It’s a slow week for stocks in Japan, with the market losing ground in part due to the selling of names that went ex-dividend on 29 September, and also out of concern over a possible US government shutdown.

29 September was the cut-off date to receive the next dividend for many Japanese stocks. Prices are often driven up before the ex-dividend date, only to fall after it has passed as investors sell, safe in the knowledge that the next dividend payment will be delivered. It’s really a non-event for long-term holders.

A US government shutdown could lead to a delay in the release of key economic indicators such as jobs data. How can we possibly know when to panic sell our stonks if we don’t know how many jobs were added/lost last month in the USA?

Despite the relative gloom, the focus for Q4 is increasingly on a potential melt-up for markets as liquidity continues to flow. Tech stock valuations are admittedly high compared to the 20-year average. However, compared to the last 5 years, the premium is significantly lower. People looking for the bursting of the AI-driven bubble may have to wait a while longer. This article suggests that Wall Street strategists, including Jim Paulsen, are starting to look at high valuations as a kind of “new normal”:

“There’s something weird going on with valuations from what they used to be — that is, there’s an upward trend in the valuation range,” said Paulsen, who now writes a Substack newsletter called Paulsen Perspectives.

Will gold keep going?

People keep asking me if gold can keep rising. The best answer I have is: unfortunately, yes. Gold ripping to all-time highs, while exciting for goldbugs, is not a good sign overall. There’s a distinct lack of trust in governments and central banks to manage their debt and spending situation.

The dollar certainly doesn’t like it:

DXY US Dollar Index

As for the yen? Well, the dollar index is down almost 10% YTD and USD/JPY is still at 148. If you are waiting for a stronger yen, you’d better hope the BOJ gets back to raising rates soon. Your mortgage won’t thank you if they do, though…

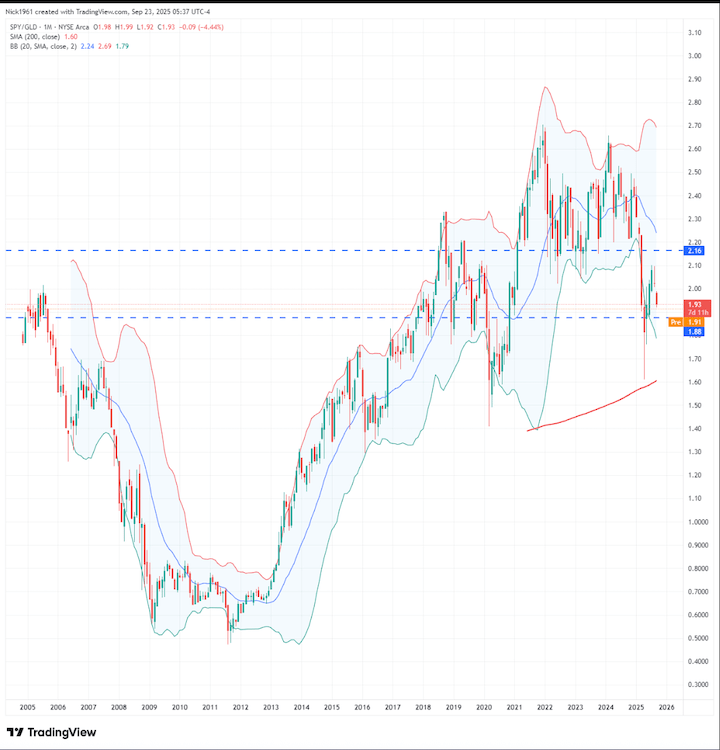

Talking of gold, here’s a chart for people to really hate on!

SPY/GLD

That came from this post by Nick G: “The price of equities is completely unchanged since 2005. All that has changed is the value of the denominator.”

So, priced in gold, the S&P 500 went nowhere since 2005. All “gains” were just the dollar losing value. And that includes dividends, apparently!

No wonder people are hyper-gambling on crypto and tech stocks…

Here’s an interesting (perhaps triggering) opinion piece on financial repression and why you want to own gold, silver and Bitcoin in the face of what’s still to come.

Speaking of which…

All eyes are on Bitcoin now as we enter Q4. If stocks remain strong into year-end, what will Bitcoin do? No price predictions from me, but I see a melt-up before a melt-down. This year’s theme has been long-term holders (who bought at rock bottom prices) enthusiastically selling to institutions that are hungry to secure their share of the network. If the OG’s put a pause on selling, look out above.

I’m hearing lots of talk of an extended cycle, a move to a 5-year cycle, and even a supercycle. I heard these same things in October 2021. I’m not saying the theory is wrong, but it was very wrong last time. I’ll believe the 4-year cycle is no longer relevant when I see the evidence. Until then, sign me up for a Q4 meltup followed by a treacherous 2026.

Quantum Leap?

I wrote a post in late 2024 about Quantum Computing. Almost nobody read it. Very few people are discussing QC or even aware of what it is. For me, it’s turning into a no-brainer satellite holding. Incredibly volatile, but with massive potential. Don’t bet the farm, but maybe study up a bit?

⚛️ Quantum is growing faster than anyone realizes — and it could disrupt everything, even Bitcoin. @Jamie1Coutts and @caprioleio.

Valued at just $52B, this misunderstood tech may be the biggest opportunity of the next decade. pic.twitter.com/6Ko1IoyhB8

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I sometimes struggle to convince people to allocate to gold; some see it as an unproductive asset, while others find it boring. It’s only when it takes off that everyone wishes they owned more.

So, why is a safe-haven asset making all-time highs at the same time as the stock market? In fact, why is gold outperforming a hot stock market this year? Isn’t it supposed to go up when stocks are beaten down and investors are panicked? What’s behind this move?

The answer is relatively simple: gold is rising because the market expects higher inflation and higher deficit spending. While central banks control short-term interest rates, they can’t dictate the direction of long-term rates. The bond market is clearly signalling the expectation of higher inflation.

Makes sense? Let’s look at the world’s most important bond market. As the US deficit approaches $2 trillion, the government is issuing more debt. More supply means bond prices are falling. International investors would normally view US bonds as the premier safe haven. Now they are looking elsewhere.

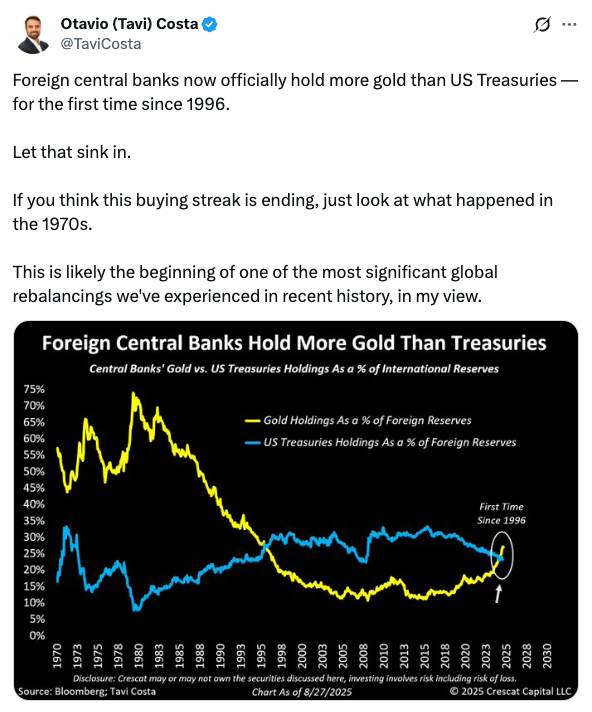

Yes, central banks themselves are upping their allocation to gold ahead of treasuries. Meanwhile, many of them are cutting rates into rising inflation due to concerns about unemployment. If Jerome Powell’s Jackson Hole speech is anything to go by, the Fed is about to join them.

The one central bank that is actually looking to raise rates is right here in Japan. However, it looks like the BOJ has already lost control of the long end of the bond market with the 30-year yield now over 3.2%. Remember, rising bond yields mean falling bond prices. No wonder gold is at an all-time high in yen…

Ray Dalio can be a little long-winded, but if you are trying to understand the economic environment we are in, it’s worth reading this interview with the Financial Times. Apparently, the FT was not entirely accurate in reporting his responses, so he published his answers to their questions in full.

For those who are pressed for time, here’s a quick summary (I will try not to mischaracterise the man!):

America’s debt problem is not new. It is due to decades of excess by both republican and democratic governments

It’s likely to become a major problem in around 3 years

If Trump succeeds in bending the Fed to his will, US bonds will lose even more trust and demand for them will continue to fall

Letting inflation ‘run hot’ is also bad for bonds and for the US dollar

There’s more covered in the article, but you get the gist. The debt problem is not specifically Trump’s fault, but his actions are only going to exacerbate it.

Bad for bonds, good for gold. This doesn’t mean sell all your bonds and buy gold, but if you are running a diversified portfolio, you can expect the bonds to perform worse and gold to perform better for a while. The MOVE Index, the bond market’s equivalent of the VIX, has risen over the last few days. If you see that continue to move higher, look out for an increase in bond market volatility.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Bitcoin, which has a habit of leading big moves in stocks, made it down to $109k from a peak of $124k. That move appears to be done for now, and it’s consolidating at around $111k. Tech stocks wobbled slightly, but nothing major so far. Nvidia earnings are on deck tonight – that’s always a big event. No doubt the dominant chipmaker will kill it, but will it kill it enough? Expectations could hardly be higher.

I don’t see Nvidia earnings being bad enough to tip the market over. Maybe a couple of days of turbulence if they are not quite as spectacular as everyone hopes?

More importantly, Jerome Powell’s Jackson Hole speech was surprisingly dovish. Stocks rallied in the aftermath, and Bitcoin put in a massive green candle that was quickly retraced. Then yesterday, Trump moved to fire Lisa Cook. As crazy as that is, the market took it in its stride. Imagine if any other President had manoeuvred so brazenly to gain control over the central bank and bring rates down…

I ended my post last week hoping for a bit more euphoria before the chaos ensues. It’s looking like I might get my wish. Trump doesn’t want rates lower for nothing. He wants to pump the markets. Plus, his businesses own a ton of crypto.

Where are the Robin Hood gamblers going to get their funds from when their cost of living keeps rising? Cash handouts from Trump? You can’t write anything off these days…

And then, today:

Well, well, well…

A few other observations

Remember Metaplanet? The haters have been running victory laps the past few weeks after Japan’s leading Bitcoin treasury company saw shares tank from their ATH of ¥1,930. Now it trades at ¥862. It’s no big surprise, however, I think few people realise that the treasury company mania didn’t end – it just moved elsewhere. Copycats have been popping up left and right. Also, stablecoins are the new hot topic.

Check out the recent price action on some of these tickers: 8105, 3853, 7422 – a ball of hot money is chasing them relentlessly, and most of this money likely came out of Metaplanet. Bigger names, like SBI Holdings (8573 ), have been pumping, too. (possible rate hikes and crypto behind this one) Monex Group (8698) is up big today on reports that it is considering issuing a yen-pegged stablecoin.

I’m not saying people should be chasing these names, but the hot money didn’t just go away. And don’t discount some of it coming back to Metaplanet in the next few weeks/months. They own the most Bitcoin, and Eric Trump (who is on the board) is coming to Japan soon. He’ll be keen to pump up the crowd.

The Japanese Prime Minister addressed a crypto conference in Tokyo this week. File that under ‘things I never would have imagined’.

We may be in the final innings, but that’s usually when the really crazy stuff happens…

I’m not leaving!

Rate cuts? Rate hikes?

After Jackson Hole, the market is now thoroughly convinced that the Fed will cut in September. That outcome is being front-run already. There will be a revolt if Powell doesn’t follow through…

What will the BOJ do? No idea, but the consensus seems to be for a small, cautious hike.

In the bigger picture, Trump is going to pump liquidity one way or another. That’s great news for risk assets in the shorter term and pretty terrifying on a longer time frame. The US doesn’t really need lower rates. If anything, inflation is likely to accelerate into the end of the year.

The pump could be spectacular. The dump is gonna hurt.

Plan accordingly. Keep your core portfolio in balance and otherwise leave it alone. Maybe take a critical look at your riskier satellite holdings and how you are positioned for what may be to come. If we get the pump, you know what comes next.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Chaos by Christmas? I do like a bit of alliteration, but this doesn’t sound good.

That nifty little turn of phrase came in a message from a friend. He’s been concerned about the way things look for a while, even as markets melted up following the Liberation Day debacle. The chaos message was timely, as I was already working on this post.

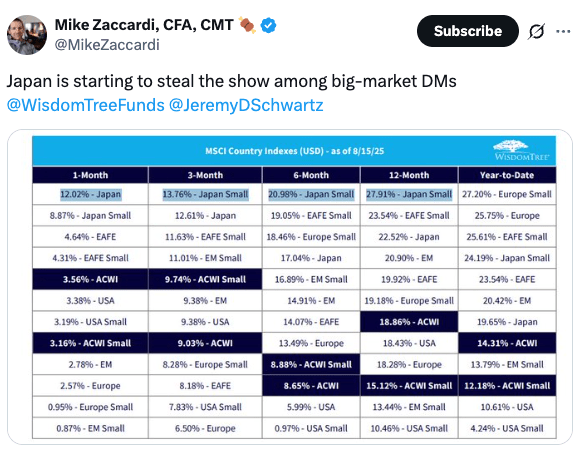

Exhibit A: Wall Street’s New Obsession? Japan’s Market Just Went Vertical – a short article about foreign investors returning to Japan in size. The Nikkei 225 is at real deal all-time highs. You see the latest price on the news each night. Is there perhaps a little euphoria creeping in?

Expectations are high. The Fed is supposedly going to ease in September. The BOJ seems to be due to hike. But will they? Federal Reserve Chair Jerome Powell is set to speak at Jackson Hole this week, but I doubt he will give much away. He has been under considerable pressure from the Trump administration to cut rates and has held firm so far. There are signs of cracks in the job market, but does JPow really have enough data to justify a cut? We’ll see, but I’m sceptical.

The same goes for the BOJ. Pressure is also coming on Governor Ueda from the US administration. Does the central bank feel certain enough about the inflation outlook and tariff outcome to take the plunge? One thing is certain: if the BOJ is going to hike, it will be leaked ahead of time. No one wants a surprise like this time last year. If you don’t hear anything in the days before, expect no action.

In the US, the S&P 500 is also pushing all-time highs, driven as ever by the Magnificent 7 tech stocks, which are driven in turn by the AI boom. Despite the furore over job numbers, the consumer seems to be doing ok on the face of things. However, the tariffs are yet to show up meaningfully in the data. Expect that to change soon.

Where are the Robin Hood gamblers going to get their funds from when their cost of living keeps rising? Cash handouts from Trump? You can’t write anything off these days…

It’s not just eggs that have gotten expensive:

The final innings for crypto?

Bitcoin topped $124k last week and has now ‘crashed’ to $113k. Ethereum went on quite a run and got the crypto bros fired up about the alt season they’ve been waiting for. If history is anything to go by, then the next couple of months should mark the top of this cycle. I have no idea where it goes in that short time, but you should probably block out the people calling for $200k by the end of the year. $120k was my best guess, and we have done that. Maybe there’s a little more left in the tank, but who knows? When it feels euphoric, that’s the signal. The fear and greed index shows fear, so I’m not feeling it yet…

What to do?

Expecting a bit of chaos and doing something about it are two different things. And maybe there is no need to do anything other than just mentally brace for a correction. After all, prolonged bear markets are illegal these days. (I jest, kind of. See: It’s going up forever, Laura)

Let’s do Japan first:

I have thoroughly enjoyed the interaction on X between investors in Japanese stocks over the last few years. What a glorious time to be invested in this market! Japan has clearly turned a corner, both in terms of putting the bubble-era all-time high behind us and making strides in corporate governance. But at ¥43,000 in August, things feel a little hot. I don’t think there’s reason to panic and dump your J-stonks, but with almost everything going up, it’s perhaps time to take a look at holdings that you might have got a little lucky with.

For me, that means going through my list and asking myself some basic questions: Why do I own this? Am I happy to hold it through a storm? My Japan account holdings now span two pages. I think I may have a few too many stocks. For some of them, I don’t really remember why I bought them in the first place. Would I buy them again now?

The majority of my holdings were bought for the dividends. That’s my way of keeping up with inflation and currency debasement in yen. I actually didn’t expect them to go up this much. I’m pretty comfortable keeping them and collecting my dividends through whatever may be on the horizon. NISA I won’t touch at all – that was all bought for a long-term hold.

I would like to get my holdings back to one page and a bit more dry powder in the cash account.

How about other markets?

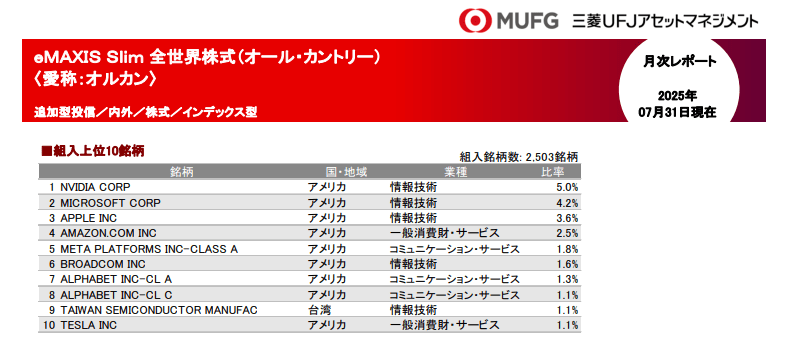

You may own a bit of everything in your All Country fund, but performance has really been driven by tech stocks. Here are your top 10 holdings:

Is tech dominance going to ease? Bank of America thinks so. You may know from my previous posts that I believe that tech stocks and Bitcoin are the two assets that will reliably outperform currency debasement. Are they due for a correction? Maybe. Is the AI bubble going to burst? Probably, but what do we mean by ‘burst’? The AI genie is out of the bottle. It’s not going away. The world will continue to hunger for more computing power. I don’t feel like selling any of this stuff, but I would like to have some dry powder to buy more when there’s a panic.

Got it, but we sell all the crypto, right?

I have said before, you need to have a plan for crypto and execute as best as you can. It gets harder the higher the level of euphoria.

My two cents: I’m not sold on the idea of dumping actual Bitcoin in order to buy it back cheaper. It comes with its own risks: the treasury companies and BlackRock suitcoiners want as much as they can lay their hands on. I don’t want to sell to them and then struggle to get it back later. Plus, the tax reporting is a pain!

ETFs are not Bitcoin; they are Bitcoin exposure. They can go. The treasury companies are probably going to be the FTX/Luna of this cycle – beware. Alts are struggling to attract enough attention and money in the middle of a bull market – you don’t want them hanging around your neck next year when everyone is depressed. (see my February post, Exit liquidity)

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I am reading “When Genius Failed: The Rise and Fall of Long-Term Capital Management”. It’s the remarkable story of a ’90s hedge fund comprising a group of big-brained academics, including Nobel Prize winners, who were so convinced that their models were infallible that they built a gigantic book of highly leveraged derivative trades. Even if you’re not familiar with the story, you can imagine how that ended.

The smart money doesn’t always win.

One of my favourite books is Jon Krakauer’s “Into Thin Air”. LTCM is like the hedge fund version of that cautionary tale. Hubris and leverage are a dangerous combination. The academics somehow convinced themselves that they had modelled out every outcome, and even if things went bad, there would always be enough liquidity to get out of their positions. Of course, ‘one in a million’ events happen more frequently than we expect, and when they do, nobody is around to buy what you desparately need to sell.

At least we learn our lessons, right? Well, LTCM blew up in 1998, and it was only 10 years later that Bear Stearns, which was closely linked to the fund, faced its own meltdown.

There’s a lot to be said for keeping things simple. Viva le dumb money!

Wait, isn’t this site supposed to be SMART Money Asia?

This is easily the greatest meme ever created. It applies to so many areas of life, and none more than investing. The LTCM guys were just too far out on the right of the curve that they no longer lived in reality.

Generally, the smart money and the dumb money follow the same strategy. They buy risk assets and sit on them. In my previous post, Liquid Refreshment, I covered how tech stocks and Bitcoin are the two things that outperform currency debasement. And what do the Robinhood degenerate gamblers do? They buy Mag 7 and IBIT and print money. When these assets dip, they buy more! What are the older, wiser retirement accounts buying? NASDAQ and IBIT, by the looks of it!

Wait, is the diversified portfolio guy telling us to just buy tech stocks and Bitcoin?

I have always said, if it’s a meaningful amount of money, you should have a core diversified portfolio weighted toward your base currency for about 80% of your wealth. You can allocate 20% or so to satellite holdings to take advantage of opportunities for higher returns. This is where you can go hard on tech stocks, gold, commodities and Bitcoin/crypto as you wish.

Overthinking and mid-curving are the killers. See my post, It’s going up forever, Laura, on why dumb money wins in the end.

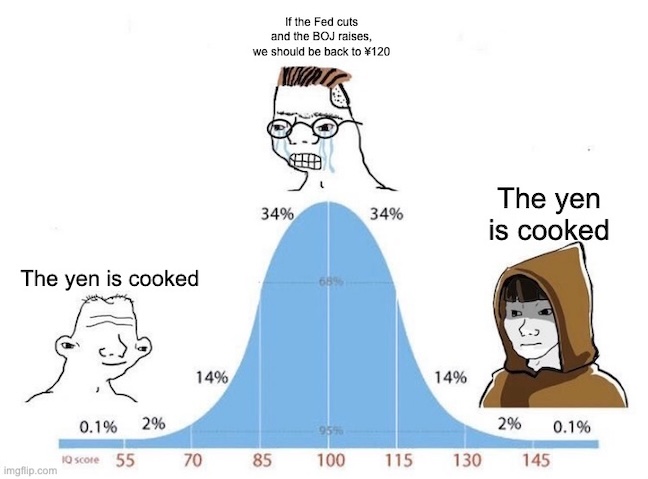

I see that USD/JPY is back at ¥150. Let’s do the meme:

Simple!

Of course, mid-curve guy is right. Short-term, barring any crazy events (which happen a lot!), the yen should strengthen against the dollar. However, if you are doing long-term planning and trying to figure out how currency could affect you, it’s pretty clear that the country with the worst debt/demographics profile is going to lose against the country with the global reserve currency.

Plan accordingly.

Trump wants rates lower, and Powell won’t play ball. So, Trump and Bessent will find ways to work around Powell and add liquidity regardless. This is bullish for stocks. If there is some kind of panic and a dip in stocks in the meantime, they will turn on the fire hose. Back up the truck and buy the dip!

The TSE apply pressure to listed companies to improve their governanace and return capital to shareholders – it’s a great time to own Japanese stocks if you have a JPY base currency need! (not so great if you don’t, see above)

Every four years, Bitcoin goes down around 80%. Then it spends about a year floundering around and recovering slightly, and the next two years in a powerful bull market. If it goes down 80% next year, you swing like Happy Gilmore!

See how it works? Dumb money stays winning!

Have a great weekend.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

The hot summer months usually mark a quiet period for markets, but there are no signs of a lull so far this year.

While the upper house election last weekend likely had a limited impact on stocks, the trade deal announced shortly after certainly got things moving. The Nikkei 225 index surged over 3% on 23 July and is creeping up on ¥42,000 as I type today.

Shigeru Ishiba may have lost his ‘mandate from heaven’, but the Japanese auto industry is saved!

Perception really is a funny thing. Automaker stocks surged yesterday as investors cheered a 10% ‘reduction’ in US import tariffs from the 25% touted by Trump. However, before Trump took office, the tariff on cars was 2.5%. So there has actually been a 12.5% increase. Trump’s big stick negotiation tactics may be crude, but they appear to be working.

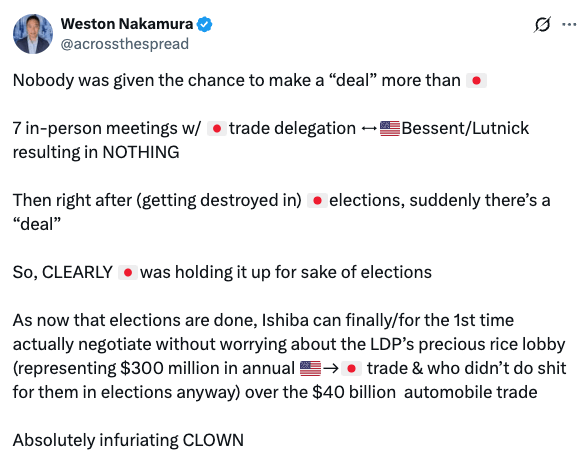

By the way, Weston Nakamura isn’t buying the coincidental timing of the trade deal announcement.

Probably the biggest pressure release for markets will be the end of tariff uncertainty. If Trump can secure a similar deal with the EU, then we are likely through the worst of it.

He’ll still have to come up with a pretty big distraction from the Epstein files, though, so we should stay on our toes.

Anyway, moving swiftly on

I find a lot of people struggle to understand the concept of currency debasement. If this is you, I highly recommend this episode of Forward Guidance with Raoul Pal and Julien Bittel:

You only actually need to listen to the first 10 minutes to get the picture, although it’s all good stuff.

A quick summary:

Governments restructured their debts after the ‘debt jubilee’ that followed the 2008 financial crisis, forming an almost perfect 4-year liquidity cycle

We’re in the 4th year of that cycle now, where the larger part of the debt is due

The liquidity that gets added never really gets taken back and is rising at a rate of around 8% per year

That is about the rate of debasement of fiat currency

If you divide an asset by the rate of global liquidity, you find out it’s true performance vs debasment

The S&P 500 is basically flat, same with other countries’ indexes

Gold is also flat, as it should be

The only assets that outperform debasement are tech stocks and crypto

Governments are now just servicing their debt. i.e. paying interest and not repaying the principal. GDP is falling due to the declining birth rate and shrinking labour force. And so, governments are debasing currency to pay for the debt.

Until political parties appear that are willing to tackle this problem, elections and politics are pretty much meaningless when it comes to investing. And, of course, no party wants to deal with the giant elephant in the room as it will mean years, likely decades of pain. That’s the reality. If you don’t want your spending power to get eroded over time, you need to be invested appropriately.

Now, should you only own tech stocks and crypto? Clearly not. But, in my humble opinion, you would be crazy not to have an allocation to them.

Incidentally, the Bitcoin 4-year cycle dovetails remarkably neatly with the 4-year liquidity cycle. I have come to realise that this is also not a coincidence. In fact, BTC lags global M2 money supply by around 90 days. Here is Julien Bittel’s chart of projected M2 from back in May:

Are you surprised that BTC is now near $120k? You shouldn’t be!

Now imagine if the Fed cuts rates in the next few months…

As long as that M2 line keeps going up, expect risk assets to follow. If you see it turn down later this year, that’s the purest signal possible that the Bitcoin bull market is nearing its end.

Inject that chart directly into my veins!

If you want to get deep into the weeds on liquidity, Arthur Hayes writes some entertaining posts. His latest is here. Be warned, Arthur is a liquidity/crypto uberbull.

Meanwhile, here in Japan, stocks are in celebration mode. I don’t see any reason to fade the mood, although my bullishness is always tempered by the fact that I’m living right here next to the canary in the debt/demographics coalmine.

You can only worry so much, though. Stay cool, and if the world ends, it will probably be a great time to buy stocks!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I’ve been getting asked about Bitcoin storage lately, so I thought I’d write a post on the topic. People rightly point out that one of the major obstacles to mainstream adoption of BTC is how difficult it is for the average person to store it safely. It’s actually one of the reasons I believe we are still relatively early in the adoption cycle, as it’s simply a problem waiting to be solved. Or at least made easier.

People have perhaps become all too accustomed to handing their assets over to ‘trusted third parties’ for safekeeping. Looking after your own Bitcoin keys is a degree of responsibility that most people are simply not used to taking on. It’s actually one of the things that fascinates me about the asset class – you have the choice of how much you want to actually be in control of your money. Custodial services are going to become more sophisticated going forward, but there will always be purists who want to manage their own keys.

What keys?

Non-Bitcoin people are probably already confused by the term ‘keys’. Put simply, you do not actually store Bitcoin itself. You store the private cryptographic keys that give you permission to access that Bitcoin. If you do not have access to your own keys, the coins can be taken from you – hence the mantra that forms the title of this post.

This doesn’t necessarily have to be done online. You can simply write your keys down on a piece of paper. If you are lucky enough to have a photographic memory, you can even store them in your head! Most people are going to want to use some kind of wallet, though.

Exchange risk

People generally purchase Bitcoin on an exchange. It’s very tempting to just leave it sitting right there. After all, it’s password protected, and you have set up 2FA. What could go wrong?

Exchanges get hacked. It’s happened many times before, with some of the biggest hacks occurring in Japan. Non-Bitcoin people may even have heard of Mt Gox, which went down back in 2014. It was by no means the last exchange to get hacked, with Coincheck suffering an attack in 2018 and DMM getting hacked more recently. Exchanges may also fail due to fraud and mismanagement, as FTX did in 2022.

Japan is interesting, as the FSA is incredibly strict and requires exchanges to keep enough reserves to cover customers in case of a hack. It’s actually one of the few countries in the world where you stand a reasonable chance of getting your money back in the event of a breach. But do you really want to take the chance?

What about small amounts?

If you only have a small exposure to Bitcoin, buying a cold storage wallet, setting it up and managing it seems like a lot of hassle. I get why people sometimes just leave coins on the exchange. However, everyone has a point where the amount of money becomes too big to stomach a loss, especially from a well-documented risk that you should have known better about taking. It’s really up to you to decide when you have reached that point.

Here’s the thing, though: people tend to think in terms of today’s value. They look at the amount of BTC they have and today’s price and say, “ok, I’m not going to go to the trouble of moving my coins off the exchange for this trivial amount”. What I would encourage people to do is think in terms of potential future value – if you lose your Bitcoin today, it’s gone. If the BTC price rises to $1 million per coin in ten years, how mad are you going to be that you didn’t protect it???

If it’s on the exchange, not your keys, not your cheese. North Korean hackers will never stop trying to get it!

Here are a few things to consider if you have decided it’s time to start looking after your holdings:

Online/offline

The first tradeoff comes with online vs. offline wallets, sometimes also referred to as hot and cold wallets.

It’s pretty simple: if your wallet is on a device that is connected to the internet (hot), it’s very convenient to use, but more susceptible to an attack. That’s why you hear Bitcoiners talk about putting their coins in cold storage. Take the keys offline, and it is much more difficult for a bad actor to get to them.

Custodial/Non-custodial

Once you have decided you want to get your keys offline, your next choice is whether to get a third party to handle it for you or do it yourself.

Of course, custodial services mean trusting someone else to manage your keys. The good ones will do this very well, perhaps better than you can yourself, but they won’t do it for free. You have to be very careful choosing a custodian and making sure that they really have your coins in cold storage and are not, in fact, lending them out to other parties and putting them at risk. Do your homework! If something doesn’t add up, there will be a reason. If a custodian is offering you a high rate of interest on your BTC, for instance, you are going to want to know where that yield is coming from and whether your coins are being put at risk to generate it.

Maybe custodial isn’t the easy route after all – it does require significant due diligence. Even after that, you have to trust the custodian to do what they say they will do.

Non-custodial cold storage

What most Bitcoiners have already figured out is that if you want a job done properly, you should do it yourself! Assuming we are not just writing our keys on paper or memorising them, this means purchasing a hardware wallet.

There are many hardware wallets available. The two best-known are made by Trezor and Ledger. I have used both and prefer Trezor, but it’s just my personal preference.

In terms of how to use these devices, I will try to keep it simple for now: buy one and follow the instructions to set it up! Tech-savvy people will find it easy. If you live in the world and have set up new computers, phones and other devices, it’s not going to be too difficult. Getting your ageing parents to use one might be a stretch…

When you set up your device, you will be guided through the process of generating a seed phrase. Here’s a definition from the Leger website:

You will want to handle your seed phrase properly. It essentially functions as a master key to access your private keys. And, if you lose or damage your hardware wallet, you can use the seed phrase to recover your keys on a new device.

Some basic rules:

Do not share your seed phrase with anyone

Do not store it online – this is not an email password that you put in a Google document or in a made-up contact in your address book! If anyone gets access to your seed phrase, they can steal your funds!

Do not type your seed phrase into anything other than your device, no matter who asks you to do so! If you keep everything safe, you will rarely need to use it at all.

Beware of emails from Trezor or Ledger saying there is a problem with your device and you need to follow a link, plug it in and enter your seed phrase to protect your funds! These emails are scams and will result in your wallet getting drained – no matter how real they may look, do not click anything!

I know this sounds a little scary, but welcome to taking responsibility for your own money! You also need to be careful accessing hardware provider websites, too – bookmark the link and access from there. These days, people tend to just Google ‘Trezor’ and click the top result – scammers work hard to get fake websites to the top of the rankings to catch people who do this. (This goes for any website, but especially where there is money or your private data at risk)

You should write your seed phrase down and store it somewhere safe. There are numerous devices available that are more sturdy than a piece of paper. I have had my wife walk in on me as I am punching a seed phrase into a metal plate – that wasn’t a simple conversation, but it was easier than explaining that the keys to my crypto ended up in the bin by accident…

Consult the experts

I am probably relatively crypto security savvy. But I am by no means an expert. I highly recommend that you consult the experts if you are going to self-custody your coins. Fortunately, I have just the guy for you!

Jameson Lopp has put together a trove of useful Bitcoin information on his website. He has tested and written up most of the Bitcoin wallets there are and published the information here: Recommended Bitcoin Wallets

He has also tested most of the seed backup devices – to destruction in some cases! His basic conclusion is that the more bells and whistles a backup device has, the more chances you have to mess it up. It’s hard to beat the simplicity of punching the phrase into a piece of metal!

Lopp is Co-founder & Chief Security Officer of Casa Hodl, which offers a range of solutions to help people store their Bitcoin more effectively. I’m not going to try to explain multisig here, but in a nutshell, it is a level of security which requires more than one user to approve a transaction using private keys. As the numbers get bigger, paying for better security begins to make sense.

Anyway, I’m not here to sell Casa’s services; I’m saying that Jameson Lopp has already done most of the research for you and generously published it on his website so you can learn. Check out his site and follow him on X @lopp

My two cents

As you have probably realised, some people possess far greater knowledge on storing Bitcoin and crypto than I do. However, if you want to know how I organise it, I can tell you.

Like with investments, I take a diversified approach. I think it’s important to learn how to take responsibility and self-custody, so I do that. However, I also live in a wooden house in an earthquake-prone country, and I am not entirely confident in looking after all of my Bitcoin. So, I also use Xapo Bank for third-party custody. I have written about them here: Banking your Bitcoin

If you ever decide to open an account with Xapo Bank, please use my referral code (SMM-XAT-EJG) or the referral link in that post. I have an ‘influencer’ deal with them, and I am surely the worst influencer they have ever had!!! It would be nice to actually help them get a customer now and then, and it won’t cost you any more than it would if you went directly to them. I am very comfortable recommending them.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I keep seeing posts declaring the 60/40 portfolio dead. No sh*t, Sherlock! Markowitz’s Modern Portfolio Theory dates back to 1952. I learned that 60/40 was no longer relevant in 2005. Where the hell have you been?

In case you are not familiar with it, the 60/40 refers to the traditional portfolio strategy that allocates 60% to stocks and 40% to bonds. The stock part aims for long-term growth while the bonds smooth out the volatility in rough periods.

Markowitz advanced this idea by blending a range of assets to produce a more efficient portfolio, recognising that the typical investor wants reasonable returns without excessive risk. See my post on Asset Allocation for more on this.

Can’t I just long equities?

Yes, it’s perfectly acceptable to just average into one or two stock ETFs and hold them for the long term, especially if you’re young. In fact, you can do that and read no further – you don’t need any help!

However, if you believe in passive investing and market indexing, which many people do these days, you must understand that the market encompasses more than just stocks.

Also, if you are investing a significant amount of money, it’s unwise to be 100% invested in one asset class, unless you have specific knowledge and overwhelming conviction. (which, by definition, a passive investor does not)

What’s a lot of money then? Great question! It’s different for everyone, but let me put it this way: If you are a passive investor, 100% in stocks, and you are starting to get concerned about the damage a market crash could do to your net worth, you might be getting close!

The funny thing about the 60/40 idea is that young people these days are probably already allocated 60/40, but to tech stocks and crypto!

Yeah, crypto, so where does that fit in?

This question is doing the rounds. If crypto is a new asset class, then where does it fit in a diversified portfolio? How big should the allocation be?

— The Wolf Of All Streets (@scottmelker) July 1, 2025

We can argue all day about whether the allocation should be closer to 10% or 40%. It clearly depends on an individual’s situation, risk profile, level of conviction, etc. The notable thing about this article is how it mixes up the whole Bitcoin vs. crypto terminology.

It mentions Bitcoin to start, but then it refers to crypto. So you should be putting 10-40% of your portfolio in what exactly? Bitcoin ETFs? Cryptocurrencies? Which ones? It’s not very clear.

I mean, they’re all the same thing, right?

Not even close! And ETH is the second-largest digital asset. Think how many coins have gone to zero since 2017! In my opinion, if you’re going to allocate part of your portfolio to this asset class, you need to get smart about it.

Here’s a pretty solid definition:

I’m not saying you can’t have mad conviction on a particular coin and hold it as an investment. If you have that level of certainty, then go for it. Hardcore XRP hodlers don’t care what I think, and they shouldn’t. They believe in the coin. But should the average investor put 10% of their net worth into it? Of course not!

The mainstream media are leading lambs to the slaughter if they can’t get their terminology straight.

Here’s the only truly investable cryptoasset in my humble opinion. Doesn’t it look beautiful?

Uncorrelated assets for the win

The modern portfolio enhances 60/40 by adding assets that are uncorrelated or only lightly correlated to stocks and bonds. That’s how you achieve better risk-adjusted returns. (similar or better returns with less risk) Back in 2005, I never imagined a shiny new, uncorrelated asset would emerge. It really is a remarkable thing.

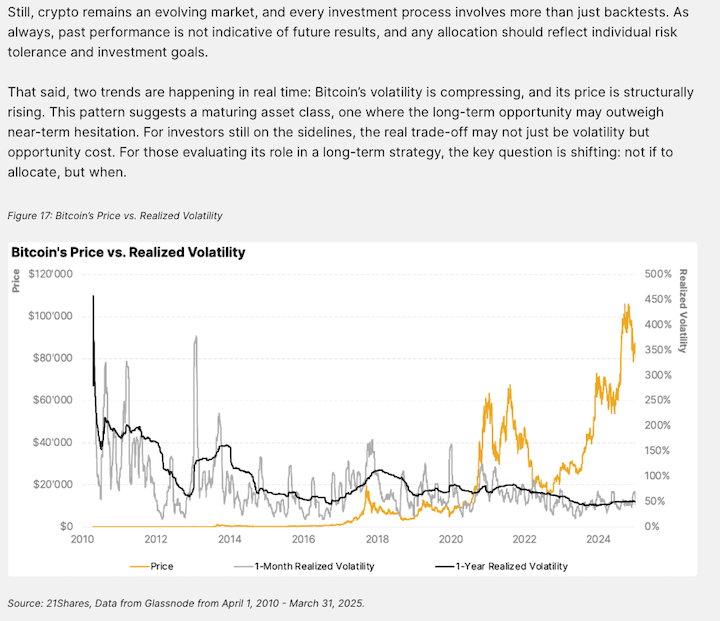

Here’s a quick summary: between April 2022 and March 2025, Bitcoin’s correlation to the rest of the asset universe was 36%. People like to compare Bitcoin to tech stocks, but its correlation to them was only 40%. These levels are significantly lower than traditional assets’ correlation to each other, which typically comes in at around 60-70%. This makes Bitcoin an ideal asset to add to a diversified portfolio in order to beef up returns without meaningfully increasing risk.

What makes Bitcoin especially interesting is how sometimes it behaves like a risk asset, like equities, and other times, it acts as a defensive asset, like gold. Over time, it is expected to become more of a gold-like store of value asset.

“This makes Bitcoin unlike any other asset in the market. It is structurally independent, behaviorally adaptive, and still offers significant asymmetric upside relative to legacy safe-haven assets. For portfolio construction, Bitcoin stands out as both a potential long-term hedge, and a high-impact diversifier at present.”

Adding a 1% allocation to Bitcoin to a modern portfolio over the 3 years resulted in stronger risk-adjusted returns. (It improved both cumulative returns and shape ratios)

Adding Bitcoin did not increase downside risk.

When scaling up to a 5% Bitcoin allocation, the risk-adjusted returns were even stronger, and the volatility remained manageable. Interestingly, they also tried a 3% allocation to the top 5 cryptoassets and achieved a similar uplift in performance without greatly increasing the risk.

So what’s the conclusion to be drawn here? You don’t have to go 40% into Bitcoin! Just a modest allocation increases portfolio efficiency without meaningfully increasing risk.

What are we trying to do again?

The whole point of investing is to beat inflation in your base currency. Doing it most efficiently with the least amount of risk is just being smart.

You can be overweight certain satellite holdings if you have a high level of conviction in them.

I still run a boring diversified portfolio, despite currently exceeding the recommended daily dosage of Bitcoin and Japanese stocks.

What’s my level of certainty?

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.