So, here we are. Overnight, the Federal Reserve announced a rate cut of 50bps, the first cut in four years. Projections imply a further 50bps later this year and another 100 bps in 2025. Welcome to the rate cut cycle.

US markets reacted cautiously, with stocks rising ahead of the announcement only to give back those gains and close down slightly. 50bps is considered a big initial cut, so it will be interesting to see how markets behave over the next few days as they digest the news.

Surprisingly, the yen fell against the dollar to the upper ¥143 range and Japanese stocks were up strongly this morning. Again, time will tell if the initial reaction is the correct one.

The macro gurus will no doubt be fighting it out as to whether the US economy is coming in for the much-vaunted soft landing or heading for recession. Jerome Powell sounded upbeat on America’s economic prospects and made clear that he views the larger cut as a move to prevent the Fed from falling behind.

We will find out in due course.

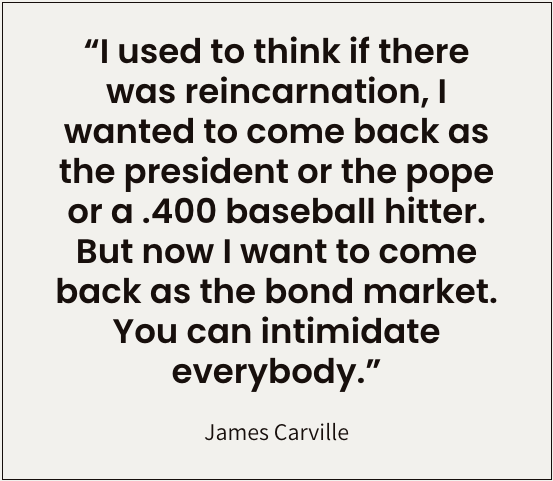

Sometimes the most obvious take is the correct one: rate cuts are generally bullish for risk assets over time, although we may need to ride out some volatility in the short term. The doomers will keep dooming but optimists make more money in the long run:

“Bulls make more than bears, so if anything being an optimist about life and about things in general is a great attribute as an investor. You just can’t be starry-eyed and naive.” — Stanley Druckenmiller

Deja vu

Three assets that are a hot topic in this new environment are gold, silver and bitcoin. It’s funny because I remember these three getting a lot of attention four years ago. Granted, the post-Covid crash environment in 2020 was very different from today – for a start, the Fed funds rate was already at zero in September 2020. However, it’s interesting how things move in cycles. Gold is around all-time highs now and silver enthusiasts are clamouring for a breakout. It has a strong 2020 feel to me, so I thought I would take a look back and see what happened four years ago.

Observe the five-year charts:

As you can see, both gold and silver reacted quickly to the stimulus injection that followed the March 2020 Covid shock. Liquidity is generally good for hard assets. Bitcoin took longer to catch alight but when it did, the fireworks were spectacular as it took out the previous all-time high of $20k and then marched right on to $60k and then $69k in 2021. That move started at $6k at the end of March 2020 and BTC was still only $11k on 19 September 2020.

I like all three of these assets in the current environment, but I like one much more than the others.

Game time soon, anon.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I hope you are enjoying Obon and the summer holiday. After a market crash and a Nankai Trough earthquake warning, things feel a little calmer this week. Hopefully, there won’t be any more ‘big events’ in August other than the local matsuri.

However, September is approaching and it feels like that will be the time to get locked in and focused. So here are a few thoughts as we speed into the last four months of the year!

US markets

There is a slew of economic data coming out of America this week, with the Producer Price Index (PPI) coming in a little softer than expected last night. CPI is tonight and another soft print will heighten expectations of a Fed rate cut in September. Toys will be thrown if Chair Powell does not deliver, but I’m also becoming a little more cautious about the outlook for stocks if he does go ahead and cut. History favours a recession scenario at the end of a hiking cycle. A lot of effort has gone into the soft landing narrative, so we should be on our guard. No reason to make adjustments to long-term investments but things rarely go as smoothly as the crowd expects.

That said, the completion of the US election will remove a lot of uncertainty, regardless of who wins.

Yen / Japan stocks

After starting August with a bang, the Bank of Japan has swiftly backed down from any plan to raise rates again this year. They got as far as 0.25% and the stock market melted down. They didn’t even get to the bond market jitters part of the project. I would love to hear from anyone who can explain how the BOJ will go about a meaningful tightening from here. Imagine what rates at 0.5% would look like. How about 1%?

I just saw a Bloomberg headline that said that PM Kishida is stepping down in favour of a leader who is supportive of the central bank’s efforts to normalise policy. Best of luck to whoever picks up that poison chalice!

Let’s just call BS, shall we? You can’t normalise a ponzi.

Nonetheless, if the Fed does begin to cut, the yen should strengthen. I don’t know how far it will get. 130? 120? 100? It doesn’t matter, because once that cycle is over it is only going the other way. You can save the bond market or the currency and no one is sacrificing the bond market.

I have said it before but I’m nothing if not a broken record: if you are going to spend your future money outside of Japan, you should forget about those alluringly cheap Japanese value stocks and get your money out of yen and into your base currency while you have the opportunity.

If you are here for the long haul, by all means, have at it. In the shorter term, Japanese stocks should do ok and I would even be tempted to look for names that will benefit from a stronger yen. Exporters that did well under the weak yen don’t seem such a great idea going forward.

Getting hard

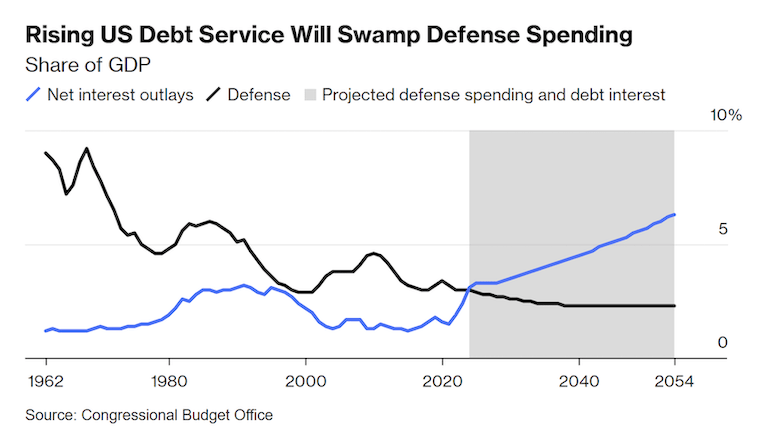

With the US election looming, the cynical among us would be watching out for a liquidity boost to pump up the US stock market. Rather than the Fed, we should probably be looking at the treasury to provide the liquid refreshment. This ‘Bad Gurl Yellen’ piece by Arthur Hayes goes deep into the fountain of liquidity that is about to spring forth. In short, the treasury needs to lower the debt-to-GDP ratio, and it will do so by issuing yet more debt.

The Congressional Budget Office projects that interest payments on America’s debt will total $892 billion in fiscal 2024 and rise significantly in the next decade.

If you are wondering what that looks like, get a load of this chart:

Tell me you’re gonna print more money without saying you’re gonna print more money…

I wrote about currency debasement and and how to protect yourself in Harden up your assets! If you are looking at stocks to plough your hard-earned money into right now, that’s one way to do it but maybe there is a better option.

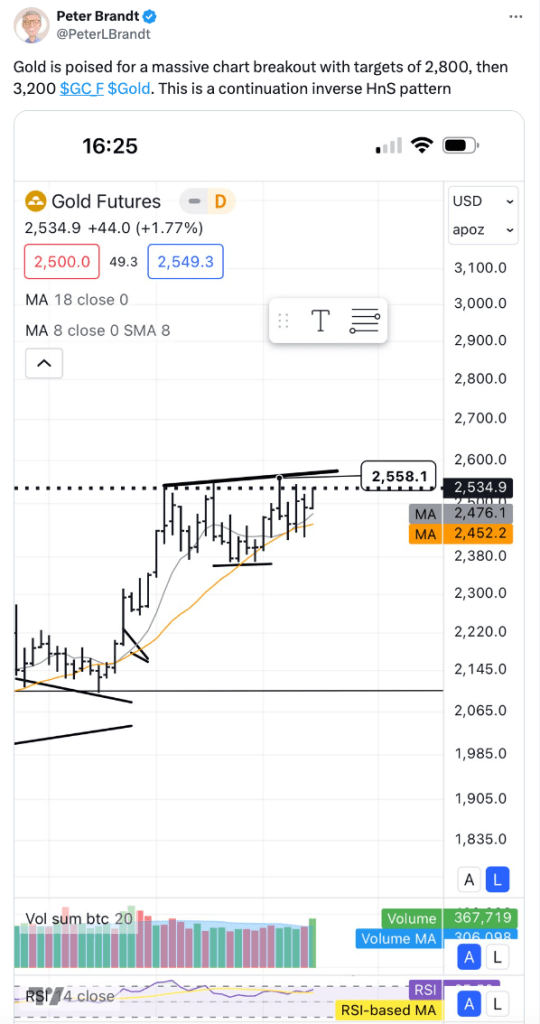

As you can see, some technical traders are getting excited about gold. JP Morgan agrees, arguing that the structural bull market remains intact and forecasting an average price of $2,500 in Q4 and $2,600 in 2025. Geopolitical tensions, rate cut expectations, central bank buying and ETF flows all point to elevated gold prices – report here.

Of course, those are short-term targets and the real point of owning gold is to protect against currency debasement over time. Remember, this is what you’re up against:

Digital gold

Ever the broken record, allow me to point out once more that the boring phase of the Bitcoin bull market is drawing to a close. We probably bounce around for a few more weeks, maybe even a couple of months. The timing is difficult to predict but I expect significantly higher prices by the end of the year. And more to come in 2025. If you are thinking of getting on the train, you don’t have long left…

Despite a reshuffle of the Democratic nominee, pretty much everything I wrote in the Bitcoin bull market update still stands. All aboard!

If you are still trying to get your head around the hardest asset on the planet, the presentations from Michael Saylor’s keynotes are a great resource.

Don’t say I didn’t warn you!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s the 1st of August. The two big central bank decisions are behind us and summer is in full swing. So what comes next? Where will markets be at the end of this year? Nobody knows the answer to that question but I can almost guarantee you one thing: there is turbulence ahead.

Just like Japanese summer, the volatility already got started in July. However, we seem to have entered a new phase and central banks are the main drivers of the momentum shift.

Having hiked rates to levels unseen in 15 years, there is little doubt that the BOJ has entered a tightening cycle. Governor Ueda did not rule out another hike this year and the yen responded quickly to his comments, rising to 150 against the dollar. Today it is trading at around 149. Weston Nakamura sees 152 as the most important price level in global macro right now and we are already well beyond it.

Japanese stocks reacted positively to yesterday’s decision, pumping across the board. However, the Nikkei 225 index slumped -2.5% today as exporters felt the pinch of a stronger yen.

US tech investors rotate into small caps

In the US, Fed chair Powell left rates unchanged while hinting that he is getting closer to a cut. The market fully expects this to happen in September and there will be visible disappointment in people’s brokerage accounts if it doesn’t. Volatility is already rearing its head. Tech stocks have sold off over the past month amid fears that the AI bubble might be bursting. Nvidia has been trending down from its 6 June high of $140.76 and a -7% dump on 29 July seemed ominous, but last night it pumped +12.7% after AMD’s better-than-expected earnings release. Go figure…

Hats off to strategist Tom Lee for calling the rotation into small caps. IWM has been the main beneficiary of the tech selloff.

The crypto coaster rolls on

Not to be outdone by chipmakers, crypto remains unpredictable over short time frames. At the Bitcoin conference in Nashville last week, none other than Donald Trump showed up to play to the crowd. His list of “promises” included: keeping the Bitcoin the US government has seized as a strategic reserve, (yes, wow!) firing Gary Gensler on day 1, ending the democrat’s war on crypto and making the US a leader in mining.

The air quotes around “promises” don’t need much explanation. Trump has zero interest in crypto and is plainly exploiting the dem’s antagonistic stance toward the industry for votes. But don’t let that distract you from the bigger picture: governments are examining Bitcoin as a strategic hedge against their own money-printing excess. The fact that this conversation is even happening is remarkable. Bitcoin game theory is going to get very interesting in the months and years ahead.

Trump to the Bitcoin Bros: “Have a good time with your Bitcoin and your Crypto and everything else you’re playing with.”pic.twitter.com/9Mf1zr1mGX

Bitcoin is back in the $64,000 range today, as it appears that the Biden/Harris camp may be selling off the reserve that Trump promised to keep. It’s never boring. See my Bitcoin bull market update for more.

Meanwhile, investors in Japan received a lesson in FOMO from Bitcoin proxy Metaplanet Inc. this week. Shares went on a tear after the company announced its Bitcoin treasury strategy in April and many people piled in late. Now the stock is coming back down to earth with a bang as the excitement wears off. Shares are down over -70% from their 24 July high and the move down doesn’t look done yet. Of course, every man and his dog wanted the stock when it was skyrocketing and nobody is interested now. There’s a clear lesson there. That said, I wouldn’t be surprised if Metaplanet makes another run if/when Bitcoin makes a decisive break above its previous all-time high and enters the parabolic phase of the cycle. Timing is everything in narrative-driven trades.

So, what to do?

I have noticed an uptick in clients trying to position and trade some of these macro moves, particularly the USD/JPY angle. The problem with access to unlimited information, content and opinion is the urge to react to it and do something. So here’s my two cents:

The summer, and perhaps the rest of the year, will see some turbulence. Volatility goes both up and down. Overall, the backdrop keeps me optimistic. Rate cuts in the US are coming – it’s just a question of when. As things currently stand, it would not be a panic cut, which is constructive for risk assets. US stocks, gold and crypto should react accordingly. Regardless of who wins, the US election will remove a lot of uncertainty. If you are broadly diversified, you could do a lot worse than fastening your seatbelt and taking a nap for a while.

If the BOJ is tightening and the Fed is loosening, the yen should continue to strengthen. This is going to put some strain on export-related Japanese stocks and the market as a whole looks more unpredictable than the US. Governor Ueda said he doesn’t think the rate hike will damage the Japanese economy. He’s probably right for now, but let’s see what kind of toll a series of hikes will take. The last time the BOJ tried to hike was 2007/2008 and that move was reversed in a hurry…

If you have been waiting for your chance to escape JPY and get into your base currency, that window is opening. Don’t miss it – long term it does not look good for the yen.

Stay hydrated folks!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s pretty incredible that the US Federal Reserve has gone through a 27-month hiking cycle and US stock markets are at all-time highs. Unless you’ve been living under a rock during this time, you are probably aware that the main growth driver has been the intense hype surrounding artificial intelligence (AI) and more specifically, generative AI.

What is AI?

The Encyclopedia Britannica defines AI as ‘the ability of a digital computer or a computer-controlled robot to perform tasks commonly associated with intelligent beings’. The US company Nvidia says AI is ‘the capability of a computer program or a machine to think and learn and take actions without being explicitly encoded with commands’.

In March 2023, Bill Gates published a blog post titled ‘The Age of AI has begun’. In it, he says: ‘The development of AI is as fundamental as the creation of the microprocessor, the personal computer, the Internet, and the mobile phone. It will change the way people work, learn, travel, get health care, and communicate with each other. Entire industries will reorient around it. Businesses will distinguish themselves by how well they use it.

Technological revolution or a waste of resources?

I read a couple of interesting threads about AI last week. The first one by David Mattin considers the recent UK election as the last ‘pre-AI’ election we will hold. He sees a world entering a period of deep economic transformation that will change how we live and work and accelerate the process of scientific discovery. Rather depressingly, he expects this transformation to split society into two camps: enthusiasts/accelerationists, who want to lean into this new technology and sceptics/decelerationists, who want to resist the incursion of technology into daily life. This split is not hard to imagine when you look at how divided the Western world has been on almost every issue of late.

The second thread, by Ed Zitron, summarises a recent Goldman Sachs report on generative AI, which brutally dismisses Chat-GPT and its ilk as unreliable and power-hungry. The report concludes that generative AI is unprofitable, unsustainable and fundamentally limited. Moreover, the huge surge in AI-related stocks is a bubble that will soon burst. Original report here.

I don’t think my opinion on the first part is worth much, but I am not really interested in taking sides. There are clearly opportunities for massive positive change and there are also equally glaring risks. In a perfect world, these would be balanced sensibly but that world doesn’t exist. Things are about to get interesting…

As far as generative AI goes, time will tell. I think the most common complaint people have is that they don’t want gen-AI to write stories, produce art and know everything. They want it to do all the boring jobs that we humans don’t want to do and free us up to be more creative.

Investing in AI

From an investment standpoint, I don’t think AI can be ignored. It seems imprudent to dismiss the whole field as a bubble. However, if some parts of the industry are in a bubble, the key question is how long can the bubble continue inflating? As George Soros has pointed out, there is a lot of money to be made by rushing into a bubble. The tricky part is getting out before it bursts.

There are relatively few pure-play AI stocks to invest in. However, many great companies are using AI technology and making investments in AI. I have picked up a few below that I think are worth watching. This is neither an exhaustive list nor a recommendation to invest. Just some ideas to get you started so you can do your own research. (performance is quoted up to 15 July 2024)

Nvidia Corp (NVDA) and Super Micro Computer Inc (SMCI)

If I asked you what the best-performing AI-related stock is over the past 12 months, you could be forgiven for answering Nvidia. However, Nvidia has actually been beaten by a company it is partnered with – Super Micro.

The Motley Fool did a nice write-up on these two companies here: Essentially, they aren’t really competitors, they complement each other. NVDA designs graphics processing units (GPUs) which, among other things, are used for AI model training. SMCI designs servers and it takes Nvidia’s GPUs and other components to make them and sell them to its clients. These are what some people refer to as ‘pick and shovel’ investments in AI.

Of all the big-name tech companies, Microsoft is perhaps the most bullish on AI. The company is accelerating its own AI commitments and has invested some $13 billion in OpenAI in a partnership that dates back to 2019. Microsoft has integrated all of its generative AI assistants into a single AI product named Microsoft Copilot. Copilot offers both free and paid versions and is integrated into a wide range of Microsoft applications providing access to Chat GPT-4 and DALL-E 3.

Investors can keep up with Microsoft’s AI developments here.

Shares are up +21.2% in 2024 so far.

Arm Holdings ADR (ARM)and Softbank Group Corp (9984)

Majority owned by Softbank Group, Arm Holdings was listed on the NASDAQ in September 2023 and has quickly established itself as a major force in AI. The company architects, develops and licenses central processing unit (CPU) products and related technology which semiconductor companies and original equipment manufacturers (OEMs) rely on to develop their products. 99% of smartphones run on Arm-based processors and Arm has shipped 287 billion chips to date.

In Q4 of fiscal 2024, Arm reported its highest-ever revenue of $928 million, up 47% year-on-year. Shares are up +216.5% since listing and +136.3% year-to-date.

Softbank Group has had its ups and downs but is recovering in 2024. Led by the charismatic and controversial Masayoshi Son, Softbank Group has aggressively invested in a broad range of fields including robotics, AI, real estate, e-commerce, telecoms and more. It would be fair to say that the company has backed more than its fair share of losers, but Arm is proving to be one of its better bets.

AI stands at the forefront of Softbank Group’s vision and strategy so investors should expect the heavy investment in AI-related companies to continue. CEO Masayoshi Son says: ‘We are heading for an AI revolution, and we will be the investment company for the AI revolution’.

Softbank Group shares are up +81.1 % so far in 2024.

These are just a few ideas to get you started. There are many more companies involved in AI that are worth considering. Both Amazon and Meta are making huge investments in AI. Arista Networks (ANET) AI networking has driven impressive returns over the past five years. In Japan, NEC Corp is developing a range of AI technologies under the banner of ‘NEC the Wise’. And, of course, the huge boom in semiconductors has largely been driven by demand from AI.

The majority of investors will already have a larger allocation to AI-related stocks than they probably realise. Any S&P 500 or NASDAQ tracker will have significant exposure, so it isn’t always necessary to make an effort to dig out the next big name.

As for timing, returns over the last 3 years have been extraordinary. It remains to be seen if this is a bubble that is soon to burst, but sudden deep corrections can occur at any time. If you are a long-term believer in the AI narrative, there is no rush to pile money into the space in one go. Dollar-cost averaging is a solid strategy, and so is adding on significant dips.

Whether you are allocating passively or building a portfolio of AI satellite holdings, things are going to get interesting and maybe just a little weird.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Of the six main asset classes, the one that stands out as perhaps the least understood is bonds. Although most people have a general idea of what bonds are and how they fit in an investment portfolio, they are incredibly complex financial instruments and misconceptions abound. I frequently hear people wonder if there is even any need to own them. So, let’s take a look and see if we can get a clearer picture of how bonds work and why they are useful.

Why do bonds exist?

Bonds are used by governments and corporations to raise capital. If a government issues a bond, it is borrowing money from the public to finance itself. Companies issue bonds so that they can expand operations or fund new business ventures. So if you buy a bond, you are loaning a government or a corporation money.

The key components of bonds

Issuer: bonds can be issued by governments or corporations. Each issuer carries a different level of credit risk, with bonds issued by developed world governments considered the safest. Bonds from issuers with a lower credit rating carry more risk of default and pay a higher yield to compensate for that risk.

Coupon rate: this is the annual interest rate paid to bondholders, expressed as a percentage of the bond’s face value. (often referred to as par value) So a bond with a $1,000 face value and a 5% coupon rate pays $50 a year in interest.

Maturity date: bonds have a specified maturity date when the issuer repays the bond’s face value to the bondholder. Maturities can range from a few months to several decades, influencing the bond’s risk and potential return. A 30-year bond is regarded as more risky than a 5-year bond as more factors can affect the issuer’s ability to repay the debt over longer periods.

Market price: the price of a bond in the secondary market can fluctuate based on changes in interest rates, credit quality and market demand. If the bond’s market value is higher than its face value, it is trading at a premium. If it is lower than face value, it is trading at a discount.

Understanding bond prices

Bonds can be bought and sold on the secondary market after they are issued. A bond’s value in this market is determined by its price and yield. The key thing to understand is that a bond’s price moves inversely to its yield. A bond’s price reflects the value of the income it can provide. So, if interest rates are falling, the value of older bonds that were sold in a higher interest rate environment increases and their price goes up. In a rising interest rate environment, older bonds become less valuable as investors would rather buy newer bonds paying higher yields.

You can see this clearly in the performance of the above iShares TLT long-term treasury ETF. After the 2008 financial crisis, interest rates were kept low to stimulate economic recovery. Just as rates began to drift upwards, Covid happened and rates were slashed again. Bond prices increased significantly in this low interest rate environment and so the price of the ETF rose. When the Federal Reserve began raising interest rates in late 2021, bond prices fell heavily and continued to fall throughout the Fed’s tightening cycle, which is now nearing its end.

You could make a pretty strong argument that now is a good time to be buying a long-term treasury ETF like TLT. When the Fed begins cutting rates, bond prices will recover and investors will be able to capture capital gains along with income.

Conversely, having held interest rates low for longer than most other developed countries, Japan is now in a rising interest rate environment as the Bank of Japan attempts to slow down inflation. This means the price of Japanese Government Bonds is likely to fall.

Why own bonds?

Investors may choose to own bonds for a range of reasons. Those reasons include:

Steady income – particularly applicable to retirees and investors who require income for other reasons

Capital preservation – if held to maturity, bonds issued by institutions with strong credit ratings come with a low risk of loss of capital

Portfolio diversification – bonds offer a good counterbalance to equity market volatility

Capital appreciation – as above, bond prices can appreciate when central banks are cutting interest rates

A hedge against economic downturn – in the US and Europe, inflation is cooling and economies are slowing. This means the income from bonds will be able to buy more goods and services, making bonds more attractive

How to buy bonds

For a typical retail investor, there is no need to buy individual bonds. Just like equities, investors can choose from a range of active or passive strategies offered by bond funds or bond ETFs. Generally, a passive ETF provides perfectly adequate exposure to bonds without any stress or hassle. For example, Blackrock’s iShares ETF series offers 135 different bond ETFs – more than enough to build a diversified bond allocation. The fixed income part of a well-diversified portfolio will generally contain a blend of shorter/medium/longer-term government bonds along with an allocation to more risky corporate and emerging market bonds.

Be sure to pay attention to your base currency when you build such a portfolio. If you are planning to spend the money in the UK eventually, you should be looking at UK Gilts as the core of your bond holdings rather than US treasuries. Don’t be afraid to engage professional help if you are not comfortable organising this yourself.

As to whether owning bonds is really necessary or not, that’s obviously an individual call to make. I would comment that if you are young and just getting started with investing a little money every month, averaging 100% into equity ETFs is a perfectly acceptable strategy for the first few years.

However, after you have been investing for some time and have built up a larger pool of capital, it is probably time to start thinking about diversifying into other asset classes to protect against sharp drawdowns in equity markets. Bonds become a useful tool as you shift from an aggressive capital accumulation strategy to a more balanced portfolio that offers growth and income with a degree of capital preservation.

Hopefully, this post goes some way to explaining what bonds are, how they work and the benefits of investing in them. Feel free to comment or send questions any time!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Happy New Year everybody! I hope you all enjoyed a peaceful winter holiday and are back, raring to go and make big things happen.

For some reason, I had a feeling that this was going to be a challenging year and it didn’t really get off to the best start in Japan. For those interested, I was googling around yesterday trying to figure out the best way to donate to disaster relief on the Noto Peninsula. I found this page run by Ishikawa Prefecture. You can download a form here to request a receipt for your donation for tax purposes. Donations qualify for the donation deduction and there is a useful FAQ on the tax treatment of donations here.

So yeah, earthquakes, runway collisions, fires and we’re only a third of the way through January!

From a personal finance and investing perspective, there is some exciting stuff going on though. The New NISA has launched. I logged into my SBI account and it was pretty simple to get started. I have already set up the ‘tsumitate’ allocation and started buying some stocks for the ‘growth’ allocation. Clearly, everyone else is doing the same thing as the Nikkei is pumping so far this year!

I posted a couple of interesting takes on Japan on ‘X’ yesterday: an optimistic look at the year ahead from Jesper Koll and a much darker look at the demographic issues facing Japan from author Nire Shūhei. It always pays to look at both sides.

So how to invest in the year ahead? If you have been reading this blog over time, you will know that I divide investments up into core and satellite allocations. The core is a diversified portfolio weighted heavily to your base currency that just gets rebalanced once a year. This would typically account for around 70-80% of your investments and the idea is to keep adding to it as much as you can. If it’s a bit dull and boring, you are probably doing it right!

The other 20-30% can be allocated to satellite holdings, which may be a little more racy and exhibit a higher risk-return profile. If this part isn’t fun, then you are probably doing it wrong!

Satellite holdings will change over time depending on the economic environment we are in. So how are things looking?

Some thoughts

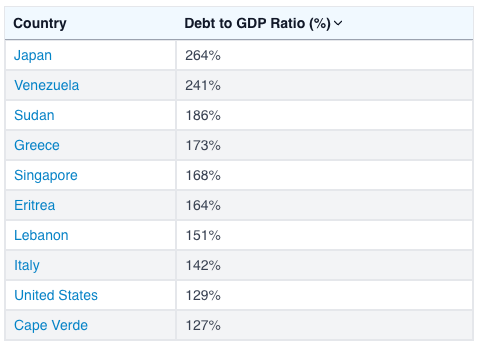

On the one hand, things look pretty much like they did for most of last year. The Fed funds rate is 5.5%. People who are obviously long risk assets have been trumpeting the start of rate cuts as early as March, but Mr Powell doesn’t look like he’s in much of a hurry to me. Although the Bank of Japan has adjusted its yield curve control policy and allowed long-term interest rates to rise a little, it is still continuing with its negative interest rate policy. There has been a significant amount of speculation, from both within and outside Japan, about when the BOJ will ‘normalise’ rates – I do love this term, like there is a way to return to normal with government debt to GDP at 264%! Gulp…

Despite noises being made about an exit from negative rate policy, it’s notable how quickly these ideas get put on the shelf. Comments I have heard recently include: ‘The earthquake will make it harder to normalise rates’. Probably true, but any excuse to avoid the inevitable. The Labour Ministry’s November report showed that real wages have declined for the past 20 months in a row, so there’s no sign of the mystical ‘virtuous cycle’ of wages outpacing price rises that would signal a move from the central bank.

It’s not going to happen, is it?

So if you’re waiting for the yen to get back to something sensible against the US dollar, good luck! Markets can remain irrational longer than you can remain solvent enough to go on a nice holiday abroad…

Japanese stocks, for the most part, are loving the weak yen. Any company with significant exports and profits abroad will see those profits magnified when converted back to yen. If you’re wondering why your Toyota shares are doing so well, there you are.

What kind of market is this?

Some time ago, I read the book Reminisces of a Stock Operator by Edwin Lefèvre. It’s considered somewhat of a bible by many investors. While there are some interesting tales of hi-jinks and high leverage, there was only really one key thing I got out of the book, but that one thing has stuck with me: Traders and investors should always know if we are in a bull market or a bear market.

It’s always the simple things that have the most impact, right? The protagonist in the book is a stock trader and his big-picture strategy is very simple: If he is in a bull market, he trades with a long bias. If he is in a bear market, he trades with a short bias. If you don’t know what kind of market you are in, you have no business trading, he says. The author coined the phrase ‘bulls and bears make money; pigs get slaughtered’.

Now, if you are a long-term investor, you don’t have to be concerned with trying to short-sell. You are more than likely to get into trouble. Simply replace the terms ‘long’ and ‘short’ with ‘risk-on’ and ‘risk-off’. Again, I am talking about satellite holdings here. You don’t have to overthink the core part of your portfolio.

Bull or bear?

The Nikkei 225 index gained around 28% last year. After such a positive start to the year, it is widely expected to keep on trucking. It’s pretty clear we are currently in a bull market. If you live in Japan and have a need for JPY base currency, then Japanese stocks are a good place to be.

The only question is what could go wrong? What could bring an end to the bull market?

I think the main short-term danger is a recession in the US. Although the financial press continues to focus on the ‘soft landing’ narrative, history tells us that rate-tightening cycles rarely have a happy ending. Depending on the depth of the recession, US stocks could fall anywhere between 20-50%. I don’t see how Japan just keeps sailing on if that happens, no matter how much better value stocks here may be. If you have already loaded up your investments for the year, I don’t think that’s a bad thing but be prepared to navigate some choppy seas. So it may not be a reason to go risk-off, but be prepared for some volatility.

The BOJ is another matter. If they actually did try to raise rates we would probably experience more than a minor squall. My expectation is they daren’t even try but let’s keep an eye on them. At year-end, I was watching a news feature where they interviewed Japanese business leaders and asked them their views on the stock market for 2024. When asked what they thought was the biggest danger to the Nikkei bull market, the majority of them said ‘the election of Donald Trump’. Interesting…my feeling is these guys need to look a little closer to home.

I’m not even going to get into geopolitics. Lots of risk there, but what are you gonna do?

Outside of Japan, US markets are making all-time highs. However, when you look under the hood, the good cheer is really driven by one group of stocks, known as the Magnificent Seven. If this is a new term to you, the stocks are Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. The size of this group is truly staggering – last time I looked, the combined market cap was around $11.7 trillion. That’s about equivalent to the entire stock markets of Japan, the UK and Canada combined! This group returned around 107% in 2023.

So this bull market is clearly a Magnificent Seven bull market, and the narrative driving it is AI. If you own any kind of global stock fund, go and check their top ten holdings. I’ll bet you that these seven stocks feature prominently.

This group of stocks are a must-own. If you feel you don’t own enough of them, a US recession and corresponding sell-off in the stock market could present a nice opportunity.

Emerging markets could be worth a whole new post, but here’s the tldr: everyone is buying India, not China.

US government bonds got clobbered through this rate hike cycle. If you bought them after the clobbering, you will probably do well as rates eventually subside.

I’m from the UK, so I usually keep an eye on the market over there, but wow, that does not look to me like a place I would want to allocate capital unless I was actually moving back there. Everything about it screams bear…

The biggest bull of all

Of course, the heavyweight champion of satellite holdings is my personal favourite. Yes, the Bitcoin-led crypto bull market is upon us. I already wrote the post on that, it’s right here. You know what to do.

Or do you? I saw a great tweet by Tuur Demeester earlier, in which he said that many people will adopt crypto reluctantly. ‘Hate buying’ he calls it. He also points out how the SEC just ‘hate approved’ the spot Bitcoin ETFs. So why are people going to buy something they hate in the end?

The answer, perhaps, lies in the ongoing debasement of Fiat money, which has accelerated considerably since the 2008 financial crisis. Raoul Pal talks about this a lot and has some great charts. You think your stocks are going up, but really it’s just the purchasing power of your money going down, and you are barely breaking even. People are gradually waking up to this. And there are not many assets that are likely to outperform this money debasement over time. Gold is not getting there. Tech stocks will probably do it, and crypto will likely do it too. Maybe you’re not ready yet, but one day you will be, and you might hate it, but you will probably buy it in the end. Better to rip off the band-aid now perhaps?

On that note, I wish you a happy and prosperous 2024!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

How’s everybody doing? This is a follow-up to my Nikkei ¥40,000? Thinking outside the box piece, which I just happened to post exactly 2 months ago. It’s interesting to see how things have developed since then and then look forward to the last quarter of the year. Yes, I know, it’s almost October. Where did those nine months go???

Remember Monex guy? Two months ago he said the Nikkei 225 was likely to trade in a range of ¥31,000 to ¥33,000 for a while. Gotta give my man credit there, it’s done exactly that. His expectation was that if we can break above that range, we’re heading for ¥40,000. What do you think about that?

If there’s one thing I’ve noticed recently, there’s been a subtle narrative change around the Japan stock market rally. In the first half of the year, it was exactly that – Japanese stocks were broadly rising and outperforming most other developed markets. What has changed, is that the narrative in the news now is more focussed on a Japanese value/dividend stock rally.

So what happened? Well, first, the Bank of Japan has allowed long-term yields to rise up to 0.70% and beyond and then, on 9 September, BOJ Governor Kazuo Ueda said that the lifting of the central bank’s negative interest rate policy will become an option if wages and prices rise. He even said they might have enough data to make a call on that by the end of the year. Despite the talk of interest rates rising, with inflation at over 3%, Japanese investors are realising that sitting in cash is a losing trade. With bonds still offering negative real rates, the money has been pouring into dividend-generating stocks. There’s also a possibility that the revamping of NISA for 2024 has got investors more excited about getting involved in the stock market.

I know it lacks class to say I told you so, but sometimes you need to toot your own horn. This is stuff I figured out some time ago. On 14 September, Nikkei News Plus 9 did a feature on the Nikkei 225 High Dividend Yield Stock 50 Index. There is an ETF that tracks this index and I have owned it since spring 2022 and I covered it in posts in March and October. Here’s what it looks like year to date:

Not bad at all. Ok, enough self-congratulation, there is still a lot to think about here. The big question is, how is this going to play out over the remainder of the year? The fact that financial news programs are starting to fixate on the value/dividend stock narrative is good news if you hold these stocks. Just since the feature on the Nikkei program last week there has been a notable bump in the dividend ETF along with bank stocks, shipping companies, trading companies and steelmakers, which News Plus 9 showcased as examples. So this is now a hot trade which could run for a while, particularly as the talk of exiting negative interest rates heats up. Pick a banking stock and take a look at its performance year-to-date and particularly over the last few weeks!

When a sector gets hot and retail crowds in, it’s often a sign that we are nearing a top. The mania phase can last longer than you expect, but it can also blow off in a hurry. If I didn’t own these stocks already, I don’t think I would be jumping in now. As I mentioned in the July post, these are tactical positions for me, so I am keen to lock in some profit, while also remaining invested to catch any further upside. I have sold incrementally over the past 2 months and reduced my holdings by about 30%. Of course, with hindsight, I feel pretty silly selling anything. I could have just waited and sold higher. But that’s the way it goes – you have to make decisions based on the information you have in real time. So I took some profit, but left two thirds still invested. So far, so good.

So is the Nikkei going to ¥40,000 this cycle? I would be happy to be wrong on this one, but my bet is no. Higher rates, or at least the talk of higher rates, are bad for growth stocks but can be good for value as we are seeing. You would need both to be going up to hit the ¥40,000 mark.

I am still of the view that any attempt at normalising rates in Japan will lead to chaos and a hasty reversal. However, as we are seeing now, even talk of an increase is enough to change market dynamics. And if last night’s Nikkei News Plus 9 program is anything to go by, there is a lot of talk going on! They were feverishly covering how some net banks are raising their rates for fixed deposits to a hefty 0.70%!

From the BOJ’s perspective, a lot of this talk on rates is just that. There’s even a term for central bankers talking up a strategy in order to get the reaction they want from markets – jawboning. It doesn’t change the corner they have painted themselves into. It’s not looking good for the yen folks…

Of course, a lot also depends on the US. Last night’s Fed decision to leave rates unchanged and the plan to hike once more this year was as expected. As they always do in this situation, the Fed is talking up a soft landing. History is not on their side on that one. As the effects of this hiking cycle gradually feed through to the underlying economy, the smart money is still betting on recession. Markets are too interconnected for Japan to keep sailing on if that’s where we are headed.

So no ¥40,000 in the near future, but there could be some more upside for value/dividend stocks. Early next year may get interesting if the BOJ tries to translate some of this talk into action. I plan to have a ready supply of dry powder to allocate if we do take a dive. That’s my view, which I will look extremely foolish for putting in writing if we see ¥40k by Christmas! But if you’re going to invest tactically, you’ve got to have an opinion. Perhaps I should buy a Monex hat to eat if I am wrong…

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

We humans are a complex bunch. I have heard that there are five stages of grief: denial, anger, bargaining, depression and acceptance. With covid, entire countries seem to have gone through their own version of this, which may or may not have included these stages: zero covid, flattening the curve, lockdowns, mass vaccination, and finally living with covid. In the end, it seems, we have to accept and live with whatever pains us.

So are we in a bear market yet? Some would argue not – the S&P 500 is down some 18% from its January peak, and bear markets are defined as falls of 20%. So they are correct, but the NASDAQ has already passed 20%, so it sure does sound a lot like denial, don’t you think? I’m generally an optimist, but I’ve come to appreciate the value of time as I get older, and therefore think we can all save some of this valuable commodity by skipping past anger, bargaining and depression and moving to accept the bear! Grrrr…

Spotted in Marunouchi recently.

So what is it like living with a bear? Well, let’s take a look at some of the qualities of this charming beast: Historically bear markets occur every 3-5 years, and on average they last about a year. The S&P 500 typically falls around 33% during bear markets, although a third of these delightful periods have seen drops of over 40%. Bear markets typically end, and bull markets begin, when investor confidence is at a low point. In terms of character, although they may start with a crash, bear markets tend to be a slow grind down, peppered with the odd burst of optimism. Yes, bear market rallies are very much a thing, usually spurred by some piece of good news. However, the rallies are generally short-lived, and then the grind downwards resumes.

As you have probably already guessed, trading the bear is not as easy as you may think. Sure, we would all like to sell the top and then go to the beach, only to return to buy the beginning of the next bull run, but trying to do that can seriously damage your wealth if the market turns around quicker than expected. This is from a post of mine back in 2017:

In the years 1980 to 2015, the S&P 500 experienced an average intra-year decline of 14.2%. However, the market ended up achieving a positive return in 27 of those 36 years. That’s 75% of the time. You cannot afford to be sitting on the sidelines while this is happening. In fact, the opportunity cost of doing nothing will cost you far more than any of the corrections, bear markets, and flash crashes:

“From 1996 through 2015, the S&P 500 returned an average of 8.2% a year. But if you missed out on the top 10 trading days during those 20 years, your returns dwindled to just 4.5% a year. Can you believe it? Your returns would have been cut almost in half just by missing the 10 best trading days in 20 years! It gets worse! If you missed out on the top 20 trading days, your returns dropped from 8.2% a year to a paltry 2.1%. And if you missed out on the top 30 trading days? Your returns vanished into thin air, falling all the way to zero!” (from Unshakeable: Your Financial Freedom Playbook by Tony Robbins)

So how do you make the most of the slow grind downwards without trying to be too clever and missing out on the best trading days? First of all you need to stay calm. Bear markets are not the time for panic and dumping investments out of hand. If you are taking the time to read this blog you likely have a long term plan and there’s no need to deviate from that. Know your risk profile, stay diversified, and take this as an opportunity to accumulate assets at lower prices. Dollar cost averaging is your friend in the bear market. Rather than trying to catch the absolute bottom, keep investing little by little at regular intervals and build up your holdings at a nice average cost. Buy quality, buy what you believe in – this is not the time for speculation on penny stocks.

As to how this particular bear will play out, my thoughts, for what they are worth, are as follows:

The Ukraine situation is obviously a factor in inflation, but the main driver here is the Federal Reserve and other central banks.

Stocks in general, and tech stocks in particular, did well in the low interest rate environment during covid – lots of stimulus!

Now inflation is 8.3% and the Fed funds rate is 0.75%, and it’s a similar story elsewhere in developed markets ex-Japan.

The Fed has to close that gap – they will keep raising rates until they close it / inflation cools down, or until something breaks…

Means pain for stocks while this goes on – we could still go lower and there will be a plenty of volatility. I don’t see capitulation yet.

I think it will be later in the second half of the year before things start to look better – there are already signs that inflation is cooling off a little. We either get out of this because inflation eases off, allowing the Fed some breathing space, or something breaks and the Fed starts cutting rates again to head off the crisis.

How about crypto?

Crypto bear markets are a rare beast, in that they are programmed into the code of the leading crypto asset and arrive with the regularity of a Japanese train. If you don’t understand the Bitcoin 4 year halving cycle, you will constantly be bombarded with narratives to explain the pain, from the Mt Gox hack to the Quadriga scandal, to the Luna / UST debacle of late, there will always be a narrative to explain something that is actually pre-programmed. 2014 was a bear market, 2018 was a bear market, and so here we are in 2022. As with stocks, in crypto bear markets you accumulate quality. That means Bitcoin and Ethereum. Keep your hands off those alts unless you are really confident in their long term value proposition. Even then, prepare to be burned as the LUNAtics have been this week. Bad things happen to alts in bear markets… Bitcoin is down some 60% from its high so far this time around. Keep in mind that peak to trough 80% is the norm. BTC fell from $20,00 to around $3,000 in 2018. In the 2021 bull market it reached $69,000. If you have the nerve, now is the time to accumulate, and 2025 is the when the next bull market train comes along. Act accordingly and embrace the bear.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s been almost two months since my last post. Apologies for the silence but we have been busy at home with a new baby girl, born in early February! I must say that, despite the massive disruption caused by covid, working mostly at home has been a blessing this last couple of months. Some things really do only happen once or twice in a lifetime and it’s important to be present for them.

So I thought I would do a general roundup on things I have been thinking about during working hours, and how I am investing in this somewhat turbulent environment.

In my 2020 Investment Outlook post in December I wrote about having a view that guides your investment plan, and being prepared to change it if necessary. My focus for the year was on inflation and how Central Bank’s efforts to fight it would affect the investment environment. This, of course, has been somewhat overshadowed by the tragic events unfolding in Ukraine. I have no experience in international conflict, so little of value to add in terms of how things may play out there, but obviously we all hope that peace is restored as soon as possible.

The war has, of course, had a huge impact on the inflation narrative, as anyone who has visited a gas station recently will know. I actually accumulated a satellite holding in energy stocks during 2021 based on 2022 being a year of re-opening / reflation, with business getting back to normal, more travel, and therefore higher consumption of energy. It actually looks like energy prices could have some way to go, but I am out of those positions now and have rotated into tech stocks, which took a pretty good hit this quarter, and Japanese dividend stocks – largely inspired by @CacheThatCheque, who I interviewed in December. (that post is here)

My core holdings are unchanged, as they only require rebalancing once a year.

So what can we expect for the rest of the year? Well, the Federal Reserve went ahead and ended bond purchases on schedule, and then proceeded with a clearly telegraphed rate hike of .25% this month, and the market has reacted surprisingly favourably. It is said that stocks climb a wall or worry, and that’s exactly what they are doing at the moment. With more rate hikes to come I still expect plenty of volatility, but I don’t see any reason for big changes in allocation. Another dip in Q2 and a strong second half of the year is my working hypothesis.

Inflation means sitting in cash is a losing trade. Your spending power is being eroded day by day. And if you hold JPY cash, but are planning on spending the money in the US, for example, you are losing almost 8% per year and taking currency risk. However, investing overseas has been somewhat complicated by exactly that risk, as we have seen a sharp weakening of the yen – the Bank of Japan is by no means ready to taper and just announced they would purchase an unlimited amount of 10 year government bonds at 0.25%. If Japan is your home for the long term, I would estimate the real inflation rate, taking into account recent energy prices, at around 2% per year. This is why I think Japan dividend stocks are interesting as there are plenty of opportunities to earn more than 2% if you are willing to take a little risk. If you don’t have the time to research individual stocks, take a look at something like this Japan high dividend ETF:

As readers know, I also invest in crypto, and things have gotten interesting there again recently. A few weeks ago, Terra founder Do Kwon announced that they would be buying some $10 billion worth of Bitcoin to back their UST stablecoin over the coming weeks. And true to his word, Terra set about buying some $125,000,000 in BTC per day last week. If you are wondering if $125 mill per day is a lot, it is. And if you are wondering how you go about buying this much BTC, the answer is TWAP, or Time-Weighted Average Price strategy.

All this twapping appears to have been the catalyst for a rally in BTC to around $47,000, which is close to the year open price. L1 alts have also picked up significantly as a result.

One thing I am watching with interest is the Grayscale Bitcoin Trust (GBTC). The trust, which simply buys and holds BTC with a 2% p.a. custody fee is still trading at almost a 28% discount to the value of the assets it holds. At $30.8 bill in assets under management it is major contender for conversion to an ETF, if it receives approval from the US Securities and Exchange Commission. So GBTC, which can be bought through US brokerage accounts and retirement plans, offers the opportunity to invest in BTC at a 28% discount to current price, with a strong possibility that it will be converted to an ETF, whereby that discount will disappear. If you believe in BTC long term, it actually looks like a better buy than the asset itself. Obviously investing in crypto is high risk, but food for thought…

Best wishes to everyone. I hope you are enjoying the warmer weather and the cherry blossom!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Wow, year two of the great covid saga is almost over! It may not feel like it, but from an investment perspective, we are coming to the end of one of the easiest years in recent history. How is your portfolio doing? The odds are it’s looking pretty good so far. This has been the kind of market where we all look like pros.

So can we expect more of the same in 2022? You are probably already getting the feeling that it’s not going to be that simple, and that has a lot to do with Mr. Powell, pictured above. There are a lot of tough jobs in this world, but trying to fight inflation during a pandemic, without crashing a stock market that you inflated, certainly has the difficulty level set to Precarious. Volatility is coming back and you better have a plan to deal with it.

Stocks: So how well have stocks actually done? Well if you look at the indices, everything looks fine: The S&P 500 is up some 26% year to date, with the NASDAQ up 17%. Bull market! The picture gets somewhat muddled though when you realise that 45% of the components of the S&P 500 are below their 50 day moving average, and 65% of NASDAQ components are below their 200 day moving average. What does that mean? Well a big chunk of the US stock market is actually in bear market territory. What’s holding up the average is the massive outperformance of big tech: Apple, Alphabet (Google) Amazon, Meta (Facebook), Microsoft, and Netflix literally are the bull market!

All this has happened in an environment nourished by the steady drip of liquidity in the form of zero interest rates and quantitative easing from Jerome Powell’s Federal Reserve.

This from a recent Zerohedge post: “So I submit the notion of a raging bull market is a myth. Indices propelled to constant new highs by still flowing central bank liquidity increasingly held together by a few stocks.”

No wonder things got choppy around the time of the FOMC meeting this week…

Bonds: The problem here is, of course, the emergence of inflation, which the Fed originally tried to write off as “transitory”, but have now decided they need to act on. That means no more drip drip, and interest rates must rise. Inflation is not good news for bonds, as it eats away at the purchasing power of the bond’s future cash flows. Why buy today’s issue when tomorrow’s will come with a higher yield? Bond yields go up = bond prices go down.

Commodities: Assuming inflation is here to stay for a while, what should go up is the price of “stuff”. There’s a reason for that 5% of your portfolio that’s been sitting in gold doing not very much all year. Just be aware that if there’s a panic à la March 2020, everything gets sold off initially, including the shiny metals. Oil is going to continue to be interesting next year if the scourge of Omicron doesn’t crush the reopening trade…

Crypto: It’s been one year since my Bitcoin: It’s About to get Loud post. Yes, I am now patting myself on the back for calling the most obvious bull market of all – the one that comes every four years! Crypto is never easy though, especially for newcomers. We have seen (I think) seven or maybe eight pullbacks of over 30% this year alone. We have been to an all time high of $69k and are now back at $46k with the fear and greed index indicating extreme fear. Meanwhile on Layer 1, Ethereum has outperformed Bitcoin and Avalanche and Solana have done crazy multiples. (ETH up about 420%, AVAX up 3,000%, SOL up 11,000%!) Have we seen the top of the mountain and we are already on the way down the other side, or is there one final push to the summit to come?

Dude, you mentioned having a plan?

A client of mine, who is a former economist once said to me: “Right or wrong, I always saw it as my job to have an opinion.” That comment has stuck with me, as I think it applies to all investors. You can’t always be right, but you should have a view, test it rigorously, and be prepared to change it if you find evidence you are wrong. So for what it’s worth, here’s my view for 2022:

The Fed, and other Central Banks are being forced to deal with inflation, but they have openly admitted that they are equally, if not more concerned, with not crashing the stock market. The words “rock” and “hard place” spring immediately to mind. So they taper now and plan to stop bond purchases by March. The market does not like this and corrects strongly, which basically means that those big tech stocks sell off dramatically. Then, central banks have to backtrack and slow or end the taper, and maybe rethink those rate hikes planned for later in the year. When the drip is turned back on, the market bounces back.

You get the idea.

How you plan for this depends on your investing style:

If you have a diversified asset allocation and your plan is to do nothing at all and ride it out, maybe continue dollar cost averaging every month: Congratulations! You are dismissed from class and free to go and play!

If you are not one of these people then please take note – staying sane is actually an option here. However, if you insist on trying to trade this, it is probably past time to start getting a little more defensive and raise some cash to deploy when things get rough. I would, however, be tempted to entertain the possibility that Omicron is also a little roller coaster like by nature, and the initial whoosh into the sky will return to earth equally quickly. This could precede the discovery in late Q1 that inflation actually was somewhat transitory, and caused mainly by supply chain disruption, and therefore the need to deal with it falls away. So be cautious, but it’s perhaps not time to lock yourself in the bunker.

Is the crypto bull market over? Crypto is more correlated to stocks than many crypto people like to think, so if anything is going to slay the bull it could be a dramatic stock market correction. That said, the level of adoption, or network effect, has increased significantly this year, and includes a good deal of institutional money. If your plan, like mine, was to sell the cycle top at $100k+ and then buy back in the bear market, it may be time for re-evaluation. I’m slowly becoming more open to the idea that the four year cycle could be smoothing out and, despite frequent mini crashes, we may not see a 2017 style blow off top followed by a grinding two year bear market. Don’t hold me to that, but a simple way to play it is to have a cold storage allocation that you hold longer term, and a tradable allocation that you look to sell at Extreme Greed and buy back at Extreme Fear, rinse and repeat.

However things play out, it is unlikely to be smooth sailing. So I wish you a peaceful holiday season. Here’s hoping Japan does a better job of holding off Omicron than my home country is doing so far…

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.