Anyone who has lived in Japan for a while knows the feeling: a faint tremor, something moving in your peripherals, like the train next to yours slowly pulling away and you’re not sure which carriage is moving. You look up at your partner/friend/co-worker…

Are we shaking?

Earthquakes are not always so subtle of course. Sometimes that faint rumble becomes something bigger. And sometimes, it’s just a heavy truck passing by outside.

Did you feel that? Maybe it was just me? Of course, the market is not just one stock but, if you had to pick a name that has driven US markets to new highs this year, it would be Nvidia. Sure, your Apples and your Microsofts have been strong too, but nothing quite like this. And last week we finally saw a hint of weakness. It would hardly be the first dip this year – questions were asked in mid-February and again in mid-April. What we haven’t really seen is a broadening out of the stock rally into other industries. Charlie Bilello points out here that the top 5 holdings in the S&P 500 now make up 27% of the index, the highest concentration since 1980. He also notes here that the index’s P/E ratio moved above 25 last week, the highest level since Q1 2021.

So, the AI hype-driven tech boom (or is it a bubble?) is still the dominant narrative driving the US market. George Soros once said: ‘When I see a bubble forming, I rush to buy, adding fuel to the fire.’ This is precisely what less savvy investors do too. However, they are rarely as clever as Soros when it comes time to take profits and get out.

Pockets of recession

US economic data continues to come in better than expected. Certainly better than small businesses and low-income families are feeling at this point. To wildly misquote one of my favourite writers, William Gibson: ‘Recession is already here – it’s just not evenly distributed.’

This one-hour podcast with James Lavish is worth a listen if you want to get a better understanding of the impending US debt crisis. He talks about how pockets of recession are already forming, they just haven’t spread broadly across the economy yet.

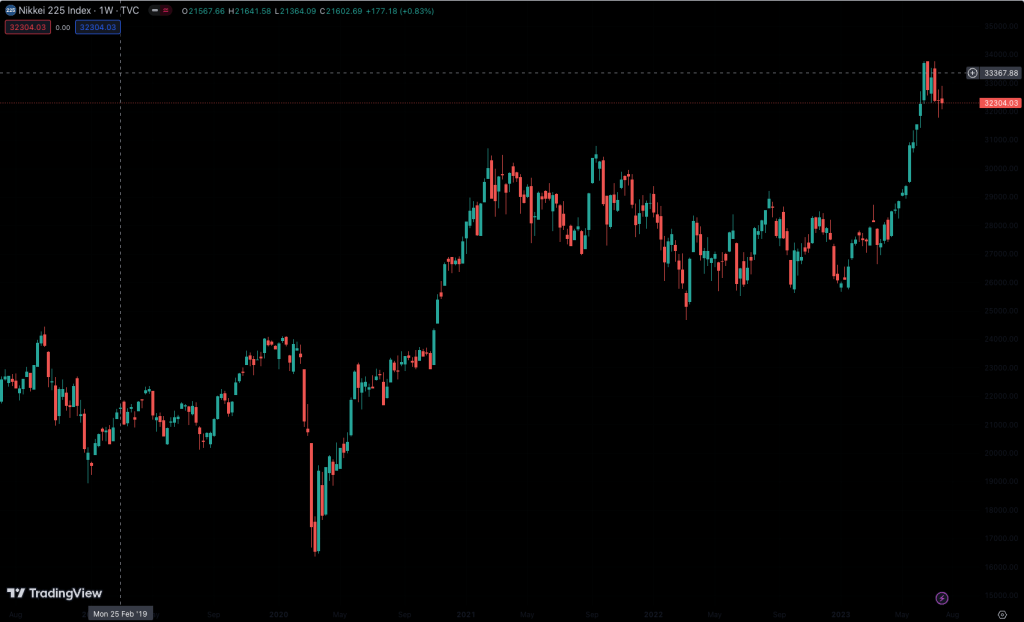

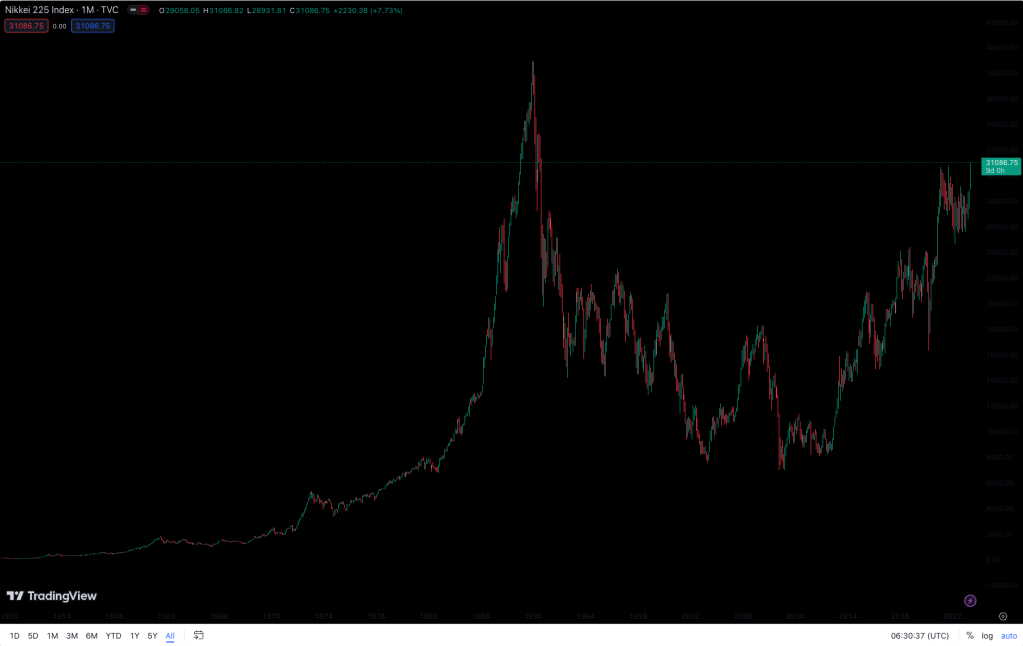

Are Japanese stocks stalling?

Speaking of debt crises, how is Japan doing? USD/JPY is creeping ever closer to the ¥160 level. Rubbing salt into the wound, the US has just put Japan back on the currency manipulator watch list. This could all be solved by the Bank of Japan raising rates in a hurry but it’s the debt that makes that rather difficult. Bad demographics, sky-high debt to GDP and a doomed currency – good thing we choose to live here for the harmony and the mild weather, desho?

After a fantastic run, there are signs that Japanese stocks are stalling too. (are we shaking?) Foreign investors, who played a significant role in driving the market to post-bubble highs, have largely been unloading in the last couple of weeks in the face of lacklustre economic data and persistent yen weakness. The Bank of Japan can no longer be relied on to buy ETFs on down days either. Stocks take the stairs up but they’re known to take the elevator back down…

Meanwhile, the Norinchukin Bank has gotten itself into quite a pickle. The fishers, farmers and foresters cooperative was long US treasuries and, trying to be sensible, it was currency hedged. That meant it endured the two-year rout in US bonds without any of the benefit of the strong dollar when converting holdings back into yen. As a result, it is having to fire sale around $60 billion of its $310 billion in foreign assets and eat the loss. I have preached for some time that currency is the biggest risk most investors don’t know they are taking, but I never considered getting burned like this by being currency hedged – ouch!!!

To sell or not to sell?

This is beginning to sound like a terribly negative post, but it’s really just a reflection of my thoughts about taking some profit and de-risking for a while. Just to be clear here, I am talking about adjusting tactical or satellite holdings. I don’t see any reason to make any changes to my long-term core investments. I own US tech stocks and a range of Japanese stocks in my core portfolio and am happy to keep them. However, I also own some of these same assets tactically – that’s to say I bought them at an opportune time with a shorter time frame in mind. Those are the ones I am getting tempted to sell.

Everyone is a genius in a bull market. You will notice though, that no one wants to tell you when to sell. Except maybe the macro doomers, but they’ve been telling you to sell the whole time markets have been rising, so let’s leave them out of this. For sure, it is smart not to fight the trend, and in US tech and Japanese equities, the trend has been unmistakably upward. There is also the fear of leaving money on the table and looking silly if markets pump after what turned out to be a minor correction.

However, we are talking tactical and that means buy low, sell high. If you are yen base currency and you bought US tech stocks a couple of years ago, not only have you made nice gains in the stocks, but the weak yen has boosted your profits significantly. You could be forgiven for cashing out back to yen and taking the win. The same can be said if you got trapped in yen and instead bought Japanese stocks to counter inflation and the market then went off to the races. That’s a nice win too, but you have to sell before you take the victory lap.

The big question is, supposing you sell, what do you do with the money next? If you are going to spend it on a sports car or a nice holiday, good for you! But if you still have to worry about keeping pace with inflation and currency debasement, you are going to have to find a suitable home for it. Sitting in cash for a few months and then catching a big drop in markets would be ideal, but we are not playing on easy mode here.

These are the thoughts I have on a Monday afternoon with the Nikkei up +0.5% to ¥38,804 and US stock futures looking steady. Perhaps I’ll just sit on this one for a while. Doing nothing is frequently the smartest play, but did you feel that? Maybe we are shaking?

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.