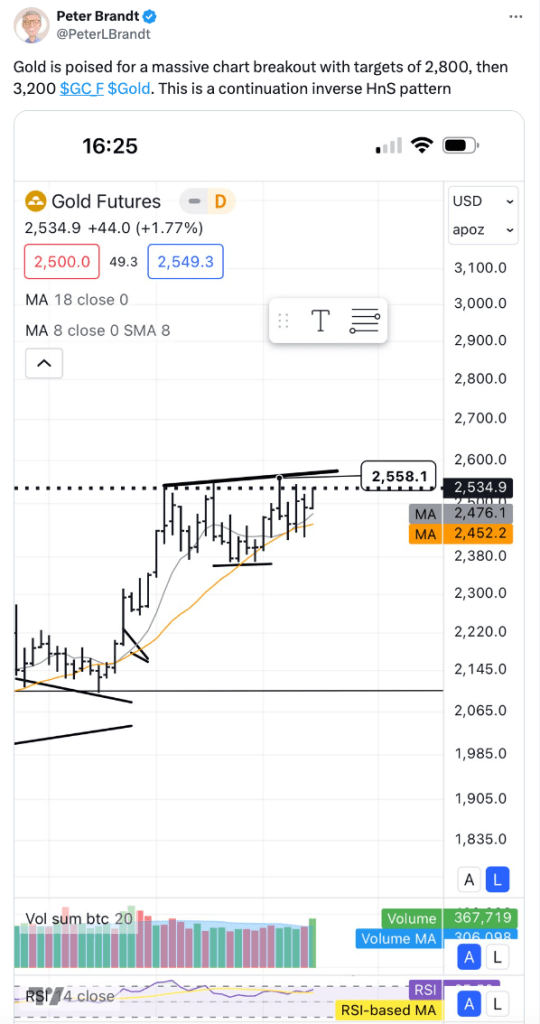

As you can see, some technical traders are getting excited about gold. JP Morgan agrees, arguing that the structural bull market remains intact and forecasting an average price of $2,500 in Q4 and $2,600 in 2025. Geopolitical tensions, rate cut expectations, central bank buying and ETF flows all point to elevated gold prices – report here.

Of course, those are short-term targets and the real point of owning gold is to protect against currency debasement over time. Remember, this is what you’re up against:

Digital gold

Ever the broken record, allow me to point out once more that the boring phase of the Bitcoin bull market is drawing to a close. We probably bounce around for a few more weeks, maybe even a couple of months. The timing is difficult to predict but I expect significantly higher prices by the end of the year. And more to come in 2025. If you are thinking of getting on the train, you don’t have long left…

Despite a reshuffle of the Democratic nominee, pretty much everything I wrote in the Bitcoin bull market update still stands. All aboard!

If you are still trying to get your head around the hardest asset on the planet, the presentations from Michael Saylor’s keynotes are a great resource.

Don’t say I didn’t warn you!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

The haters said I couldn’t do it. And they were right. Honestly, great call by the haters.

Stairs up, elevator down.

If you have been diligently investing in stocks these last few years, especially Japanese stocks, you are probably not feeling too great right now. You are probably feeling a little sick in the stomach. And maybe a bit stupid. I’m here to tell you it’s alright to feel bad for a while but don’t beat yourself up too much. Nobody saw a crash like this coming. Hell, the day the BOJ raised rates, the market went up! Don’t listen to the smart-asses who tell you they knew this would happen and traded it perfectly – most of them didn’t even have any skin in the game.

However, if you are going to take a beating in the markets, you better learn something from it. Otherwise, it really was all for nothing. Welcome to the Hansei-kai.

The Google translation is kind of cute. Whenever I hear this word actually used, it’s more like: ‘We screwed up, now we have to examine why and drown our sorrows’. Maybe it’s just the company I keep!

The purpose of this post is not to bore you with another deep-dive analysis of the unwinding of the yen carry trade. You have probably had enough of that already and there are people more qualified to talk about it than me. The idea is to try and learn something from the experience that will be helpful in the future.

There are always signs!

I haven’t lost my shirt in this crash and I hope you haven’t either. However, I was sitting on some rather profitable satellite positions, mostly in Japanese stocks, and I was thinking about selling some of them. I know this because I wrote about it just six weeks ago in Are we shaking?

What’s worse, I had figured out that if anything was going to derail the Japanese equity bull market, it would be the Bank of Japan. I know this because I wrote about it in January: 2024 – Here goes nothing!

The call was coming from inside the house!

Aren’t I the clever one! I had it all figured out and I didn’t sell.

I am a regular viewer of the Nikkei News Next program on BS TV Tokyo. These last few months, I couldn’t shake this nagging impression of hubris as the presenters and guests lauded the performance of the Japanese stock market and talked about the prospects of the BOJ raising rates like it would be just another positive. Don’t get me wrong, it’s a serious news program asking the right questions, but my feeling was that they were a little too caught up in the hype.

And I didn’t sell!

Ok, ok. I said we weren’t going to beat ourselves up. But you get the picture. The signs were there. And of course, they are a hundred times more obvious in hindsight. I’m not even that mad at myself. I never had any intention of touching my core investments and I have dry powder at the ready to allocate once the panic subsides. My point is that if your gut is telling you something, maybe you should listen to it.

Sell euphoria. Sell euphoria. Sell euphoria. I’m not going to get the tattoo but it has been imprinted on my brain.

What happens next?

After the Hansei-kai, it’s time to move forward. It’s still a little early for me to think about how to allocate money. US futures are down bad and it’s probably going to be a long week. I don’t feel the need to dive in immediately and any stocks I buy will be with a minimum 5-year timeframe. I’m a lot better at buying fear than I am at selling euphoria!

So, more on that at a later date. For now, go easy on yourself, learn the lessons and get ready to step up to the next level.

And f**k the BOJ lol!!!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Being a financial planner by trade, I try to organise our financial future as efficiently as possible without going overboard. My wife and I both work and we have a reasonable income. We have a plan, we know what our numbers are for later in life and the big events in between. Most of all, we are flexible in that plan – our core investments are set and forget, but they can be adjusted easily. The tactical stuff is fun for me and I see it as a bit of a challenge.

Of course, things can go wrong: ill health, accidents, economic change and shifts in specific industries. You prepare for these as best you can and get on with living. Eat well, exercise, look both ways crossing the street, buy insurance etc. etc.

However, there are a few bigger things that bother me. I don’t think about them all the time, but they lurk in the back of my mind. For example, I don’t think AI is going to take over my job, but it could change the world considerably – gotta keep up with developments there. I could classify these things as outliers and conspiracies. Some may or may not have a meaningful impact and others feel a little ‘out there’. The best conspiracy theories have an element of truth, though, don’t they?

So, here are a few things I think about and how they relate to money, investing and how big your number should be:

Climate

I must confess, I don’t allow myself to dwell on what we are doing to the planet. We are clearly having an adverse impact and most of the damage is being done by big business interests who will not stop. The paper straws are cute, but they are hardly going to offset the widespread burning of fossil fuels and other environmental destruction. It’s not that I don’t think it’s important – it’s crucial to our survival as a species. I just know there isn’t much I can do about it. I separate our garbage, cut down on plastic and try not to waste resources, but I’m not losing sleep. Half the people in the developed world don’t even believe climate change exists so good luck to us coming together and taking action as a species. Do you remember the Covid mask and vaccine debates?

It is certainly getting hotter though! And it’s hotter for longer than it was before. After 27 years in Japan, it’s noticeable how spring and autumn are shrinking while summer gets longer year by year. What’s that going to be like in 10 years? How about 20?

I hardly think Yokohama will become unlivable in our lifetime but it could become pretty unpleasant. Imagine Japanese summer from April to October! Would that change your planning? Could it mean your ‘number’ needs to be bigger? The ability to escape Kanto, and maybe even Japan, for several months a year could become a key lifestyle choice. Maybe some people will want to escape for good. Wouldn’t that mean that the cooler, more livable climates in the world are going to see an influx of people who can afford to move? Parts of India are already hitting 50°C as a matter of course. That kind of temperature is more manageable in the developed world with aircon but doesn’t higher demand for a cool place mean higher prices?

As we move from climate change to climate crisis, how are governments going to address it? Again, remember Covid? It was all the people’s fault that it was spreading. They had to be stopped from travelling and confined to their homes in some countries.

Climate lockdowns anyone? Do you think they won’t do it?

It’s a dark thought, but people with flexibility financially will fare better than those who are struggling for money. Does that change your number?

Japan’s economic decline

Honestly, this one would bother me more if I was younger. I’m not sure Japan is a place I would be trying to build a life, career or business given the demographics and the economic outlook if I was in my twenties. But I’m not that young any more and I’m happy where I am. I would, however, want my kids to have the opportunity to live and work overseas if they choose.

The yen is a major concern though. My view is that short term it should recover somewhat when America begins cutting rates. I can see it getting to ¥130 or even ¥120 in the next year or so. However, longer term I expect the yen to steadily lose ground, particularly against the dollar. I talked about it in my ‘How screwed is the yen?’ post a year and a half ago. Staying alert for opportunities to earn in other currencies, investing in a combination of domestic and overseas assets and accumulating Bitcoin remain priorities for me.

Financial shenanigans

Grab your tinfoil hats for this one! In simple terms, the money has been funny since the 2008 global financial crisis. A lot of institutions that should have died were propped up at the expense of taxpayers and we’ve been getting screwed ever since. Economies and big business have become addicted to liquidity: cheap money, low rates. Low interest rates foster inflation, which is a tax on us all, but especially a tax on people who do not own financial assets.

Countries have too much debt and are not producing enough to pay it back. Japan is perhaps the worst offender, at least in the developed world. The debt spiral is probably terminal. That’s why the yen is doomed, and after that so are the pound, the euro and the dollar. I covered currency debasement in ‘Harden up your assets.’ There are tools to fight it that need to be deployed. Otherwise, your money buys less and less.

This is why governments are getting interested in the idea of Central Bank Digital Currencies. (CBDCs) At some point, they are going to need to perform a reset and substitute the current failing money with an alternative. And the powers that be never want to waste an opportunity to seize more control.

In essence, CBDCs are just another form of fiat money. But they come with a whole new opportunity for manipulation. Here’s an interesting video of Rishi Sunak being asked how he would enforce national service in the UK:

Controlling ‘access to finance’ is a government wet dream and CBDCs will make it easy. If you think that the possibility of losing permanent residence due to unpaid taxes is bad, wait until they freeze your bank account or apply a negative interest rate to your money until you pay up.

The public is sleepwalking into this one. You can already imagine how half the population won’t have any issue with it at all. ‘If you don’t have anything to hide, why would you need to keep your money private?’ will be the refrain. People who are well off have no concept of how less fortunate people can run into money trouble and fall behind on bills and taxes. The rich just don’t want to pay for a bunch of ‘layabouts and immigrants’.

The Bank of Japan already has a page on its website about Central Bank Digital Currency by the way. Cute, huh? No plans to implement it at present, but they are looking into it…

CBDC is one thing I think is really worth fighting against, but it will most likely be a losing battle. Sooner or later some crisis will come along and CBDC will have to be implemented ‘for our protection’. You can already see it happening with the AML/CFT mission creep.

Call me crazy, but I think that accumulating Bitcoin and other crypto is the best we can do to prepare for what is coming. Any money sitting in the fiat system will be caught in the net. In many countries, people who want to withdraw a few thousand dollars in cash already have to explain to the bank what they are planning to do with it.

Assuming the number will go up

So there it is. Like you didn’t have enough to worry about! From a financial planning perspective, my take on this is that whatever your number is, you will probably need more.

That’s to say, whatever amount of money you think will be enough to secure your future, maybe add another 10-20% for safety.

This is why I recommend dividing investments into core/strategic and satellite/tactical. The long-term strategic investments are focused on hitting the number. The tactical assets are aiming for a little extra. The crypto holdings are a shot at f**k you money.

Number go up. Act accordingly.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Of the six main asset classes, the one that stands out as perhaps the least understood is bonds. Although most people have a general idea of what bonds are and how they fit in an investment portfolio, they are incredibly complex financial instruments and misconceptions abound. I frequently hear people wonder if there is even any need to own them. So, let’s take a look and see if we can get a clearer picture of how bonds work and why they are useful.

Why do bonds exist?

Bonds are used by governments and corporations to raise capital. If a government issues a bond, it is borrowing money from the public to finance itself. Companies issue bonds so that they can expand operations or fund new business ventures. So if you buy a bond, you are loaning a government or a corporation money.

The key components of bonds

Issuer: bonds can be issued by governments or corporations. Each issuer carries a different level of credit risk, with bonds issued by developed world governments considered the safest. Bonds from issuers with a lower credit rating carry more risk of default and pay a higher yield to compensate for that risk.

Coupon rate: this is the annual interest rate paid to bondholders, expressed as a percentage of the bond’s face value. (often referred to as par value) So a bond with a $1,000 face value and a 5% coupon rate pays $50 a year in interest.

Maturity date: bonds have a specified maturity date when the issuer repays the bond’s face value to the bondholder. Maturities can range from a few months to several decades, influencing the bond’s risk and potential return. A 30-year bond is regarded as more risky than a 5-year bond as more factors can affect the issuer’s ability to repay the debt over longer periods.

Market price: the price of a bond in the secondary market can fluctuate based on changes in interest rates, credit quality and market demand. If the bond’s market value is higher than its face value, it is trading at a premium. If it is lower than face value, it is trading at a discount.

Understanding bond prices

Bonds can be bought and sold on the secondary market after they are issued. A bond’s value in this market is determined by its price and yield. The key thing to understand is that a bond’s price moves inversely to its yield. A bond’s price reflects the value of the income it can provide. So, if interest rates are falling, the value of older bonds that were sold in a higher interest rate environment increases and their price goes up. In a rising interest rate environment, older bonds become less valuable as investors would rather buy newer bonds paying higher yields.

You can see this clearly in the performance of the above iShares TLT long-term treasury ETF. After the 2008 financial crisis, interest rates were kept low to stimulate economic recovery. Just as rates began to drift upwards, Covid happened and rates were slashed again. Bond prices increased significantly in this low interest rate environment and so the price of the ETF rose. When the Federal Reserve began raising interest rates in late 2021, bond prices fell heavily and continued to fall throughout the Fed’s tightening cycle, which is now nearing its end.

You could make a pretty strong argument that now is a good time to be buying a long-term treasury ETF like TLT. When the Fed begins cutting rates, bond prices will recover and investors will be able to capture capital gains along with income.

Conversely, having held interest rates low for longer than most other developed countries, Japan is now in a rising interest rate environment as the Bank of Japan attempts to slow down inflation. This means the price of Japanese Government Bonds is likely to fall.

Why own bonds?

Investors may choose to own bonds for a range of reasons. Those reasons include:

Steady income – particularly applicable to retirees and investors who require income for other reasons

Capital preservation – if held to maturity, bonds issued by institutions with strong credit ratings come with a low risk of loss of capital

Portfolio diversification – bonds offer a good counterbalance to equity market volatility

Capital appreciation – as above, bond prices can appreciate when central banks are cutting interest rates

A hedge against economic downturn – in the US and Europe, inflation is cooling and economies are slowing. This means the income from bonds will be able to buy more goods and services, making bonds more attractive

How to buy bonds

For a typical retail investor, there is no need to buy individual bonds. Just like equities, investors can choose from a range of active or passive strategies offered by bond funds or bond ETFs. Generally, a passive ETF provides perfectly adequate exposure to bonds without any stress or hassle. For example, Blackrock’s iShares ETF series offers 135 different bond ETFs – more than enough to build a diversified bond allocation. The fixed income part of a well-diversified portfolio will generally contain a blend of shorter/medium/longer-term government bonds along with an allocation to more risky corporate and emerging market bonds.

Be sure to pay attention to your base currency when you build such a portfolio. If you are planning to spend the money in the UK eventually, you should be looking at UK Gilts as the core of your bond holdings rather than US treasuries. Don’t be afraid to engage professional help if you are not comfortable organising this yourself.

As to whether owning bonds is really necessary or not, that’s obviously an individual call to make. I would comment that if you are young and just getting started with investing a little money every month, averaging 100% into equity ETFs is a perfectly acceptable strategy for the first few years.

However, after you have been investing for some time and have built up a larger pool of capital, it is probably time to start thinking about diversifying into other asset classes to protect against sharp drawdowns in equity markets. Bonds become a useful tool as you shift from an aggressive capital accumulation strategy to a more balanced portfolio that offers growth and income with a degree of capital preservation.

Hopefully, this post goes some way to explaining what bonds are, how they work and the benefits of investing in them. Feel free to comment or send questions any time!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

With the weather warming up, I’m starting to get the itch to get back out on the golf course. I know people who don’t play the game struggle to see what is so interesting about golf, but I can tell you there is a lot more to it than just chasing a little white ball around the countryside. Golf may be a competitive sport professionally, and many amateurs like to put a bit of money on the line against their mates. However, anyone who has played the game knows that it’s never you against the other player. It’s all about the battle between you and the golf course. Or, more accurately, the battle between you and that space between your ears. If you focus on what the other guy is doing, you are always going to lose. Knowing who the real opponent is is the key to improvement.

The same can be said for investing. If you’re a trader, you are playing a zero-sum game. Every time you win, someone on the other side of the trade loses. However, it’s not like this for investors. It’s not a competition between you and other people. What everyone else is doing is irrelevant. You need to master yourself, and more importantly, you have to know what it is you are competing against.

People tend to think they are trying to beat the market but that is really not the case. The market just is. It doesn’t even know you exist. It’s the sum of all the information available driven by the impulse of human emotion. You cannot conquer this beast. The market just tells you the price of things, no matter how crazy it may seem.

Know your enemy

If you are going to be successful at investing, you better know what you are up against. What exactly is it you are trying to beat? Think about that for a minute. Why is it that you have to expend all this time and energy trying to run your own personal hedge fund? Why do you have to pay some ‘expert’ to guide you through this lifelong struggle? Why can’t you just put your money in the bank and get on with more important things?

The standard answer to these questions can be summed up in one word: inflation. But what does that mean? Well, here’s the definition: inflation is the rise in the cost of goods and services over time. It sounds almost innocent, doesn’t it? The price of things just goes up a little over time, so you should invest to keep pace with it. No big deal right? Any half-decent financial planner can help you put a plan in place to handle that.

The truth is a little more sinister. That 2-3% inflation number that governments and central banks report to you every month is heavily manipulated to begin with. But it doesn’t even come close to measuring the size of the monster that is actually eating up your spending power. The final boss, the thing you are really playing against is much more significant than a natural rise in the price of stuff over time.

What the hell is that you ask? Well, in the old days, when coins were made out of gold and silver, debasement was the act of mixing base metals with the precious metals, therefore reducing the amount of the ‘good stuff’ in money. By using less gold and silver in the coins, the issuer lowered the value of the currency.

These days, debasement takes place when a government prints money, increasing the money supply without a corresponding increase in output. Debasement gifts more money to governments for spending and bailing out their banker friends, and the result for citizens is inflation.

Can you think of a country where that may be happening?

Gold was long considered money, and still is by many people. A good way to judge if your currency is being debased is to take a look at how it is performing against gold.

Gold vs JPY

Hmmmm, maybe printing all that money in order to escape deflation has more than achieved the expected result…

And before we rag too hard on the Bank of Japan, here’s the US dollar. And yes, the chart goes back to 1832 – can you spot where the currency came off the gold standard?

Gold vs USD

If that doesn’t make you mad, I don’t know what will. It certainly answers the question of why we have to spend so much time learning to invest.

You are probably understanding that investing is not a choice here. If you don’t learn how to do it, your spending power is toast. Do you think these governments are going to stop?

If anything, debasement is picking up the pace. The world’s economies took on too much debt and are not producing nearly enough to pay it back. The only way out of this hole is to inflate the currency which means that you and me get screwed.

Oh, and if you want to see what monetary debasement looks like when combined with climate change, take a look at cocoa these days:

Cocoa vs USD

Better stock up on Easter eggs folks!

Yes, all Fiat currency

I know I said let’s not rag on Japan, but let’s rag on Japan, shall we? Finance Minister Suzuki has been out every day this week expressing his ‘concern’ over ‘excessive’ moves in the currency. After printing to infinity, he even had the nerve to blame the weakness in the yen on, wait for it, ‘speculators’!

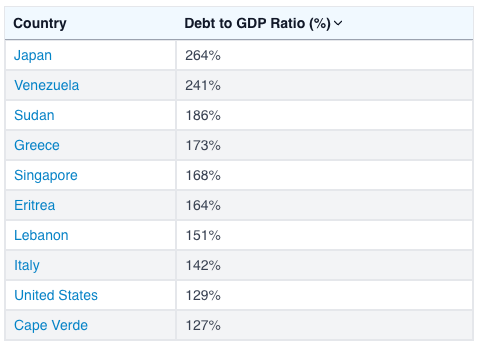

It’s straight-up gaslighting and I’m ‘speculating’ that with debt to GDP at 263%, they are going to continue to incinerate the yen. Don’t get me wrong, this isn’t Turkey – the liras of this world are on their death bed and there isn’t long left to say your goodbyes. Japan has a highly developed and productive economy so the currency isn’t going to implode tomorrow, but have no doubt, it is going to die a slow and painful death and that pain will be felt by you if you don’t protect yourself.

The US dollar is the global reserve currency. This doesn’t free the US from the endgame of its own excessive money printing. It just means it will be the last man standing. All currencies will go down against the dollar. The dollar will go down after the demise of everything else.

No double bogeys!

Back to the golf analogy – I don’t know who said it but there’s a quote that goes something like: ‘A bogey is one bad shot. A double bogey is one bad shot followed by a stupid shot.’

If getting yourself into a position where you have money in yen that you one day want to spend in another currency was your mistake, it’s time to make sure your next shot isn’t a stupid one.

Even if you are planning to stay in Japan and spend your yen here, sitting in cash will devour your spending power. So how do you fight currency debasement? You have to own assets. Assets, like food and other goods, are ‘stuff’. A currency that is being debased goes down against stuff. The Nikkei 225 is not at ¥40,000 by accident. The denominator is going down against shares in companies. Japan’s average land prices rose by 2.3% last year. The denominator is going down against land. I look at my stocks app and a Japanese gold ETF is up over 3% today. It seems like people are getting the message. (great thread about that from Weston Nakamura here)

Harden up your assets

If you’ve been reading my blog for a while, you will be familiar with how I like to structure investments: a ‘core’ diversified portfolio that holds a broad range of assets combined with ‘satellite’ holdings of tactical assets that fit current market conditions. The satellite holdings you want to beef up in order to stave off currency debasement are ‘hard assets’. By this, we mean tangible assets or assets that have a fundamental value. Real estate is a good example. Commodities, especially gold, are another.

You don’t have to buy houses, office buildings and bars of gold to achieve this. You can own Real Estate Investment Trusts (REITs) for a small amount of money. You can own a gold ETF. Is the real thing better? Sure, but we don’t have to be purists about it. The currency is going down against gold ETFs – problem solved.

You’re going to talk about Bitcoin again, aren’t you?

Nah, I’ll just post a chart.

Rock hard supply-capped digital asset vs currency debasement

Happy Easter everyone!

Put this blog post in a tweet

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Happy New Year everybody! I hope you all enjoyed a peaceful winter holiday and are back, raring to go and make big things happen.

For some reason, I had a feeling that this was going to be a challenging year and it didn’t really get off to the best start in Japan. For those interested, I was googling around yesterday trying to figure out the best way to donate to disaster relief on the Noto Peninsula. I found this page run by Ishikawa Prefecture. You can download a form here to request a receipt for your donation for tax purposes. Donations qualify for the donation deduction and there is a useful FAQ on the tax treatment of donations here.

So yeah, earthquakes, runway collisions, fires and we’re only a third of the way through January!

From a personal finance and investing perspective, there is some exciting stuff going on though. The New NISA has launched. I logged into my SBI account and it was pretty simple to get started. I have already set up the ‘tsumitate’ allocation and started buying some stocks for the ‘growth’ allocation. Clearly, everyone else is doing the same thing as the Nikkei is pumping so far this year!

I posted a couple of interesting takes on Japan on ‘X’ yesterday: an optimistic look at the year ahead from Jesper Koll and a much darker look at the demographic issues facing Japan from author Nire Shūhei. It always pays to look at both sides.

So how to invest in the year ahead? If you have been reading this blog over time, you will know that I divide investments up into core and satellite allocations. The core is a diversified portfolio weighted heavily to your base currency that just gets rebalanced once a year. This would typically account for around 70-80% of your investments and the idea is to keep adding to it as much as you can. If it’s a bit dull and boring, you are probably doing it right!

The other 20-30% can be allocated to satellite holdings, which may be a little more racy and exhibit a higher risk-return profile. If this part isn’t fun, then you are probably doing it wrong!

Satellite holdings will change over time depending on the economic environment we are in. So how are things looking?

Some thoughts

On the one hand, things look pretty much like they did for most of last year. The Fed funds rate is 5.5%. People who are obviously long risk assets have been trumpeting the start of rate cuts as early as March, but Mr Powell doesn’t look like he’s in much of a hurry to me. Although the Bank of Japan has adjusted its yield curve control policy and allowed long-term interest rates to rise a little, it is still continuing with its negative interest rate policy. There has been a significant amount of speculation, from both within and outside Japan, about when the BOJ will ‘normalise’ rates – I do love this term, like there is a way to return to normal with government debt to GDP at 264%! Gulp…

Despite noises being made about an exit from negative rate policy, it’s notable how quickly these ideas get put on the shelf. Comments I have heard recently include: ‘The earthquake will make it harder to normalise rates’. Probably true, but any excuse to avoid the inevitable. The Labour Ministry’s November report showed that real wages have declined for the past 20 months in a row, so there’s no sign of the mystical ‘virtuous cycle’ of wages outpacing price rises that would signal a move from the central bank.

It’s not going to happen, is it?

So if you’re waiting for the yen to get back to something sensible against the US dollar, good luck! Markets can remain irrational longer than you can remain solvent enough to go on a nice holiday abroad…

Japanese stocks, for the most part, are loving the weak yen. Any company with significant exports and profits abroad will see those profits magnified when converted back to yen. If you’re wondering why your Toyota shares are doing so well, there you are.

What kind of market is this?

Some time ago, I read the book Reminisces of a Stock Operator by Edwin Lefèvre. It’s considered somewhat of a bible by many investors. While there are some interesting tales of hi-jinks and high leverage, there was only really one key thing I got out of the book, but that one thing has stuck with me: Traders and investors should always know if we are in a bull market or a bear market.

It’s always the simple things that have the most impact, right? The protagonist in the book is a stock trader and his big-picture strategy is very simple: If he is in a bull market, he trades with a long bias. If he is in a bear market, he trades with a short bias. If you don’t know what kind of market you are in, you have no business trading, he says. The author coined the phrase ‘bulls and bears make money; pigs get slaughtered’.

Now, if you are a long-term investor, you don’t have to be concerned with trying to short-sell. You are more than likely to get into trouble. Simply replace the terms ‘long’ and ‘short’ with ‘risk-on’ and ‘risk-off’. Again, I am talking about satellite holdings here. You don’t have to overthink the core part of your portfolio.

Bull or bear?

The Nikkei 225 index gained around 28% last year. After such a positive start to the year, it is widely expected to keep on trucking. It’s pretty clear we are currently in a bull market. If you live in Japan and have a need for JPY base currency, then Japanese stocks are a good place to be.

The only question is what could go wrong? What could bring an end to the bull market?

I think the main short-term danger is a recession in the US. Although the financial press continues to focus on the ‘soft landing’ narrative, history tells us that rate-tightening cycles rarely have a happy ending. Depending on the depth of the recession, US stocks could fall anywhere between 20-50%. I don’t see how Japan just keeps sailing on if that happens, no matter how much better value stocks here may be. If you have already loaded up your investments for the year, I don’t think that’s a bad thing but be prepared to navigate some choppy seas. So it may not be a reason to go risk-off, but be prepared for some volatility.

The BOJ is another matter. If they actually did try to raise rates we would probably experience more than a minor squall. My expectation is they daren’t even try but let’s keep an eye on them. At year-end, I was watching a news feature where they interviewed Japanese business leaders and asked them their views on the stock market for 2024. When asked what they thought was the biggest danger to the Nikkei bull market, the majority of them said ‘the election of Donald Trump’. Interesting…my feeling is these guys need to look a little closer to home.

I’m not even going to get into geopolitics. Lots of risk there, but what are you gonna do?

Outside of Japan, US markets are making all-time highs. However, when you look under the hood, the good cheer is really driven by one group of stocks, known as the Magnificent Seven. If this is a new term to you, the stocks are Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. The size of this group is truly staggering – last time I looked, the combined market cap was around $11.7 trillion. That’s about equivalent to the entire stock markets of Japan, the UK and Canada combined! This group returned around 107% in 2023.

So this bull market is clearly a Magnificent Seven bull market, and the narrative driving it is AI. If you own any kind of global stock fund, go and check their top ten holdings. I’ll bet you that these seven stocks feature prominently.

This group of stocks are a must-own. If you feel you don’t own enough of them, a US recession and corresponding sell-off in the stock market could present a nice opportunity.

Emerging markets could be worth a whole new post, but here’s the tldr: everyone is buying India, not China.

US government bonds got clobbered through this rate hike cycle. If you bought them after the clobbering, you will probably do well as rates eventually subside.

I’m from the UK, so I usually keep an eye on the market over there, but wow, that does not look to me like a place I would want to allocate capital unless I was actually moving back there. Everything about it screams bear…

The biggest bull of all

Of course, the heavyweight champion of satellite holdings is my personal favourite. Yes, the Bitcoin-led crypto bull market is upon us. I already wrote the post on that, it’s right here. You know what to do.

Or do you? I saw a great tweet by Tuur Demeester earlier, in which he said that many people will adopt crypto reluctantly. ‘Hate buying’ he calls it. He also points out how the SEC just ‘hate approved’ the spot Bitcoin ETFs. So why are people going to buy something they hate in the end?

The answer, perhaps, lies in the ongoing debasement of Fiat money, which has accelerated considerably since the 2008 financial crisis. Raoul Pal talks about this a lot and has some great charts. You think your stocks are going up, but really it’s just the purchasing power of your money going down, and you are barely breaking even. People are gradually waking up to this. And there are not many assets that are likely to outperform this money debasement over time. Gold is not getting there. Tech stocks will probably do it, and crypto will likely do it too. Maybe you’re not ready yet, but one day you will be, and you might hate it, but you will probably buy it in the end. Better to rip off the band-aid now perhaps?

On that note, I wish you a happy and prosperous 2024!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

How’s everybody doing? This is a follow-up to my Nikkei ¥40,000? Thinking outside the box piece, which I just happened to post exactly 2 months ago. It’s interesting to see how things have developed since then and then look forward to the last quarter of the year. Yes, I know, it’s almost October. Where did those nine months go???

Remember Monex guy? Two months ago he said the Nikkei 225 was likely to trade in a range of ¥31,000 to ¥33,000 for a while. Gotta give my man credit there, it’s done exactly that. His expectation was that if we can break above that range, we’re heading for ¥40,000. What do you think about that?

If there’s one thing I’ve noticed recently, there’s been a subtle narrative change around the Japan stock market rally. In the first half of the year, it was exactly that – Japanese stocks were broadly rising and outperforming most other developed markets. What has changed, is that the narrative in the news now is more focussed on a Japanese value/dividend stock rally.

So what happened? Well, first, the Bank of Japan has allowed long-term yields to rise up to 0.70% and beyond and then, on 9 September, BOJ Governor Kazuo Ueda said that the lifting of the central bank’s negative interest rate policy will become an option if wages and prices rise. He even said they might have enough data to make a call on that by the end of the year. Despite the talk of interest rates rising, with inflation at over 3%, Japanese investors are realising that sitting in cash is a losing trade. With bonds still offering negative real rates, the money has been pouring into dividend-generating stocks. There’s also a possibility that the revamping of NISA for 2024 has got investors more excited about getting involved in the stock market.

I know it lacks class to say I told you so, but sometimes you need to toot your own horn. This is stuff I figured out some time ago. On 14 September, Nikkei News Plus 9 did a feature on the Nikkei 225 High Dividend Yield Stock 50 Index. There is an ETF that tracks this index and I have owned it since spring 2022 and I covered it in posts in March and October. Here’s what it looks like year to date:

Not bad at all. Ok, enough self-congratulation, there is still a lot to think about here. The big question is, how is this going to play out over the remainder of the year? The fact that financial news programs are starting to fixate on the value/dividend stock narrative is good news if you hold these stocks. Just since the feature on the Nikkei program last week there has been a notable bump in the dividend ETF along with bank stocks, shipping companies, trading companies and steelmakers, which News Plus 9 showcased as examples. So this is now a hot trade which could run for a while, particularly as the talk of exiting negative interest rates heats up. Pick a banking stock and take a look at its performance year-to-date and particularly over the last few weeks!

When a sector gets hot and retail crowds in, it’s often a sign that we are nearing a top. The mania phase can last longer than you expect, but it can also blow off in a hurry. If I didn’t own these stocks already, I don’t think I would be jumping in now. As I mentioned in the July post, these are tactical positions for me, so I am keen to lock in some profit, while also remaining invested to catch any further upside. I have sold incrementally over the past 2 months and reduced my holdings by about 30%. Of course, with hindsight, I feel pretty silly selling anything. I could have just waited and sold higher. But that’s the way it goes – you have to make decisions based on the information you have in real time. So I took some profit, but left two thirds still invested. So far, so good.

So is the Nikkei going to ¥40,000 this cycle? I would be happy to be wrong on this one, but my bet is no. Higher rates, or at least the talk of higher rates, are bad for growth stocks but can be good for value as we are seeing. You would need both to be going up to hit the ¥40,000 mark.

I am still of the view that any attempt at normalising rates in Japan will lead to chaos and a hasty reversal. However, as we are seeing now, even talk of an increase is enough to change market dynamics. And if last night’s Nikkei News Plus 9 program is anything to go by, there is a lot of talk going on! They were feverishly covering how some net banks are raising their rates for fixed deposits to a hefty 0.70%!

From the BOJ’s perspective, a lot of this talk on rates is just that. There’s even a term for central bankers talking up a strategy in order to get the reaction they want from markets – jawboning. It doesn’t change the corner they have painted themselves into. It’s not looking good for the yen folks…

Of course, a lot also depends on the US. Last night’s Fed decision to leave rates unchanged and the plan to hike once more this year was as expected. As they always do in this situation, the Fed is talking up a soft landing. History is not on their side on that one. As the effects of this hiking cycle gradually feed through to the underlying economy, the smart money is still betting on recession. Markets are too interconnected for Japan to keep sailing on if that’s where we are headed.

So no ¥40,000 in the near future, but there could be some more upside for value/dividend stocks. Early next year may get interesting if the BOJ tries to translate some of this talk into action. I plan to have a ready supply of dry powder to allocate if we do take a dive. That’s my view, which I will look extremely foolish for putting in writing if we see ¥40k by Christmas! But if you’re going to invest tactically, you’ve got to have an opinion. Perhaps I should buy a Monex hat to eat if I am wrong…

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I have been meaning to write this update for a while. In particular, because people keep finding an article I wrote about the ‘New NISA – Coming in 2024’ and telling me it is out of date, which it most certainly is! You see, that was the old new NISA plan and since then there is a new new NISA plan, which is even bigger and better. Clear? Apologies for the confusion and for my tardiness in updating – the old article will be consigned to the fires of internet hell just as soon as I get this one written and posted.

If you’ve read this blog before, you may be aware that I care very little about product. By that I mean, if you are buying a box to hold things, I don’t care if you get the blue box, the pink box or the rainbow box. It’s just a box, after all! There are a number of NISA products out there offered by online brokerages and banks. I hear even the Japan Post Bank is getting in on the act. My preference would be for the online brokerage accounts, but that’s mainly because I am terminally online and want to minimise time spent ever talking to staff at the bank! If the post office works for you, have at it!

What does get me excited is what you put in the box. That’s where things get interesting. I already wrote a post on How to choose investments for your NISA, so please check that out as a compliment to this post.

So, down to the nitty-gritty. How does the new NISA work? My NISA is with SBI, and they wrote a little guide with some ‘helpful’ graphics – see here. Google translate works ok on the main body of text but the graphics remain in Japanese. I’m really linking to this so you don’t rely entirely on this post to remain correct. Keep an eye on official sources in case something changes before launch.

In short:

You can invest up to ¥3.6 million per year – ¥1.2 million has to be invested in mutual funds, and the remaining ¥2.4 million can be invested freely. That means ETFs and direct stocks are on the menu.

The investment term is unlimited – so ¥3.6 million a year for 5 years = ¥18 million. This is the fastest you can fill it up, but you can actually take as long as you want to reach the ¥18 million limit.

The holding term is forever – there is no limit on how long you can hold the assets in the NISA. As long as you don’t sell, dividends will be paid tax-free and there will be no capital gains tax when you do eventually sell.

All in all, it’s a pretty good deal! I plan to be maxing out my allocation for each of the five years before making any investments into taxable accounts.

If you have an existing NISA, you will not be able to make any new contributions to it after the end of 2023, but you can choose to keep the money invested until the end of the term. For example, if you started a regular NISA this year and invested ¥1.2 million, you can leave that money invested, tax-free, for another four years. Any new contributions will go into the new NISA. If you have a Tsumitate NISA with 15 years remaining, you can choose to leave the money contributed up until the end of 2023 in there for 15 years. Again, from 2024 any new contributions will go to the new NISA.

Investment Strategy

I encourage you to give some thought as to how to allocate the investments in the new NISA. Again, the post I mentioned earlier may help.

There is one trade-off I am particularly focussed on here: growth vs. income. Your forever NISA investment will benefit from not being charged the 20% tax on capital gains or dividends. So which should you try to maximise? The short answer here is probably a combination of both, but let’s do some thinking about it:

For the ¥1.2 million per year that has to be invested in mutual funds, I don’t think it will be possible to generate income. Mutual funds generally re-invest dividends, so they are part of the investment return, but unless they have a distribution share class, they don’t pay dividends out. If anyone finds a mutual fund, available for NISA, that actually pays out dividends, please do chime in – I would be very interested to hear about it. For now, I’m going to assume that such funds are not available. In that case, for the ¥6 million (¥1.2 mill x 5 years) that you invest in mutual funds, it would make sense to go for growth. I will be looking for high-growth-focused funds for this part of the allocation. (note that growth stocks generally pay no/low dividends as any earnings the company makes are reinvested to spur further growth)

For the remaining ¥2.4 million a year, that’s ¥12 million, I am tempted to strongly focus on dividend-paying stocks and/or dividend stock ETFs. If you can generate a 4% dividend return on ¥12 mill, that gives you a tax-free ¥480,000 per year in income alone. And, of course, these stocks will probably also grow in value over time if you are patient. Now, nobody is retiring on ¥480,000 a year but over 25 years, for example, that’s ¥12 mill in your pocket. Not bad, huh?

Of course, there’s a pretty good argument for investing the ¥12 mill into a fund that reinvests the dividends so you get the compounding effect over the term of the NISA. I have no objection to that. I just like the idea of collecting my ¥480k tax-free every year and either spending it or reinvesting it myself.

Also, after a discussion with Ben at Retire Japan, I discovered that under the new NISA rules, you can sell assets and then re-use the tax-exempt amount to invest in a different asset, which is a huge improvement on the current system. Thanks, Ben for pointing that out! See this FAQ on the FSA website.

So those are my thoughts. I would love to hear from anyone who looks at the NISA opportunity differently. Drop me a line or come and tell me I’m wrong on X. (yes, we have to call it that now…)

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.