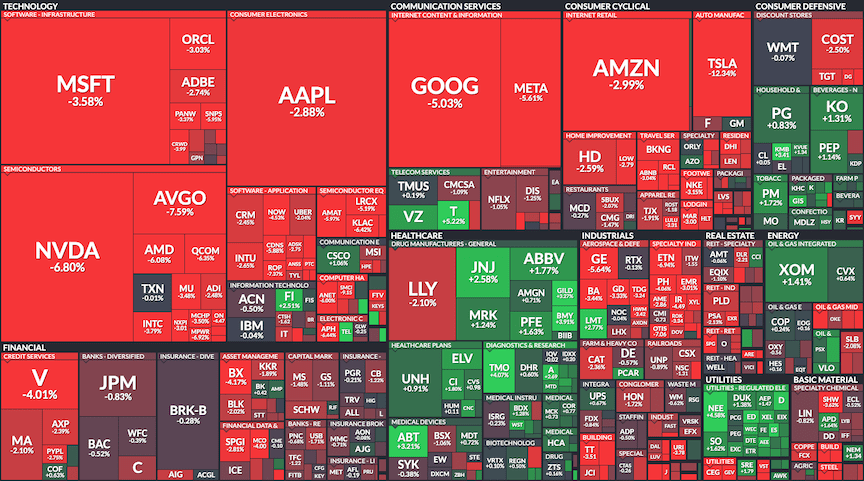

After showing signs of wobbling the last few weeks, US markets slumped on 24 July with big tech shares leading the move down. Tesla Inc (TSLA) fell -12.3% after a Q2 earnings miss while Alphabet Inc (GOOGL) dropped -5% despite beating earnings expectations. That was enough to trigger an avalanche and the NASDAQ ended -3.6% lower and the S&P 500 endured its worst day since 15 December 2022, falling -2.2%.

Correction territory

Japanese shares followed the US market down, with the Nikkei 225 index falling -3.3% today as exporters laboured under a strengthening yen. The benchmark index peaked on 11 July at ¥42,426 and has trended downwards since then. It turns out that I wasn’t imagining things when I asked Are we shaking? at the end of June.

Investors will now be wondering if this is simply a healthy correction after a big run-up or the start of a larger move downwards. It is too early to begin talking about a bear market but we are certainly in correction territory. A correction is defined as a fall of -10% from a recent high and the Nikkei closed today down -10.7% from the 11 July peak.

At 3pm today, USD/JPY was trading at ¥152.7. The current rebound in the yen is being driven by expectations that the Bank of Japan will raise rates at its policy meeting next week. In addition, the US Federal Reserve appears to be moving in the direction of rate cuts starting in September. A sustained sell-off in stocks may well need confirmation of rate cuts in order to stabilise.

Semiconductor stocks fall hard, Lawson delisted

Semiconductor-related stocks are bearing the brunt of the current selloff with Disco Corporation (6146) falling for seven straight days. Disco fell a further -4% today to close at ¥46,850, well off its peak of ¥68,850 set on 11 July.

In other news, convenience store operator Lawson Inc. was delisted from the TSE on 24 July following a successful tender offer from KDDI Corp. KDDI will partner with Lawson’s parent company, Mitsubishi Corp to take the company private.

A stock to watch

Crypto followed the trend in traditional markets with Bitcoin falling to around the $64,200 mark. Ethereum is down around -8% despite the successful launch of the Ethereum ETFs in the US on 23 July.

Meanwhile, Japanese Bitcoin proxy Metaplanet Inc. (3350) has been on a wild ride. The stock has risen more than +1,100% since the company announced its Bitcoin treasury strategy in early April. However, the FOMO really kicked in this week with shares accelerating to ¥300 on 24 July. Metaplanet is back trading around ¥220 today but is still a stock to watch as investors try to front-run the potential decisive break of Bitcoin’s all-time high in the coming months.

It seems likely that traders view Metaplanet as a tax-efficient way to gain exposure to Bitcoin price moves. Crypto in Japan is taxed as miscellaneous income, whereas stocks are taxed as capital gains.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s been almost 8 months since my Bitcoin bull market prep post Bitcoin – Pump up the Volume. It feels like it’s time to check in and see how things are going. I don’t know how accurate Rekt Capital’s estimation of progress will turn out to be but it feels about right. When I talk to people about Bitcoin, which I probably do far too much, I’m still stunned to find how little the halving cycle is understood. Nobody is interested in buying in the bear phase, but when the price starts going up and making news, people start asking if they should be getting involved.

For those of us who bought in the bear market, this is supposed to be the fun part. However, the timeline has been strangely depressed. I think a lot of people got sucked into alts and memecoins when they were rallying earlier this year and are stuck there. This is why I tell beginners to focus on Bitcoin. As volatile as it may appear to outsiders, it is actually quite predictable. So, what’s going on at the moment?

ETFs

The spot Bitcoin ETFs that launched in the US in January have been wildly successful. Blackrock’s IBIT took just 137 days to reach $20 billion in assets. The fastest before that took 985 days. The ‘sell the news’ traders did not come out of this well. The five US spot ETFs are at around $56.5 billion in assets. There is nothing complicated here – increased demand for a finite asset is going to have an effect on price and year-to-date the leading crypto asset is up a little over +50%.

What’s more, Blackrock CEO Larry Fink, previously a crypto sceptic, is regularly on TV talking about his belief that Bitcoin is a legitimate financial instrument which has a role in portfolios. Note the repost from Michael Dell:

Larry might be talking his own book, but he has actually grasped another thing that the majority of people are missing: that rather than a get-rich-quick scheme, Bitcoin is actually a defensive asset that can protect against currency debasement and other economic ills.

I’ll say that again: Bitcoin is a defensive asset. Let’s be real here, it’s not going to replace fiat currency as the base layer of the financial system. Governments have far too much invested in the status quo to let it go. And they are going to continue recklessly printing fiat money and inflating their debt. That money is going to go down in value against hard assets over time. Read Harden up your assets for more on that.

Guess who else seems to have just changed their opinion on Bitcoin?

You think Dimon flipped and doesn’t own any? Dips are for buying in the bull market folks.

Ever the opportunist, Donald Trump has seized on the Democrat’s hostility towards crypto and is speaking at a Bitcoin conference in Nashville later this month. I like the orange coin much more than I like the orange man but a Trump victory in November would likely be a full-bull mania catalyst.

Who are your bets on for Prez these days?

Never mind the parabolics, it’s the banana zone!

Maybe this cycle will be different. Nothing is certain in life. We could be wrong here after all. But if we’re not, the next phase of the bull market is banana-shaped. Raoul Pal is a bit excited:

Ahhhh, liquidity

Summer in Japan officially starts now. It’s going to be a hot one and there will be much call for regular liquid refreshment. And, what comes after summer?

That’s right, rate cuts in the US!

Jerome Powell is now pretty openly signalling that he intends to begin cutting this year, possibly as soon as September. The market believes him too. The biggest investing lesson I learned in the last few years is that liquidity drives markets. Liquidity is coming back and Bitcoin is thirsty. Don’t get me wrong, stocks love liquidity too but Bitcoin slurps it up with the highest intensity of all.

I don’t know if I’m as bullish as Raoul, but I’m not far off.

So, to sum up, we’ve got an asset that has been through three consecutive 4-year bull/bear cycles and is potentially 40% of the way through the current bull phase. We’ve got a bullet-dodging potential US President speaking at a Bitcoin conference. We have the kings of fiat finance changing their tune. And JPow is about to cut rates.

Am I forgetting anything? Oh, yeah. Ethereum ETFs look set to go live next week!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

The all-time highs keep coming. On Monday 9 July, the Nikkei 225 index made its highest ever close at ¥41,580.17. Semiconductor-related stocks led the way, while other notable movers included Hitachi Ltd (6501) and Fujikura Ltd (5803).

Not to be outdone, the S&P 500 and NASDAQ Composite also closed at record highs on 9 July. Gains were heavily weighted to big tech stocks as the AI narrative continues to drive market sentiment. Fed Chair Jerome Powell stuck to the script during his first day of testimony, reiterating that the Fed’s objective is to cool the economy and progress towards the 2% inflation target without cooling it too much. Market consensus continues to favour a soft landing scenario, with one or two rate cuts expected later this year. CPI data is due on Thursday and if that comes in line with expectations, the positive mood should continue.

Meanwhile, Tesla Inc (TSLA) continued its rebound, closing higher for the 10th consecutive day.

Japan’s real wages fall again, BOJ discussing cuts in bond purchases

Despite the good times in the stock market, much of Japan’s economy still looks relatively weak. Real wages fell by 1.4% in May, marking a record 26th month in decline. Wages are actually rising at the fastest pace in 31 years, but the increases are being offset by inflation, meaning households have less purchasing power.

USD/JPY is trading around ¥161.47 with no end to yen weakness in sight.

This week sees the Bank of Japan meeting with major market players to discuss the tapering of the central bank’s bond purchases. Some market participants are calling on the BOJ to cut bond purchases in half while others favour a more gradual reduction. The final plan is expected to be revealed at the BOJ’s end-of-July meeting.

Semiconductor shares remain strong, Hitachi and Fujikura impress

Chip stocks are once more powering ahead with Advantest Corp (6857) and Tokyo Electron Ltd (8035) gaining +4.1% and +3.8% respectively on 9 July. Chip materials maker Resonac Holdings Corp (4004) announced that it will form a consortium with nine other Japanese and US firms to collaborate on the development of semiconductor technologies for generative AI. Resonac shares surged +8.7% on the news.

Hitachi shares jumped +5.2% on reports that the company is increasingly focused on improving shareholder returns. On 2 July, the electronics giant provided an update on the progress of its buyback of up to 21 million shares at a cost of up to ¥200 billion. The company is targeting a total return ratio of around 50%, including dividends and buybacks – that would be on an expected net profit of 600 billion this fiscal year. Hitachi shares are up +89% year-to-date.

Another big mover was Fujikura Ltd, which jumped +11.4% on 9 July. Fujikura is an electrical equipment manufacturer that develops a range of telecommunication system products, including devices for optical fibres. It appears that Fujikura’s surge was spurred by a 12% move by Corning Inc (GLW) on 8 July after the company revised its sales forecast upward. Fujikura gained a little more today and is now up +228% in 2024.

Japanese stocks rose again today with the Nikkei 225 closing at another record high of ¥41,831.99. Financial stocks were up again on hopes that higher interest rates would bring improved profits. Mitsubishi UFJ Financial Group (8306) has gained over +8% in the past month and almost +50% year-to-date.

Bitcoin also bounced back from its current correction somewhat, moving from around $57,000 to $59,000 despite an increase in market supply from Mt Gox and the German government. Bitcoin ETF flows were positive again and traders eagerly await the SEC decision on Ethereum ETFs.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Being a financial planner by trade, I try to organise our financial future as efficiently as possible without going overboard. My wife and I both work and we have a reasonable income. We have a plan, we know what our numbers are for later in life and the big events in between. Most of all, we are flexible in that plan – our core investments are set and forget, but they can be adjusted easily. The tactical stuff is fun for me and I see it as a bit of a challenge.

Of course, things can go wrong: ill health, accidents, economic change and shifts in specific industries. You prepare for these as best you can and get on with living. Eat well, exercise, look both ways crossing the street, buy insurance etc. etc.

However, there are a few bigger things that bother me. I don’t think about them all the time, but they lurk in the back of my mind. For example, I don’t think AI is going to take over my job, but it could change the world considerably – gotta keep up with developments there. I could classify these things as outliers and conspiracies. Some may or may not have a meaningful impact and others feel a little ‘out there’. The best conspiracy theories have an element of truth, though, don’t they?

So, here are a few things I think about and how they relate to money, investing and how big your number should be:

Climate

I must confess, I don’t allow myself to dwell on what we are doing to the planet. We are clearly having an adverse impact and most of the damage is being done by big business interests who will not stop. The paper straws are cute, but they are hardly going to offset the widespread burning of fossil fuels and other environmental destruction. It’s not that I don’t think it’s important – it’s crucial to our survival as a species. I just know there isn’t much I can do about it. I separate our garbage, cut down on plastic and try not to waste resources, but I’m not losing sleep. Half the people in the developed world don’t even believe climate change exists so good luck to us coming together and taking action as a species. Do you remember the Covid mask and vaccine debates?

It is certainly getting hotter though! And it’s hotter for longer than it was before. After 27 years in Japan, it’s noticeable how spring and autumn are shrinking while summer gets longer year by year. What’s that going to be like in 10 years? How about 20?

I hardly think Yokohama will become unlivable in our lifetime but it could become pretty unpleasant. Imagine Japanese summer from April to October! Would that change your planning? Could it mean your ‘number’ needs to be bigger? The ability to escape Kanto, and maybe even Japan, for several months a year could become a key lifestyle choice. Maybe some people will want to escape for good. Wouldn’t that mean that the cooler, more livable climates in the world are going to see an influx of people who can afford to move? Parts of India are already hitting 50°C as a matter of course. That kind of temperature is more manageable in the developed world with aircon but doesn’t higher demand for a cool place mean higher prices?

As we move from climate change to climate crisis, how are governments going to address it? Again, remember Covid? It was all the people’s fault that it was spreading. They had to be stopped from travelling and confined to their homes in some countries.

Climate lockdowns anyone? Do you think they won’t do it?

It’s a dark thought, but people with flexibility financially will fare better than those who are struggling for money. Does that change your number?

Japan’s economic decline

Honestly, this one would bother me more if I was younger. I’m not sure Japan is a place I would be trying to build a life, career or business given the demographics and the economic outlook if I was in my twenties. But I’m not that young any more and I’m happy where I am. I would, however, want my kids to have the opportunity to live and work overseas if they choose.

The yen is a major concern though. My view is that short term it should recover somewhat when America begins cutting rates. I can see it getting to ¥130 or even ¥120 in the next year or so. However, longer term I expect the yen to steadily lose ground, particularly against the dollar. I talked about it in my ‘How screwed is the yen?’ post a year and a half ago. Staying alert for opportunities to earn in other currencies, investing in a combination of domestic and overseas assets and accumulating Bitcoin remain priorities for me.

Financial shenanigans

Grab your tinfoil hats for this one! In simple terms, the money has been funny since the 2008 global financial crisis. A lot of institutions that should have died were propped up at the expense of taxpayers and we’ve been getting screwed ever since. Economies and big business have become addicted to liquidity: cheap money, low rates. Low interest rates foster inflation, which is a tax on us all, but especially a tax on people who do not own financial assets.

Countries have too much debt and are not producing enough to pay it back. Japan is perhaps the worst offender, at least in the developed world. The debt spiral is probably terminal. That’s why the yen is doomed, and after that so are the pound, the euro and the dollar. I covered currency debasement in ‘Harden up your assets.’ There are tools to fight it that need to be deployed. Otherwise, your money buys less and less.

This is why governments are getting interested in the idea of Central Bank Digital Currencies. (CBDCs) At some point, they are going to need to perform a reset and substitute the current failing money with an alternative. And the powers that be never want to waste an opportunity to seize more control.

In essence, CBDCs are just another form of fiat money. But they come with a whole new opportunity for manipulation. Here’s an interesting video of Rishi Sunak being asked how he would enforce national service in the UK:

Controlling ‘access to finance’ is a government wet dream and CBDCs will make it easy. If you think that the possibility of losing permanent residence due to unpaid taxes is bad, wait until they freeze your bank account or apply a negative interest rate to your money until you pay up.

The public is sleepwalking into this one. You can already imagine how half the population won’t have any issue with it at all. ‘If you don’t have anything to hide, why would you need to keep your money private?’ will be the refrain. People who are well off have no concept of how less fortunate people can run into money trouble and fall behind on bills and taxes. The rich just don’t want to pay for a bunch of ‘layabouts and immigrants’.

The Bank of Japan already has a page on its website about Central Bank Digital Currency by the way. Cute, huh? No plans to implement it at present, but they are looking into it…

CBDC is one thing I think is really worth fighting against, but it will most likely be a losing battle. Sooner or later some crisis will come along and CBDC will have to be implemented ‘for our protection’. You can already see it happening with the AML/CFT mission creep.

Call me crazy, but I think that accumulating Bitcoin and other crypto is the best we can do to prepare for what is coming. Any money sitting in the fiat system will be caught in the net. In many countries, people who want to withdraw a few thousand dollars in cash already have to explain to the bank what they are planning to do with it.

Assuming the number will go up

So there it is. Like you didn’t have enough to worry about! From a financial planning perspective, my take on this is that whatever your number is, you will probably need more.

That’s to say, whatever amount of money you think will be enough to secure your future, maybe add another 10-20% for safety.

This is why I recommend dividing investments into core/strategic and satellite/tactical. The long-term strategic investments are focused on hitting the number. The tactical assets are aiming for a little extra. The crypto holdings are a shot at f**k you money.

Number go up. Act accordingly.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I spent the last year and a half writing financial content for a broker. I enjoyed the experience immensely and learned a lot in the process. Unfortunately, the contract ended, but I now have 10-12 hours a week that have been returned to me. So, readers of this blog may notice some extra market commentary/analysis being posted here. I hope it is useful.

It’s central bank week, with both the Federal Reserve (Fed) and the Bank of Japan (BOJ) conducting their policy meetings. As expected, the Fed held rates steady at 5.25-5.5% while CPI came in marginally cooler than expected. The Fed was surprisingly hawkish, forecasting just one rate cut in 2024.

Some think the BOJ may actually tighten at their meeting. If they do, it will likely be a minor adjustment. There will certainly be discussion about reducing the purchase of government bonds.

USD/JPY is currently trading close to the ¥157 level. With no major change in the US/Japan interest rate differential, we can expect the yen to remain weak for some time.

US markets hit all-time highs

In the US, the S&P 500 and the NASDAQ hit fresh all-time highs overnight. Apple Inc (AAPL) rose again after jumping +7.3% on 11 June when it unveiled a range of AI-enabled features and software for its devices. Apple overtook Microsoft Corporation (MSFT) to once more become the world’s most valuable company. Apple’s market cap now stands at a staggering $3.27 trillion.

Oracle Corporation (ORCL) surged +13.3% after the cloud technology company announced two new partnerships with OpenAI and Google Cloud while also forecasting strong revenue growth in fiscal 2025. Broadcom Inc (AVGO) jumped +14.6% after hours on strong earnings and a big stock split.

TDK and Hitachi set new highs since listing

Japanese stocks are largely in wait-and-see mode as the BOJ meeting kicks off today. TDK Corp (6762) has set another new high since listing as electronic parts stocks related to Apple are bought up. TDK announced in December that it will manufacture lithium-ion battery cells for iPhones in India.

Hitachi Ltd (6501) also hit a new high since listing of ¥17,340 on 11 June. On 7 June, its subsidiary, Hitachi Energy announced that it will invest $4.5 billion to increase production of power transmission and distribution equipment by 2027. Hitachi shares have cooled a little in the last couple of days, despite the announcement of plans to invest ¥300 billion in generative AI in fiscal 2025.

At lunchtime on 13 June the Nikkei 225 index is up slightly to ¥38,831.

Crypto stocks rise

Bitcoin, being the quickest asset to react to economic data and central bank policy, fell the day before the CPI data release and immediately bounced when the numbers came in soft. At the time of writing BTC is trading at around the $68,000 mark. Crypto stocks fared well with both Microstrategy Inc (MSTR) and Marathon Digital Holdings Inc (MARA) up overnight. Meanwhile, in Japan, Metaplanet Inc (3350) announced the purchase of an additional 23.35 Bitcoin on 11 June. The company now holds 141.07 Bitcoins, acquired at an average price of ¥10,278,391 per coin. Shares are up +494% since Metaplanet announced the adoption of Bitcoin as its core treasury asset on 8 April.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

If you have been following my posts on crypto, you probably have at least a general understanding of the Bitcoin halving-driven 4-year cycle. If you have really been paying attention to the space, you will have noticed that each bull market leg of the cycle is accompanied by a craze of some sort. I choose the word craze deliberately because, to the rational individual and long-term investor, these speculative frenzies appear exactly as such: crazy!

In 2016/2017, it was ICOs. In 2020/2021, it was NFTs. And in 2024/2025, the craze is for memecoins.

Initial coin offerings (ICOs) were crypto’s equivalent of an initial public offering (IPO). And projects seeking to raise money for their new blockchain, app or service launched them left and right during the 2016/2017 bull market. That period saw an explosion of ICOs. Ventures with absolutely no use case for a blockchain launched on the blockchain. New coins pumped and pumped and dumped. Scams abounded, fraud ran wild and fortunes were made and lost.

A few projects survived and thrived. Ethereum completed its token presale in 2014 and launched in 2016. Investors got rich and the protocol is still developing and innovating today. It was the introduction of the Ethereum ERC-20 token standard that kicked off the ICO boom. Launching an ERC-20 token was far easier than launching an independent blockchain. And launch they did, in their thousands. Notable survivors include AAVE, Filecoin and Chainlink. The majority of ICOs however, did not make it.

If ICOs were looked down on then NFTs were truly hated. Who would have thought all those monkey JPGs would end up being worthless??? The first mover, and arguably the coolest non-fungible tokens were Cryptopunks. A collection of 10,000 8-bit-style avatars, launched on Ethereum (aha!) by Larva Labs in 2017, punks were an experiment in the tokenization of assets. Each punk was different and could only be owned by one person at a time. Initially, they were given away but by 2022, some punks were selling for millions. Punk 5822 sold for a record $24 million (8,000 ETH) in February 2022.

Many imitators followed, and soon the market was awash in Bored Apes and Miladys. Just like ICOs, some collections survived but the eventual crash in prices was inevitable.

The hate for NFTs was most intense from photographers, artists and other creators. There was an undeniable scaminess to the space and the money was too easy. Digital art went crazy regardless, with some genuinely innovative artists emerging. In March 2021, Beeple sold an NFT of a digital collage of his work for $69 million. At Christie’s, no less! Beeple still produces an impressive output of bizarre, and often disturbing artwork – find him here.

NFTs originated on the Ethereum network, but the 2020/2021 cycle saw the emergence of a new player: Layer 1 blockchain Solana. Solana uses a proof-of-stake mechanism to provide smart contract functionality. For the uninitiated, that means you can build stuff on it. NFT platforms, decentralised exchanges and more. Solana and its native SOL token flourished during the last bull market and, more importantly, it survived the chaos that followed.

And then came the memes

Memecoins are by no means new. DOGE, widely credited as the original memecoin, was created as a joke back in 2013 with the image of a shiba inu dog named Kabosu as its logo. Doge may have been a joke coin but Kabosu was a real dog, owned by a kindergarten teacher from Sakura, Japan. Kabosu and her owner became surprise celebrities in their own right and there was genuine grief when Kabosu passed away in May 2024. (RIP)

Meme Stocks and ‘Dumb Money’

Meme-based investments are not limited to crypto. You may be familiar with Keith Gill, better known as Roaring Kitty, who sparked the craze in GameStop (GME) shares that literally took down hedge funds in a short squeeze in January 2021. If you haven’t seen the movie ‘Dumb Money’, I highly recommend it.

Roaring Kitty caused a commotion last month, suddenly returning to X with a barrage of memes and kicking off another run in GME that almost made him a billionaire just last week!

The craze of the current crypto bull run has clearly been memecoins. In particular, the frenzy has been driven by the relative ease of creating new memecoins on Solana. These coins are typically inspired by internet jokes, memes and satire. They are fun and crazy, not serious investments. And yet, some traders have run up impressive returns.

Dogs are as popular as ever. The Bonk Inu (BONK) memecoin was designed to support the Solana community. It launched on Xmas day 2022 when SOL was trading at around $11.40, down some 96% from its peak of $260. (yes, yikes!) BONK was airdropped to various NFT projects, artists and collectors. Almost 300,000 wallets were created to receive the airdrop and within a week of launch, the token had risen over 2,000%. Much volatility followed!

BONK doesn’t do anything. However, the Solana and BONK communities found ways to incorporate the token into various protocols, such as De-Fi, NFTs, gaming and payments. It can be used for direct exchange, to buy NFTs, as in-game tokens/rewards, and more. It currently has a market cap of around $1.9 billion.

Astonishingly, there are now some 967 Solana memecoins trading with a total market cap of around $9 billion! Celebrities are getting in on the act, with Caitlyn Jenner and Iggy Azaelea launching their own coins. You can smell the lawsuits already…

So what do you meme?

Smart traders will undoubtedly make money in memes. However, for most this isn’t going to end well. Personally, I don’t own or trade any of these coins and I am certainly not recommending you go 100x long on Dogwifhat coin. However, the latest craze is fun to watch while providing genuine insight into where we are in the bull market cycle. Here’s how it goes: money flows into Bitcoin and Bitcoin rises. (have you seen those ETF inflows?) Then traders rotate into the L1s and L2s and they pick up. Next, the money moves to the various altcoins from larger cap to small and lastly, there’s a memecoin frenzy. This repeats with increasing intensity as the bull run builds to a crescendo. If you are trying to time your way out of the market, the memecoins act as a useful indicator of froth and irrational exuberance.

At some point in the next 12-18 months we will see Bitcoin well above its previous cycle all-time-high of $69k – which is where it sits now, incidentally. Now it becomes important to pay attention to the rotation I mentioned above. Ethereum finally turns on the afterburners, Solana goes stratospheric, AI coins go supersonic. And finally, the memes blast off.

The meme mania is the exit sign, a glowing beacon. There is only one way out and not everyone is going to fit through the door at once. Your crypto holdings have outperformed every other asset class. You have been steadily taking profits and now it’s time to push the button one last time. You must not hesitate. Unfasten your seatbelt, stand up and walk calmly to the exit, before the crush.

Last one out, turn out the lights.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Once more, I find myself short of time to post here. However, it is not due to a lack of things going on in markets these days. So, here I am on a Friday afternoon with a little time to spare to share some observations. Let’s do it quick and dirty!

Macro

We seem to be at the mercy of central banks these days. The number of Fed watchers and Fed experts is growing exponentially, especially among those with high exposure to risk assets who are gasping for a rate cut! Inflation is coming down, but not as fast as Mr. Powell would like. (remember falling inflation still means prices are going up, just not as quickly as they were) You may notice how the US stock market pumps whenever Fed officials say anything vaguely dovish. It also jumps on any weak economic data. Bad news is good news – ie. if the economy is slowing, the Fed is more likely to cut rates and pump our stocks. Weak jobs report = market up. GDP lower than expected = market up. Whatever you think of the Fed’s performance, they have been abundantly clear that they are data dependent. If inflation comes down and/or the economy weakens significantly, cuts are more likely. My guess is not until late this year, maybe next year.

Despite all this, the US market is near all-time highs. Stocks sure do like to climb a wall of worry!

Of course, there is an election coming. Biden has rather brashly said on camera that he thinks rates will come down. Yes, the Fed is independent and not susceptible to political pressure, right? The last time Trump won, the market went up. And you can bet the orange one will be applying heavy pressure for rate cuts if he wins again.

Of course, worsening economic data puts recession firmly on the table. Stocks do not like the R-word. However, recession also means rate cuts and the mere whiff of them may be enough to reignite irrational exuberance across risk assets. It’s going to be interesting…

Japan

The Nikkei is trading over ¥38,000 with bond yields pushing 1% and the yen at ¥157 to the dollar. If you had predicted this a few years ago, nobody would have believed you! I keep seeing articles about ‘the sun rising on a new Japanese bull market’. I don’t know where these writers have been for the last 2 years… I keep getting tempted to take some profits but doing nothing has worked nicely so far. Still, you might want to make sure your seatbelt is securely fastened. Turbulence is no fun, as we learned in recent news about a UK to Singapore flight.

In theory, rate cuts in the US will reduce the interest rate differential between the US/Japan and the yen should strengthen. Again, I don’t think it will be until later this year at the earliest, and maybe well into next year, but there may be some relief for the yen in the near term. Long term looks dark though, ladies and gents. If you got stuck in yen but it’s not your base currency, I would take any chance you get to reverse that. The market doesn’t owe you anything.

Time to get long on electricity generators?

Remember when Bitcoin was boiling the oceans and drinking swimming pools full of water like tequila shots? Crypto is forgiven. There’s a new bad guy in town and ChatGPT is hungry for electricity and in dire need of a drink! I’m pressed for time so you can google yourself, but data centres for AI are consuming mucho power and they get hot while they do it – I literally saw an article this morning about some crazy number of swimming pools needed to cool everything down. If you think demand for power is going anywhere but up, I don’t know what to say to you.

While on the topic of AI, chip giant Nvidia nailed earnings yet again. And raised their guidance to suggest more next quarter. Absolute monster company. Semiconductors, AI, data centres: all going bonkers.

The stock is up +594% over the last 3 years. Expect volatility, sure, but it’s not slowing down yet…

Crypto bull market progress

The Bitcoin halving is behind us. We got a pretty good pullback to $56k from $70k and now we are back at $67k. We didn’t even get to the good part yet. I still think people are underestimating how crazy this cycle will get. Another thing to strap in for!

The Biden admin, spearheaded by Senator Karen (sorry, Warren) has been openly hostile towards the industry ever since Sam Bankman-Fried torched them. These guys could rival the EU in crushing innovation. But then a funny thing happened: Trump came out and said ‘If you like crypto, you better vote for me’. Then he started accepting donations in crypto. Suddenly the crypto vote is leaning heavily towards orange man. And what do you know? We got an Ethereum ETF. Believe me when I say, there was ZERO chance of an ETH ETF getting approved a few weeks ago.

ETH has underperformed this whole cycle. And judging by today’s weak ETF reaction, the PTSD is real. The Bitcoin ETFs blew away expectations in terms of inflows. Watch for ETH doing the same.

There are many ways to play the crypto bull. Metaplanet Inc, a Japanese company no one had ever heard of, (they do hotel development and some web3 stuff) announced on 8 April that they were adopting Bitcoin as their core treasury asset, a la Microstrategy. The stock went from ¥19 to ¥36 on the news. Now it’s at ¥57, having touched ¥120 on 23 May. They’ve got Mark Yusko on the board and Dylan LeClair as Director of Bitcoin strategy.

I’m not saying you should buy this stock. (Disclaimer below!) I’m saying you should put it on your watchlist and forget about it until Bitcoin breaks out past the previous cycle all-time high, goes parabolic and then you can kick yourself for not owning such an obvious play on the bull market. (insert wink emoji here)

Supply and demand

Being dumb but with a high appetite for risk if you can explain something to me in simple terms, I own a copper ETF. (1693) I was hearing for some time that the demand for copper is going to far outstrip supply, so I got some exposure. So far, so good. A lot of clever people are saying the move is overdone and we are going lower, but these are low-time frame traders and from what I can tell, the long-term supply/demand dynamics are unchanged. But what do I know? Regardless, we’re gonna need some popcorn over here, please.

A note here: we are talking about satellite holdings and my long term diversified portfolio is completely unchanged, moisturised, happy in its lane etc etc.

I’m out of time here but lastly, somebody helpfully reminded me that Ben at Retire Japan is offering a 50% discount if you pre-order his 2024 Guide to NISA. I don’t see how you can afford to miss that. Click here!

Until next time!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

With the weather warming up, I’m starting to get the itch to get back out on the golf course. I know people who don’t play the game struggle to see what is so interesting about golf, but I can tell you there is a lot more to it than just chasing a little white ball around the countryside. Golf may be a competitive sport professionally, and many amateurs like to put a bit of money on the line against their mates. However, anyone who has played the game knows that it’s never you against the other player. It’s all about the battle between you and the golf course. Or, more accurately, the battle between you and that space between your ears. If you focus on what the other guy is doing, you are always going to lose. Knowing who the real opponent is is the key to improvement.

The same can be said for investing. If you’re a trader, you are playing a zero-sum game. Every time you win, someone on the other side of the trade loses. However, it’s not like this for investors. It’s not a competition between you and other people. What everyone else is doing is irrelevant. You need to master yourself, and more importantly, you have to know what it is you are competing against.

People tend to think they are trying to beat the market but that is really not the case. The market just is. It doesn’t even know you exist. It’s the sum of all the information available driven by the impulse of human emotion. You cannot conquer this beast. The market just tells you the price of things, no matter how crazy it may seem.

Know your enemy

If you are going to be successful at investing, you better know what you are up against. What exactly is it you are trying to beat? Think about that for a minute. Why is it that you have to expend all this time and energy trying to run your own personal hedge fund? Why do you have to pay some ‘expert’ to guide you through this lifelong struggle? Why can’t you just put your money in the bank and get on with more important things?

The standard answer to these questions can be summed up in one word: inflation. But what does that mean? Well, here’s the definition: inflation is the rise in the cost of goods and services over time. It sounds almost innocent, doesn’t it? The price of things just goes up a little over time, so you should invest to keep pace with it. No big deal right? Any half-decent financial planner can help you put a plan in place to handle that.

The truth is a little more sinister. That 2-3% inflation number that governments and central banks report to you every month is heavily manipulated to begin with. But it doesn’t even come close to measuring the size of the monster that is actually eating up your spending power. The final boss, the thing you are really playing against is much more significant than a natural rise in the price of stuff over time.

What the hell is that you ask? Well, in the old days, when coins were made out of gold and silver, debasement was the act of mixing base metals with the precious metals, therefore reducing the amount of the ‘good stuff’ in money. By using less gold and silver in the coins, the issuer lowered the value of the currency.

These days, debasement takes place when a government prints money, increasing the money supply without a corresponding increase in output. Debasement gifts more money to governments for spending and bailing out their banker friends, and the result for citizens is inflation.

Can you think of a country where that may be happening?

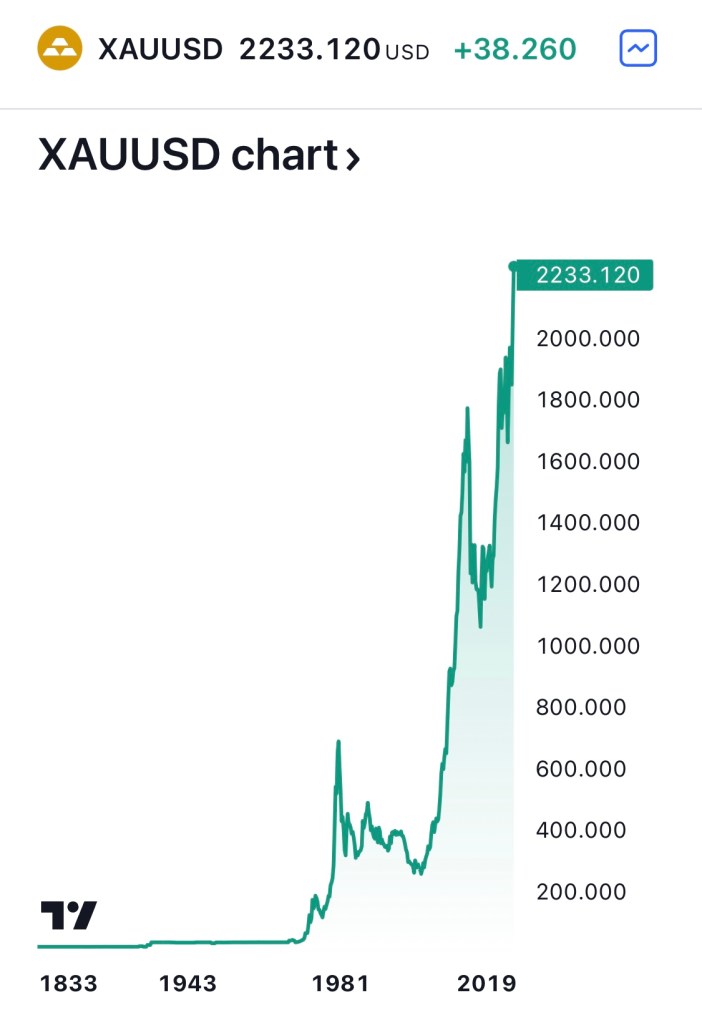

Gold was long considered money, and still is by many people. A good way to judge if your currency is being debased is to take a look at how it is performing against gold.

Gold vs JPY

Hmmmm, maybe printing all that money in order to escape deflation has more than achieved the expected result…

And before we rag too hard on the Bank of Japan, here’s the US dollar. And yes, the chart goes back to 1832 – can you spot where the currency came off the gold standard?

Gold vs USD

If that doesn’t make you mad, I don’t know what will. It certainly answers the question of why we have to spend so much time learning to invest.

You are probably understanding that investing is not a choice here. If you don’t learn how to do it, your spending power is toast. Do you think these governments are going to stop?

If anything, debasement is picking up the pace. The world’s economies took on too much debt and are not producing nearly enough to pay it back. The only way out of this hole is to inflate the currency which means that you and me get screwed.

Oh, and if you want to see what monetary debasement looks like when combined with climate change, take a look at cocoa these days:

Cocoa vs USD

Better stock up on Easter eggs folks!

Yes, all Fiat currency

I know I said let’s not rag on Japan, but let’s rag on Japan, shall we? Finance Minister Suzuki has been out every day this week expressing his ‘concern’ over ‘excessive’ moves in the currency. After printing to infinity, he even had the nerve to blame the weakness in the yen on, wait for it, ‘speculators’!

It’s straight-up gaslighting and I’m ‘speculating’ that with debt to GDP at 263%, they are going to continue to incinerate the yen. Don’t get me wrong, this isn’t Turkey – the liras of this world are on their death bed and there isn’t long left to say your goodbyes. Japan has a highly developed and productive economy so the currency isn’t going to implode tomorrow, but have no doubt, it is going to die a slow and painful death and that pain will be felt by you if you don’t protect yourself.

The US dollar is the global reserve currency. This doesn’t free the US from the endgame of its own excessive money printing. It just means it will be the last man standing. All currencies will go down against the dollar. The dollar will go down after the demise of everything else.

No double bogeys!

Back to the golf analogy – I don’t know who said it but there’s a quote that goes something like: ‘A bogey is one bad shot. A double bogey is one bad shot followed by a stupid shot.’

If getting yourself into a position where you have money in yen that you one day want to spend in another currency was your mistake, it’s time to make sure your next shot isn’t a stupid one.

Even if you are planning to stay in Japan and spend your yen here, sitting in cash will devour your spending power. So how do you fight currency debasement? You have to own assets. Assets, like food and other goods, are ‘stuff’. A currency that is being debased goes down against stuff. The Nikkei 225 is not at ¥40,000 by accident. The denominator is going down against shares in companies. Japan’s average land prices rose by 2.3% last year. The denominator is going down against land. I look at my stocks app and a Japanese gold ETF is up over 3% today. It seems like people are getting the message. (great thread about that from Weston Nakamura here)

Harden up your assets

If you’ve been reading my blog for a while, you will be familiar with how I like to structure investments: a ‘core’ diversified portfolio that holds a broad range of assets combined with ‘satellite’ holdings of tactical assets that fit current market conditions. The satellite holdings you want to beef up in order to stave off currency debasement are ‘hard assets’. By this, we mean tangible assets or assets that have a fundamental value. Real estate is a good example. Commodities, especially gold, are another.

You don’t have to buy houses, office buildings and bars of gold to achieve this. You can own Real Estate Investment Trusts (REITs) for a small amount of money. You can own a gold ETF. Is the real thing better? Sure, but we don’t have to be purists about it. The currency is going down against gold ETFs – problem solved.

You’re going to talk about Bitcoin again, aren’t you?

Nah, I’ll just post a chart.

Rock hard supply-capped digital asset vs currency debasement

Happy Easter everyone!

Put this blog post in a tweet

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I made an appearance on Retire Japan TV on 22 January. It was a delightful conversation and many thanks to Ben and Daniel for having me on. In particular, much respect to Ben for tackling the subject of crypto, which he is by no means a believer in! I don’t think I convinced him, but hopefully, I somewhat demystified the idea of crypto, and Bitcoin in particular, as an investment asset.

I have spent the last 6 years learning about and experiencing crypto. Whenever I talk to people who have not been paying much attention, I have to remind myself that they have many misconceptions that I dispelled long ago. Watching the video back, I inevitably found a few parts that I could have explained better, but I think I covered the main points I wanted to hit:

Bitcoin not crypto – I can’t really stress this enough. If you are new to the asset class and you don’t yet have a basic understanding of Bitcoin and its four-year halving cycle, you should not be diving into altcoins. You will get rekt, which is a technical term by the way! The Bitcoin four-year cycle drives all of the price action in crypto. Get a little Bitcoin first, learn about it, and then explore other crypto assets if you are comfortable.

Go forth and diversify! – we touched on Harry Markowitz and efficient frontiers. I have covered this in a post on Asset Allocation. I also wrote a post back in 2018 on Diversifying Through Crypto. With Bitcoin, we are talking about an asset that is only moderately correlated to traditional asset classes. Non-correlation is the name of the game if you are looking for better returns without significantly increasing risk. If you only own stocks, you are not diversified. If you own stocks plus Bitcoin, now you are a little more diversified. Really you need to own a little of every asset class. Diversification becomes more and more important as the amount of capital you have growsbigger, and also as you get closer to spending it. Most people are not diversified enough. Read Ray Dalio, folks!

You are being robbed! – we are not just talking about a little bit of healthy, organic inflation here. Central banks have been printing money and inflating their balance sheets knowing that in the end, it’s the public who will pay for it. When the system makes money, it’s capitalism. And when the system creates a big hole, it’s time for some socialism. The next book on my reading list is Broken Money by Lyn Alden. Ben made the point that other investment assets like stocks and real estate offer protection against inflation, and they absolutely do, but good luck exchanging a fraction of your house to buy goods and services. The difference here is that Bitcoin is a form of money and it is programmed to be deflationary. In my opinion, it will outperform the debasement of Fiat money over time better than stocks or property.

Basic economics – I took a few economics classes back in university. I wish I had been more interested at the time. The first thing that was covered was supply and demand. It is fundamental. Fixed supply with increasing demand = number go up! Jurrien Timmer at Fidelity is an essential follow for understanding the properties of Bitcoin and how it relates to other asset classes. Read up on Metclafe’s Law and network effects. We are talking about a network here.

Misconceptions

There are too many misconceptions about Bitcoin to count. The biggest one is that someone could just make another one. Folks, we’re talking about an asset with a $785 billion market cap. Good luck making a new one that’s going to knock it off its perch. Nobody in crypto is trying to do that. The race for the underlying store of value in the space is over.

That doesn’t mean all the other coins are not investable. Some are better than others and they are simply built to do different things. But that’s a whole new essay that I don’t have time for here.

As for the idea that only a handful of people own most of the Bitcoin. That was a new one on me but it’s simply not true. There’s a great report on that by Grayscale here. Also, if you are looking to figure out what’s going on in the network, Glassnode is an amazing tool. Check out their 2023 Yearly On-chain Review.

I could go on, there are so many misconceptions. Hell, China has banned Bitcoin multiple times. So no one in China owns BTC right?

Integration into traditionalfinance

The rallying call of crypto folk used to be ‘We’re still early!’. Judging by how little the average person understands the asset class, I think that’s still true, but it is getting less so. A few years ago, Larry Fink, the CEO of Blackrock, was decrying crypto as a tool only used by criminals to launder money and finance terrorism. It’s a familiar refrain from those who feel threatened by the emergence of a system that competes with the one that made them rich. (We see you too, Jamie Dimon) Now Larry has a spot Bitcoin ETF and is on Bloomberg and CNN saying that all financial assets will end up tokenised on the blockchain. Stocks, bonds, the whole shebang. We’re not so early any more.

Of course, a Bitcoin ETF is a tradfi product. You can’t exit it in Bitcoin, only in dollars. But for Japan residents, that does mean it gets taxed as capital gains, not income.

Other resources

The first time I looked at Bitcoin was in early 2017. My friend came back from a conference and said “We need to buy Bitcoin!” and handed me a report called ‘How to position for the rally in Bitcoin’, which was actually published in 2015 by Adamant Research. I read that and thought he was probably right. Adamant is still publishing analysis and their latest report is called ‘How to position for the Bitcoin boom’. You can find all their analysis here.

I mentioned Microstrategy on Retire Japan TV. Their Bitcoin dashboard is quite something and can be used to compare Bitcoin returns to other assets.

So there you have it. Not content with being allowed to talk for an hour, I have now written a post to further clarify my thoughts.

The halving is in April. I would expect a couple of months of sideways chop in crypto prices, maybe even a big juicy drawdown. That’s all part of the ride. Check in on me in 12-18 months!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Happy New Year everybody! I hope you all enjoyed a peaceful winter holiday and are back, raring to go and make big things happen.

For some reason, I had a feeling that this was going to be a challenging year and it didn’t really get off to the best start in Japan. For those interested, I was googling around yesterday trying to figure out the best way to donate to disaster relief on the Noto Peninsula. I found this page run by Ishikawa Prefecture. You can download a form here to request a receipt for your donation for tax purposes. Donations qualify for the donation deduction and there is a useful FAQ on the tax treatment of donations here.

So yeah, earthquakes, runway collisions, fires and we’re only a third of the way through January!

From a personal finance and investing perspective, there is some exciting stuff going on though. The New NISA has launched. I logged into my SBI account and it was pretty simple to get started. I have already set up the ‘tsumitate’ allocation and started buying some stocks for the ‘growth’ allocation. Clearly, everyone else is doing the same thing as the Nikkei is pumping so far this year!

I posted a couple of interesting takes on Japan on ‘X’ yesterday: an optimistic look at the year ahead from Jesper Koll and a much darker look at the demographic issues facing Japan from author Nire Shūhei. It always pays to look at both sides.

So how to invest in the year ahead? If you have been reading this blog over time, you will know that I divide investments up into core and satellite allocations. The core is a diversified portfolio weighted heavily to your base currency that just gets rebalanced once a year. This would typically account for around 70-80% of your investments and the idea is to keep adding to it as much as you can. If it’s a bit dull and boring, you are probably doing it right!

The other 20-30% can be allocated to satellite holdings, which may be a little more racy and exhibit a higher risk-return profile. If this part isn’t fun, then you are probably doing it wrong!

Satellite holdings will change over time depending on the economic environment we are in. So how are things looking?

Some thoughts

On the one hand, things look pretty much like they did for most of last year. The Fed funds rate is 5.5%. People who are obviously long risk assets have been trumpeting the start of rate cuts as early as March, but Mr Powell doesn’t look like he’s in much of a hurry to me. Although the Bank of Japan has adjusted its yield curve control policy and allowed long-term interest rates to rise a little, it is still continuing with its negative interest rate policy. There has been a significant amount of speculation, from both within and outside Japan, about when the BOJ will ‘normalise’ rates – I do love this term, like there is a way to return to normal with government debt to GDP at 264%! Gulp…

Despite noises being made about an exit from negative rate policy, it’s notable how quickly these ideas get put on the shelf. Comments I have heard recently include: ‘The earthquake will make it harder to normalise rates’. Probably true, but any excuse to avoid the inevitable. The Labour Ministry’s November report showed that real wages have declined for the past 20 months in a row, so there’s no sign of the mystical ‘virtuous cycle’ of wages outpacing price rises that would signal a move from the central bank.

It’s not going to happen, is it?

So if you’re waiting for the yen to get back to something sensible against the US dollar, good luck! Markets can remain irrational longer than you can remain solvent enough to go on a nice holiday abroad…

Japanese stocks, for the most part, are loving the weak yen. Any company with significant exports and profits abroad will see those profits magnified when converted back to yen. If you’re wondering why your Toyota shares are doing so well, there you are.

What kind of market is this?

Some time ago, I read the book Reminisces of a Stock Operator by Edwin Lefèvre. It’s considered somewhat of a bible by many investors. While there are some interesting tales of hi-jinks and high leverage, there was only really one key thing I got out of the book, but that one thing has stuck with me: Traders and investors should always know if we are in a bull market or a bear market.

It’s always the simple things that have the most impact, right? The protagonist in the book is a stock trader and his big-picture strategy is very simple: If he is in a bull market, he trades with a long bias. If he is in a bear market, he trades with a short bias. If you don’t know what kind of market you are in, you have no business trading, he says. The author coined the phrase ‘bulls and bears make money; pigs get slaughtered’.

Now, if you are a long-term investor, you don’t have to be concerned with trying to short-sell. You are more than likely to get into trouble. Simply replace the terms ‘long’ and ‘short’ with ‘risk-on’ and ‘risk-off’. Again, I am talking about satellite holdings here. You don’t have to overthink the core part of your portfolio.

Bull or bear?

The Nikkei 225 index gained around 28% last year. After such a positive start to the year, it is widely expected to keep on trucking. It’s pretty clear we are currently in a bull market. If you live in Japan and have a need for JPY base currency, then Japanese stocks are a good place to be.

The only question is what could go wrong? What could bring an end to the bull market?

I think the main short-term danger is a recession in the US. Although the financial press continues to focus on the ‘soft landing’ narrative, history tells us that rate-tightening cycles rarely have a happy ending. Depending on the depth of the recession, US stocks could fall anywhere between 20-50%. I don’t see how Japan just keeps sailing on if that happens, no matter how much better value stocks here may be. If you have already loaded up your investments for the year, I don’t think that’s a bad thing but be prepared to navigate some choppy seas. So it may not be a reason to go risk-off, but be prepared for some volatility.

The BOJ is another matter. If they actually did try to raise rates we would probably experience more than a minor squall. My expectation is they daren’t even try but let’s keep an eye on them. At year-end, I was watching a news feature where they interviewed Japanese business leaders and asked them their views on the stock market for 2024. When asked what they thought was the biggest danger to the Nikkei bull market, the majority of them said ‘the election of Donald Trump’. Interesting…my feeling is these guys need to look a little closer to home.

I’m not even going to get into geopolitics. Lots of risk there, but what are you gonna do?

Outside of Japan, US markets are making all-time highs. However, when you look under the hood, the good cheer is really driven by one group of stocks, known as the Magnificent Seven. If this is a new term to you, the stocks are Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. The size of this group is truly staggering – last time I looked, the combined market cap was around $11.7 trillion. That’s about equivalent to the entire stock markets of Japan, the UK and Canada combined! This group returned around 107% in 2023.

So this bull market is clearly a Magnificent Seven bull market, and the narrative driving it is AI. If you own any kind of global stock fund, go and check their top ten holdings. I’ll bet you that these seven stocks feature prominently.

This group of stocks are a must-own. If you feel you don’t own enough of them, a US recession and corresponding sell-off in the stock market could present a nice opportunity.

Emerging markets could be worth a whole new post, but here’s the tldr: everyone is buying India, not China.

US government bonds got clobbered through this rate hike cycle. If you bought them after the clobbering, you will probably do well as rates eventually subside.

I’m from the UK, so I usually keep an eye on the market over there, but wow, that does not look to me like a place I would want to allocate capital unless I was actually moving back there. Everything about it screams bear…

The biggest bull of all

Of course, the heavyweight champion of satellite holdings is my personal favourite. Yes, the Bitcoin-led crypto bull market is upon us. I already wrote the post on that, it’s right here. You know what to do.

Or do you? I saw a great tweet by Tuur Demeester earlier, in which he said that many people will adopt crypto reluctantly. ‘Hate buying’ he calls it. He also points out how the SEC just ‘hate approved’ the spot Bitcoin ETFs. So why are people going to buy something they hate in the end?

The answer, perhaps, lies in the ongoing debasement of Fiat money, which has accelerated considerably since the 2008 financial crisis. Raoul Pal talks about this a lot and has some great charts. You think your stocks are going up, but really it’s just the purchasing power of your money going down, and you are barely breaking even. People are gradually waking up to this. And there are not many assets that are likely to outperform this money debasement over time. Gold is not getting there. Tech stocks will probably do it, and crypto will likely do it too. Maybe you’re not ready yet, but one day you will be, and you might hate it, but you will probably buy it in the end. Better to rip off the band-aid now perhaps?

On that note, I wish you a happy and prosperous 2024!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.