One down, one to go. With the FOMC resulting in a dovish cut, we now await the BOJ meeting next week. So, how are things shaping up for the end of the year and 2026?

The Fed delivered the expected 0.25% rate cut. It was accompanied by cautious commentary on next year, without really turning hawkish. Pretty much a goldilocks result for markets. Stocks rallied into the close, while Bitcoin pumped to $94k before quickly retracing. The Fed’s dot plot and 2026 outlook seem wildly irrelevant given where things are going after Powell’s term ends.

BREAKING: President Trump is asked if the new Fed Chair will be expected to "lower interest rates immediately."

Does anybody need that stated more clearly? The next Fed chair will be appointed by Trump and will do his bidding. Their primary function will be to cut interest rates. End of story.

Leaping into the future, it will be fascinating to see if a post-Trump Democrat administration will work to reinstate the Fed’s “independence”. I bet you they won’t…

Anyway, I digress. The US is moving toward financial repression in 2026. Inflation allowed to run hot, and interest rates forced lower = Negative real rates. Negative real rates are a stealth tax on savers. It’s how the government reduces the debt burden.

It’s not good. But it’s what is going to happen.

Americans who own assets will be fine. Those who don’t will struggle.

Lots of liquidity, equities up, hard assets up, and a weaker dollar.

So, Bitcoin to the moon, right?

Hmmm, given what I wrote above, we are looking at the perfect environment for Bitcoin. The macro gurus, who are relatively new to Bitcoin, are declaring the 4-year cycle dead and preparing for new all-time highs in 2026. Except that’s not what usually happens. October marked a picture-perfect 4-year cycle top. It doesn’t get any clearer. The bottom should be around Oct/Nov next year.

I’m long BTC and happy to be proven wrong, but I think there is pain to come. I think we will see $40-50k, and buying Bitcoin when stocks are pumping will seem like the dumbest thing a person could ever do with their money. Sentiment needs to be broken before we run again.

And yes, I will buy at those levels. Until then, there isn’t much point in thinking too hard about it.

As for stocks…

The midterm general election is in November. Sometimes the most obvious outcome is the correct one.

Is the BOJ going to spoil the party?

The BOJ is signalling a hike. It’s been reported in the Nikkei. It’s pretty much baked in and would be more of a surprise if it didn’t happen. I don’t think it’s going to shock markets. It might strengthen the yen a little, but it probably won’t be earth-shattering. See my post on the Yen Carry Trade from last week.

Japan, of course, is already at negative real rates. That should support the Japan equity bull market. It only sucks if you don’t own stocks…

I have the flu. That’s as much brain power as I have this morning. Time for a lie down.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It looks like the Bank of Japan (BOJ) is finally ready to raise rates again this month. So, right on cue, out come the doomers to ring the alarm on how the unwinding of the yen carry trade is going to blow up global financial markets.

Should we be worried? How could a potential unwind of this trade affect investors in Japan?

What is the yen carry trade?

The core idea behind this trade is to borrow money in a low-interest currency (JPY) and invest it in higher-yielding assets elsewhere.

For example, a fund could borrow yen at less than 1% interest, invest in US Treasuries earning 3.5%, and pocket the difference. This works perfectly until exchange rates make a big move. Then things can get interesting.

A conservative estimate puts the size of the carry trade at around $1 trillion, based on Japanese banks’ foreign lending. Some estimates use the notional value of FX swaps and forwards using the yen to reach a figure closer to $14 trillion.

Of course, hedge funds are not necessarily just buying conservative US government bonds on this trade. A mountain of cheap yen is converted to dollars and other currencies and flows into all kinds of assets. A deep dive would likely reveal that a large portion of this trade has gone right into the red-hot Magnificent 7 stocks.

Why Japan?

The carry trade can take place using any currency with a low interest rate. Japan has been the primary go-to market due to its unique characteristics:

The lost decades following the bursting of the bubble in the early 90s

Deflation and slow growth

The BOJ’s long-term low/negative interest rate policy

Hence, the yen became the world’s cheapest funding currency

How the carry trade makes (and loses) money

This trade works based on the interest rate differential – the carry. With a stable or weakening yen, it will remain profitable. In this type of environment, it’s hard to miss.

Problems occur if the yen strengthens. If an institution borrowed yen at ¥150 to the dollar but later the yen strengthens to ¥130, it suddenly requires more dollars to repay the same yen loan.

The unwind then happens as follows:

Sell the dollar asset (treasuries/stocks, etc.)

Convert to yen

Repay the yen loan

This unwind puts downward pressure on the asset being sold, which could be US treasuries or global stocks. And the flood of capital back into JPY accelerates the yen’s strengthening. A relatively small move in exchange rates can snowball into something much larger.

Famous unwind events include the 1998 Asian financial crisis and the 2008 global financial crisis. In 2024, we saw a mini unwind as the BOJ shifted policy.

Why does it matter to everyday investors, especially in Japan?

With the US central bank cutting rates and the BOJ looking to raise rates, there is a real possibility that the yen will strengthen in the short term. Most Japan residents will be relieved as foreign goods and overseas trips will become more affordable.

However, the unwind can suck out global liquidity and do some real short-term damage to our investments. Not many risk assets fare well in this kind of event, so be prepared for international stocks, Japanese stocks, high-yield bonds and crypto to take a beating. Japanese exporters, such as Toyota, are particularly sensitive as a stronger yen erodes their overseas profits.

So, are the doomers right this time?

Beware of people claiming that the yen will suddenly surge and stocks will crash overnight. The reality is:

Yen carry trade unwinds tend to happen in bursts, and not always in a straight line

Central banks will often intervene, verbally or via policy tools.

Markets tend to pre-position before the worst moves happen

You can already see this pre-positioning happening. The yen has strengthened over the last few days after the BOJ hinted at action at its next meeting. Note how BOJ governor Ueda is trying to communicate his thoughts in advance and avoid a “shock rate hike” a la August 2024.

People writing epic threads on X tend to overstate the timeline risks. Sharp moves can indeed happen. However, it doesn’t necessarily guarantee an imminent crash.

Should we be worried?

Concern about the carry trade unwind is most rational if you have:

Investments heavily exposed to foreign currencies

A portfolio dominated by global stocks

Income linked to export-driven Japanese companies

There is less to worry about if you have:

Mostly yen-denominated assets

A long time horizon

No plans to move money internationally soon

Concerns about a carry trade unwind are certainly not irrational. However, the real risk lies less in timing the event and more in understanding how currency moves can affect your portfolio and positioning accordingly.

So it really comes down to portfolio structure. Trying to predict macro events is insanely hard…

Ok, then how do I hedge against this?

Of course, some assets will benefit from a carry trade unwind:

The yen, of course, is the obvious winner – that trip abroad could get a lot cheaper next year!

Gold is historically a beneficiary of unwinds as investors deleverage and seek out safe havens. If the yen is rising, the dollar is usually falling, which is generally good for gold.

Long-duration government bonds generally do well as the world goes risk-off and money flows into the safest assets. Bond prices go up as yields go down.

In conclusion, don’t let the doomers scare you out of long-term investments, but be prepared for some volatility. Keep an eye on central bank rate decisions, the corresponding US-Japan interest rate gap, USD/JPY exchange rate and global risk sentiment.

Personally, I am long-term bearish on the yen, but in the short term, anything can happen.

It’s always good to keep some dry powder to pick up risk assets while investors run scared.

And make sure your passport is still valid for that overseas trip you’ve been planning!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Markets are not looking so hot right now. I really hate to be bearish, but it’s becoming unavoidable.

Last week, Bitcoin made its first daily close below $100,000 in 188 days. Then yesterday it closed below the 50-day moving average on the weekly chart. This is always bad news for bulls. Some of the people who were telling us the 4-year cycle is over are still holding out for a reversal, but they are probably grasping at straws.

We are so done. Thank you for playing.

I know it’s unlike me to be so negative, but when a situation changes, it’s important to confront reality quickly. Crypto is heading into a bear market, and it’s right on schedule.

Initially, Bitcoin is acting as the pressure release valve as investors lose faith in an overheated risk environment. You will note how, over the last week or so, Bitcoin is lower when you wake up. Asia propped up the price in the daytime, and then America sold hard while we slept. Now Asia is selling, too.

Worse still, BTC tends to lead equities, and in my humble opinion, BTC is heading lower.

Stocks are already wobbling. In particular, the AI trade is coming under increased scrutiny. Nvidia earnings are due on Wednesday. I don’t think there are numbers big enough to satisfy the masses this time, although the numbers will likely be impressive regardless.

Burry put on his Nvidia/Palantir short and then closed his fund. Now he doesn’t have to worry about investors trying to pull their money when the market moves against him. People are debating whether he is actually any good at calling this stuff, which is a valid question. It’s such an obvious trade that you wonder if it can really be that simple, especially with Trump there to pump the markets every time they stumble.

But it doesn’t look great to me. In the short term, at least, I’m siding with the bears.

Time preference is key

It’s ok to be bearish, but the big question is: over what timeframe?

BTC is a good starting point for this discussion, as it is highly sensitive to both global liquidity and overall risk sentiment.

When Bitcoin topped in November 2021, it was just as the Federal Reserve pivoted to begin a brutal tightening regime. Interestingly enough, in November 2025, the Fed is going in the opposite direction. In fact, the market was pricing in a further rate cut in December until the US government shutdown delayed the data and muddied the waters. Uncertainty around rates is a huge factor in sparking the sudden loss of appetite for risk.

The liquidity picture for 2026 actually looks pretty rosy. Trump is effectively going to gain control over the Fed, and he has the midterm elections to pump the market for. On the flip side of that lies a slowing US economy.

Bitcoin’s level of institutional adoption was meagre in 2021/2022. In fact, it turned out the industry was on the brink of collapse. And collapse it did: Terra/Luna, Celsius, Blockfi, 3AC, and, of course, FTX all fell during the bear market.

The picture is very different now. US Bitcoin ETFs have almost $120 billion in assets under management. $72 billion of that is in BlackRock’s IBIT alone. What’s more, the Trump administration is pro-crypto. This is not an industry on the brink of collapse any more. It’s just going to need to take a breather for a while.

Plan for the worst

The typical bear market drawdown from the peak for Bitcoin is 80%. So, worst case, we are going back to $25,000. Ouch! Not pleasant at all, but I would not bet against this outcome.

If ETFs and institutional adoption, plus a favourable liquidity cycle count for anything, which I think they do, we may not go that low. Personally, I’m not really interested in bidding $90k. I’ll get interested at lower levels. $50k seems a bit more like it. (this is my finger in the air, best guess if you are wondering how I got this number)

Here’s a little perspective:

What about stocks?

Nvidia’s P/E ratio is around 53. Investors are willing to pay that amount for each dollar of the company’s earnings. I probably don’t need to tell you that future earnings expectations are a little on the high side. The Magnificent 7’s average P/E ratio is around 28 to 35. Those expectations may well be due for a sharp adjustment.

The other 493 stocks in the S&P 500 are not looking so bad, although they could get dragged down somewhat in a Mag 7 correction.

Global stocks, Japan included, are unlikely to emerge unscathed, but we could well be looking at an interesting buying opportunity.

Personally, I kind of like the idea of reducing US exposure (particularly Mag 7) and increasing Japan. The only problem is then you get trapped in yen. Finance Minister Katayama is making the usual concerned noises about exchange rates, while taking absolutely no action to counter the yen’s decline. Real interest rates in Japan remain negative, and as long as they persist, the currency will continue to struggle.

Negative real rates are a boon for stocks, though. If rates somehow ever turn positive, it’s time to rethink.

All in all, it comes down to where you are in the financial planning process. I covered this in the Burry post, but here it is again in simpler form.

I see three key stages in the personal finance journey:

Accumulation – spend less than you earn and invest the difference into stocks and other high-growth assets. If asset prices decline, don’t panic and keep buying. In fact, buy more if you can.

Diversification – a mix of protecting capital, whilst continuing to accumulate. The key to knowing when to diversify comes down to three factors:

a) The data tells you – you hit your number and simply don’t need as much risk any more

b) You become conscious of the amount of money you have at risk and start thinking about what to do

c) Asset prices are considerably higher than the average price you paid when accumulating. Despite the wobbles, we are still in this zone for anyone who has been accumulating for a while. It may not last much longer, however…

3. Distribution – you begin living off the income generated from your accumulated assets, or simply spending the money

If you are in stage 1 or 3 and are properly allocated, a stock market correction should not bother you too much. If you are at stage 2 but have not diversified yet, the current window of opportunity may be about to close for a while. Don’t panic, but perhaps give it some thought.

Personally, I have been selling stocks that have done well over the short term, particularly tech/semi/AI-related stuff. A few Japanese tech stocks I owned got a big boost when PM Takaichi was elected and are probably due for a reality check.

In other business

My next casual meetup, billed as the Nikkei ¥50,000 party, is on 26 November from 7pm at Hobgoblin Roppongi. Everyone is welcome. You don’t have to talk about investing, and you don’t have to drink unless you want to. Some of us may need to!

Before you ask, yes, the event will go ahead even if the Nikkei is below ¥50,000. That is an achievement unlocked, and I’m sure we’ll be back above that level in due course.

Don’t get too bearish!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s been another interesting week. ‘Big Short’ legend Michael Burry returned to X to call out the AI bubble, posting charts that question whether the ongoing mega AI capex boom really matches demand. Burry pops up every now and then to predict disaster, and his hit rate post-2008 is not all that spectacular. However, he followed up by filing his investment firm’s 13F 11 days early, showing that he is short 1 million Nvidia shares and 5 million Palantir shares.

Money where his mouth is.

The market took notice and US tech stocks tumbled on 4 November. Japanese stocks followed suit, with Softbank Group dumping almost -17% over 2 days. This comes at a time when the US government shutdown is blocking the liquidity faucet and tightening things up considerably.

Crypto didn’t like it either, but hey…

Predictably, President Trump issued some positive comments about stocks and Bitcoin overnight, and the situation calmed down. Every time I think this market is ready to begin its descent into hell, I’m reminded that the guy in charge of America has a vested interest in keeping it above ground…

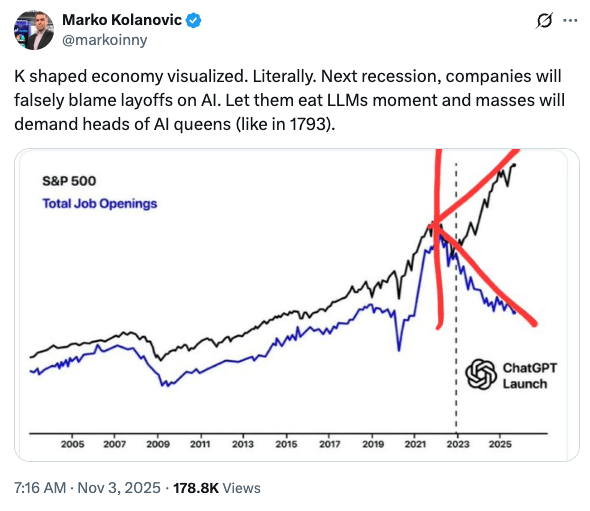

Clearly, Burry is hitting a nerve with AI bubble enjoyers. Here’s a great thread from Marko Bjegovic covering why he is probably correct.

The ‘K-shaped’ economy

You are probably hearing this term lately. The K-shape represents the latest expression of wealth inequality. Essentially, high earners and large corporations are getting richer as asset prices rise, while low-income households and small businesses, the lower leg of the K, are struggling to get by.

High-end products are selling, while companies like Chipotle are finding their customers poorer and less inclined to visit.

Here’s another way of looking at the K-shape, from a different Marko:

Speaking of liquidity and the AI bubble, Ray Dalio just posted about how the Fed is stimulating at an odd time. I’m not sure the Fed is really beginning QE, as he says, but it is certainly ending QT, cutting rates and taking an expansionary stance. This is something it would generally do when the economy is in trouble. Instead, the backdrop for the Fed’s easing is high asset valuations, a relatively strong economy, inflation above target and abundant credit. Not to mention a bubble in AI-related stocks – the elephant in the room, so to speak.

The Trump administration is taking a bold and probably reckless bet on growth, and particularly AI growth. What could go wrong???

Time to take profit?

We’ve been talking about a melt-up before a melt-down, but that’s by no means guaranteed, and we’ve already melted up a lot.

Stock investors, belonging to the top leg of the K, have done very well, but are now faced with a choice: remain invested and ride through the bubble or protect capital. As Michael Burry experienced in 2008, bubbles can keep inflating and punishing shorts for a long time before they finally pop. Younger investors can probably handle the drawdown, provided they are disciplined enough not to sell the bust. We all know the drill when panic hits: as the last desperate few capitulate, central banks will cut rates, stimulate, and markets will surge back over the next 12-18 months.

People who are getting closer to spending their investment money should probably think more carefully. There may not be a better opportunity to take risk off the table and diversify for some time. Nobody ever went broke taking profit, especially around all-time highs.

For people in between, US treasuries are holding up as a safe haven as well as anything else at this time. Spreading some of the risk also serves an often overlooked purpose: offering the opportunity to rebalance and buy the bottom in stocks if we do suffer a crash. I stand by my belief that anyone with a meaningful amount of money should be well diversified at a time like this.

The stock market is not the economy

Here in Japan, we are enjoying the Nikkei holding above the ¥50,000 mark. That doesn’t mean we escaped the K-shaped economy. In a rare quiet moment the other evening, I was thinking about Japan’s economy and why interest rates don’t seem to go up much. Aside from the rich asset holders, many people are struggling. Wages still lag inflation. 5kg of rice is almost ¥5,000. The lower/middle classes do not have a lot of money to spend.

Fewer people spending money is bad for the economy. The general expectation seems to be that interest rates will rise gradually. They certainly won’t rise quickly. Higher rates would mean higher interest payments on government debt. PM Takaichi is focused on growth, not inflation.

Should we really expect a meaningful rise in interest rates? I simply can’t see it.

If rates can’t rise, then the yen remains weak, prices increase, stocks and Tokyo property appreciate, and low-income families continue to struggle.

If all this is true, then what’s the trade?

Own dollars, own financial assets, own hard assets, and be kind…

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Our family just came back from a weekend break, which was my treat in celebration of our stellar investment returns. Note: don’t tell your significant other how well your portfolio is doing unless you are prepared to spread some of the winning around! We had barely been back home for 5 minutes when the doorbell rang and a new pair of boots was delivered. She bought those herself, so no complaints from me, but you can see how this goes.

Even the stock market is enjoying a little retail therapy.

In case you’re not familiar with the term, retail in this case means individual investors: regular people, you and me. One theory is that covid is behind this surge in retail-driven performance. Stuck at home with their stimmy checks, regular investors learned to buy the dip, and it’s been working for them ever since. Stocks, crypto, gold – whatever retail jumps on goes up. Institutional investors look on in bewilderment, stuck with their risk models flashing warnings as the market leaves them in the dust.

It may not be healthy, but these are the cards we’ve been dealt. And with the Fed expected to cut a couple more times this year while simultaneously ending its balance sheet runoff, it’s hard to find a compelling reason to ease off the gas. Trump has even been talking about handing out money from tariff proceeds to the public. Can you imagine?

It would be rude not to do this! I’m looking at late November, maybe 26th, 27th or 28th. I’m open to suggestions on the venue, but my basic rule is that it must be a cash bar, so we don’t have to worry about whether everyone turns up to cover costs or fiddle around sorting out the bill. What do you say? If you don’t live in Tokyo and have been thinking of taking a trip, well…

Send me a message, email, DM or whatever if you want to come along. Will mostly plan this on X, so keep an eye on this thread.

We’ve been talking about an end-of-year melt-up for a few weeks now. So far, so good. I noticed the Nikkei Asia already started talking down the likelihood of a BOJ rate hike later this week. You can pretty much take that to the bank, right?

Is the Bitcoin 4-year cycle over?

After the most vicious deleveraging event ever just a couple of weeks ago, the crypto market has recovered. Yes, retail bought the dip once more!

There has been a wave of speculation over whether the 4-year cycle is still intact. It’s fascinating, actually, as crypto-natives have been hyper-trained on this narrative. It’s probably the reason Bitcoin is not significantly higher right now. Long-term holders have been unloading, while retail ETF buyers continue to accumulate. Many of the new investors have no idea what the 4-year cycle is and just have a monthly allocation set up for their account.

Felix is awesome, and I love his Forward Guidance Podcast, but time will tell. 2013, 2017 and 2021 were all followed by a nasty bear market. Yes, Bitcoin wasn’t a macro asset like it is now. Yes, you can make a great case that liquidity is rising, and the boomer ETF buyers will keep buying. I really want to believe, you know! But let’s just say I’m ready for anything. Warren Buffett hates crypto, but his quote about finding out who’s been swimming naked when the tide goes out could have been written for the industry. All we need is one good leverage flush to start the dominoes falling, and we all get a chance to buy at $50k again. Don’t think it can’t happen.

At least it will give these guys something to chirp about.

These guys are great! They’ve done zero work, but they will gladly tell you how Bitcoin is too volatile to be investable.

Well, BTC has closed above $100,000 for 172 consecutive days now. If you wanted to sell, you have had plenty of time to do so. If 2026 is a bear market, make sure you ignore these nitwits on their victory lap and back up the truck.

Melt-up before the melt-down, though, right? I’m yet to see real euphoria in crypto this year. Remember the images of people lined up on the street to buy gold a week or so ago? That’s what we’re looking for. We’re not there yet.

It’s a busy week with the Fed meeting, BOJ and Trump on the loose in Asia. I don’t know when the next dip will come, but you can bet that retail will be ready to buy it!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

As you may know, I have worked as an independent financial adviser for many years. I first got involved in this business in 2002, and the world has changed drastically since then. Some of the financial products that were popular at that time are almost obsolete now. So, is offshore investing over? Or is it still something worth considering for the right person?

A note here: I have never used this blog to promote offshore products, and that is not my intent here. However, I’m probably as qualified as anyone to discuss this topic, so here we go!

Much has changed

In 2002, if you were an expat in Japan, earning good money and looking for a way to invest, your options were fairly limited. Opening an investment account in Japan was not something many people considered. Along with the obvious language barrier when it came to reading product information, opening an account would involve meeting with a broker from a Japanese securities company and going through their sales process. If you think offshore advisers had a bad reputation, local securities company salesmen were not much better – they were well known for heartily recommending whatever was booming at the time and throwing their clients in at the chuffing top of the market.

Therefore, speaking to a British guy in a suit and cufflinks and investing in the Isle of Man was usually a more palatable option. Of course, these guys operated on commission, and some of them did not have your best interests at heart. Buyer beware! Many people got duped into long-term savings plans they didn’t understand.

To be fair, some of these people partly deserved what they got. All these offshore products had terms and conditions readily available in English. You just had to get a copy and read them! Plenty of people managed to ask questions, read the documents and invest in a product that they actually understood.

These days, investing in Japan could not be simpler. Go online, choose a brokerage, fill in the initial online form (with your name in half-width katakana hahahahahaha!) and then post off copies of your residence card/My Number card. You can have a brokerage account and a tax-free NISA set up in a couple of weeks.

So, is offshore investing dead?

Other advisers may have different mileage, but from my perspective, the demand for offshore products is certainly down significantly. I attribute this to two factors: getting a low-cost brokerage account is very easy, and nobody wants to pay for anything these days.

Not that avoiding high fees on investments is a bad thing. It’s one of the simplest things you can do to improve your returns. However, when offshore advisory is done well, you are not necessarily paying a lot for the product. Lump sum investment products in particular have very flexible fee structures, and a good adviser will be reducing their initial commission and taking an annual management fee for servicing you and providing ongoing advice.

Of course, much depends on your country of origin, how long you plan to spend in Japan and where you will go next. Offshore isn’t a great fit for everyone. (Americans in particular, take note. NISA isn’t necessarily a great fit for you either, and you are likely better off getting US-specific advice and investing in US-based accounts.)

Here’s a simplified view of how I see the steps to allocate money:

Make sure you have an emergency cash reserve

Fill up anything tax advantaged first – in Japan, that would be NISA, iDeCo

Any money over and above that is up for consideration – it could be invested in a taxable Japan brokerage account, an international brokerage account like Interactive Brokers, or offshore.

Again, a lot depends on nationality and personal situation, so no advice here, but some of the benefits of offshore get overlooked in the relentless pursuit of low fees.

I will leave the offshore regular savings plans out of this, as they are somewhat outdated. But many people, including myself, still have plans set up years ago, and that’s fine.

The offshore portfolio bond is for larger lump sum investments. It’s essentially an insurance structure; the individual owns the policy, and the policy owns the assets. It is open architecture so policyholders can access ETFs, mutual funds and individual stocks. For Japan residents, you are not required to report capital gains and dividends within these policies as they occur. You report when you exit the policy and pay a one-time tax payment (一時所得) of around 20% of gains. E.g. You invest $100k and the policy grows to $200k – you cash out the policy and owe approximately $20k.

So you effectively get gross roll-up inside the policy. You can switch investments and take profits as much as you like without triggering a taxable event. For some people, that alone is worth the fees.

If you leave Japan, you just take it with you, and when you cash out, you may end up owing nothing here. Of course, some people may have to factor in the exit tax and the lookback, etc. It depends on amounts and timeframes.

Use of trusts

The other thing you can do with offshore insurance products is put them in a trust. Trusts can be very effective for estate planning, particularly for, but not limited to, British nationals.

In the case of Isle of Man assets, probate will be required on the death of the last policyholder before proceeds can be paid out of the plan. Placing the policy in trust avoids this lengthy and often frustrating process, allowing money to be paid out quickly to the beneficiaries.

Trusts allow the donor to maintain a degree of control over the assets and, in some cases, to have limited access to the capital. A discretionary trust, for example, can instruct the trustees to hold the assets until the beneficiaries reach a certain age before distributing the proceeds to them.

For individuals who are treated as UK long-term residents, a trust is an effective way to shield assets from UK inheritance tax. Trusts are also worth considering for anyone who plans to become a UK long-term resident in the future.

A note here: trusts will not help you to mitigate Japanese inheritance tax. Japanese tax authorities do not recognise foreign trusts and generally look through them and tax the assets. If Japanese inheritance tax is a concern, you should first do your own reading and then discuss with a local tax professional before taking action. Reddit is an incredible resource, but you should not be taking personal tax advice from there.

If you have an offshore policy that you have been holding onto and perhaps do not know what to do with, it could be worth discussing with your adviser as to whether it would be better to put it into a trust. If you have lost contact with your advisor, you are welcome to contact me. I can also assist with general advice on whether it is better to keep the policy or cash it in and invest elsewhere.

In conclusion

Offshore investing is generally less relevant than it used to be. However, it is far from dead. In particular, high-net-worth individuals may find there are significant benefits to investing in a tax-free jurisdiction, and/or taking assets out of their own name.

For simple day-to-day investing for longer-term Japanese residents, NISA and iDeCo are incredibly hard to beat, and local brokerage accounts provide access to a wide range of assets. We are really spoiled these days. If you need help getting things organised, don’t forget that I offer fee-based personal finance coaching!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I woke up last Saturday morning and, as is my habit, checked on the overnight market movements. I did a double-take and wondered what the hell had happened. Bitcoin, perhaps the nimblest indicator of global risk appetite, had dumped heavily. Several possible scenarios ran through my mind, but I knew it could only mean one thing…

Donald Trump has posted something!

Bingo! After market hours on a Friday, America’s fearless leader had somehow mangled a Chinese announcement on rare earth exports and sent out a post threatening further 100% tariffs on China. After all the TACO earlier this year, I had forgotten about the trade war!

Had stock markets been open, they would not have liked it at all. As they were closed, crypto bore the brunt, and anyone unfortunate enough to be awake got to witness the biggest liquidation cascade of all time. Bitcoin fell to around $104,000 initially before bouncing. Alts were nuked without mercy, with $ATOM token getting as close to zero as you can really get without going negative.

Something in the range of $18.7 billion in positions got liquidated in a matter of minutes, and around $560 billion was wiped from the total crypto market cap. Fun times!

I won’t get into the whole conspiracy theory of what happened. Suffice to say, a very large and very suspicious short position appeared in the market shortly before the fun began. This seems to be the only person who made money that day. It could be a coincidence, of course. I guess we will never know…

Japan is moving to ban insider trading in crypto, by the way. Seems like a good call.

Bitcoin hodlers would be a little concerned to see the price fall so quickly, but most take it in their stride. Leveraged traders, however, some of whom don’t even own Bitcoin, did not make out so well. Many got a lesson in risk management they will never forget.

Of course, by the US open on Monday morning, Trump had already straightened things out, and stocks acted like nothing had ever happened.

It’s always the leverage

Most people should stay away from leverage. Hell, even skilled traders should handle it with care. And yet, Volatility Shares just filed for a total of 27 leveraged 3x and 5x single asset ETFs. If approved, every Robinhooder will be able to go 5x long Nvidia, Palantir, XRP and more. What could possibly go wrong?

Wall of worry

We’re so back! Add to this the growing concern over the AI-driven boom and whether it is, in fact, a bubble, and you have to wonder if the Q4 melt-up might be cancelled.

The AI bubble talk is understandable. OpenAI has around $1.5 trillion in AI build-out plans. This for an unprofitable company with only $13 billion in annual revenue. Both smart money and dumb money alike are positioned for a bullish Q4. Tech stocks sure have a long way to fall if investors lose their nerve.

A week or two ago, the CEO of Goldman Sachs warned that a stock market correction could occur in the next 12-24 months. Thanks for the deep insight, bro! Jamie Dimon is talking about gold possibly going to $5,000 or even $10,000.

Throw in the US government’s shutdown, and you may wonder how stocks can possibly rise further. Surely the Bitcoin bull run is over, too?

While Trump was busy TACOing, Jerome Powell came out on Tuesday and said that “the downside risks to employment appear to have risen.” That appears to imply a further rate cut at the Fed’s end-of-month meeting. More importantly, JPow signalled the end of the Fed’s balance sheet runoff. If quantitative tightening is really over and liquidity flows, the wall of worry could melt rapidly.

I don’t know what’s going to happen, and you certainly shouldn’t be making investment decisions based on my offhand opinions, but if we get a strong earnings season, I still see a bullish Q4 and then trouble on the horizon in 2026. It’s never dull, is it?

Yes, Prime Minister

Organising a Prime Minister seems to be a tough gig these days. France had a guy quit and then get reappointed in the same week! Here in Japan, Sanae Takaichi went from being a done deal to less than Liz Truss in a couple of days. Now the LDP is courting the opposition, and it’s looking like they might find the votes to anoint the country’s first female Prime Minister after all. Who knows?

The market has already tipped its hand if the deal gets done. JP stocks up and yen down. I will unapologetically cheer for our iron lady just because I want my Nikkei ¥50,000 party. The yen is cooked anyway.

A diversified portfolio matched to your base currency and risk profile with satellite holdings in debasement assets.

I sound like a broken record, don’t I? By the way, I found a Japan Physical Palladium ETF (1543). It’s amazing what is available these days. Don’t do anything I wouldn’t do!

Thank you for your attention to this matter.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

You can’t time the market. Except those times when you can. Last week, I wrote a post called Melt Up? Maybe I got lucky, but the meltup began right after and is now in full swing. Gold, Bitcoin and of course, Japanese stocks.

Not that I’m claiming clairvoyance here. I had no idea how the market would react to the LDP leadership vote. Generally, I discount politics as it has far less effect on asset prices than people think. At first, I thought the market reaction was relief that the younger, less experienced guy didn’t get in, but clearly it’s not that. It’s all about the new leader.

I won’t delve into political analysis. I don’t have any edge here. Takaichi’s economic stance is perceived as expansionary, and there seems to be an expectation that she will go full Abenomics on us. That remains to be seen, but here are a few observations:

Taro Aso was clearly instrumental in getting Takaichi elected and will be a key figure in the administration. He opposes ‘modern monetary theory’ and argues for fiscal discipline. Watch the yen over the coming months to find out who is really in charge.

When Abenomics was implemented, USD/JPY was at 80 and inflation was negative. Now we have the dollar at 152 and 3% inflation. It’s a very different world. You can’t just cut rates to zero and reimplement QE without inflation blazing out of control.

The BOJ may not be entirely free from political interference, but it will make its own decisions. It may or may not hike at the next meeting, but it’s not going to go the other way any time soon. No doubt, Chairman Ueda’s job just got a little more complicated, though.

I’ll stop there. Prime Ministers don’t seem to last very long these days, so we should probably give it 6 months or so before expecting a clear indication of where this will land. For now, you can probably give up on any hopes of a stronger yen. And you’d better own stocks and hard assets.

The meltup continues. I joked about having a Nikkei ¥50,000 party on X, but I think we should do it. It may be soon, so get ready!

Running it hot

If you are seeing posts and mentions about the ‘debasement trade’, it’s no wonder.

I’ve been harping on about monetary debasement for some time. People seem to be getting the idea. I’m seeing more and more people who don’t own gold capitulating and buying it at all-time highs. They should have owned it earlier, but that doesn’t make them wrong for getting some now.

Reminder: if you run a diversified portfolio, you will already have a 5-10% allocation to gold. You don’t have to play catch-up. People who only own stocks are learning this now.

It’s clearly a sign that people’s portfolios are at all-time highs. We should probably be a little careful about getting too greedy, but it’s a wonderful time to consider how to get joy out of the money we have worked for and taken risk to grow.

I ordered the orange iPhone. It’s due to be delivered in early November. I wasn’t planning on becoming a walking top signal, but maybe I’m about to…

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s a slow week for stocks in Japan, with the market losing ground in part due to the selling of names that went ex-dividend on 29 September, and also out of concern over a possible US government shutdown.

29 September was the cut-off date to receive the next dividend for many Japanese stocks. Prices are often driven up before the ex-dividend date, only to fall after it has passed as investors sell, safe in the knowledge that the next dividend payment will be delivered. It’s really a non-event for long-term holders.

A US government shutdown could lead to a delay in the release of key economic indicators such as jobs data. How can we possibly know when to panic sell our stonks if we don’t know how many jobs were added/lost last month in the USA?

Despite the relative gloom, the focus for Q4 is increasingly on a potential melt-up for markets as liquidity continues to flow. Tech stock valuations are admittedly high compared to the 20-year average. However, compared to the last 5 years, the premium is significantly lower. People looking for the bursting of the AI-driven bubble may have to wait a while longer. This article suggests that Wall Street strategists, including Jim Paulsen, are starting to look at high valuations as a kind of “new normal”:

“There’s something weird going on with valuations from what they used to be — that is, there’s an upward trend in the valuation range,” said Paulsen, who now writes a Substack newsletter called Paulsen Perspectives.

Will gold keep going?

People keep asking me if gold can keep rising. The best answer I have is: unfortunately, yes. Gold ripping to all-time highs, while exciting for goldbugs, is not a good sign overall. There’s a distinct lack of trust in governments and central banks to manage their debt and spending situation.

The dollar certainly doesn’t like it:

DXY US Dollar Index

As for the yen? Well, the dollar index is down almost 10% YTD and USD/JPY is still at 148. If you are waiting for a stronger yen, you’d better hope the BOJ gets back to raising rates soon. Your mortgage won’t thank you if they do, though…

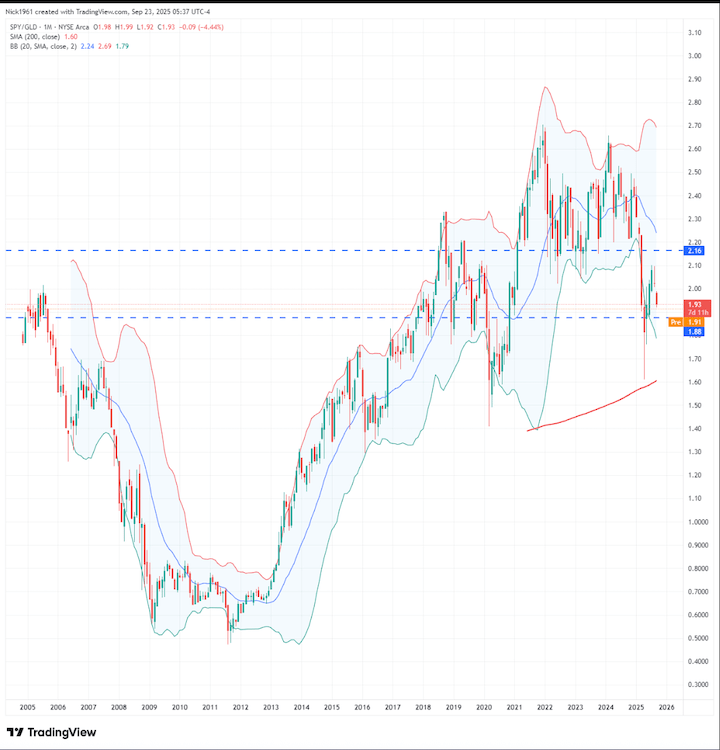

Talking of gold, here’s a chart for people to really hate on!

SPY/GLD

That came from this post by Nick G: “The price of equities is completely unchanged since 2005. All that has changed is the value of the denominator.”

So, priced in gold, the S&P 500 went nowhere since 2005. All “gains” were just the dollar losing value. And that includes dividends, apparently!

No wonder people are hyper-gambling on crypto and tech stocks…

Here’s an interesting (perhaps triggering) opinion piece on financial repression and why you want to own gold, silver and Bitcoin in the face of what’s still to come.

Speaking of which…

All eyes are on Bitcoin now as we enter Q4. If stocks remain strong into year-end, what will Bitcoin do? No price predictions from me, but I see a melt-up before a melt-down. This year’s theme has been long-term holders (who bought at rock bottom prices) enthusiastically selling to institutions that are hungry to secure their share of the network. If the OG’s put a pause on selling, look out above.

I’m hearing lots of talk of an extended cycle, a move to a 5-year cycle, and even a supercycle. I heard these same things in October 2021. I’m not saying the theory is wrong, but it was very wrong last time. I’ll believe the 4-year cycle is no longer relevant when I see the evidence. Until then, sign me up for a Q4 meltup followed by a treacherous 2026.

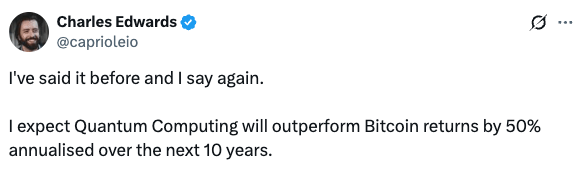

Quantum Leap?

I wrote a post in late 2024 about Quantum Computing. Almost nobody read it. Very few people are discussing QC or even aware of what it is. For me, it’s turning into a no-brainer satellite holding. Incredibly volatile, but with massive potential. Don’t bet the farm, but maybe study up a bit?

⚛️ Quantum is growing faster than anyone realizes — and it could disrupt everything, even Bitcoin. @Jamie1Coutts and @caprioleio.

Valued at just $52B, this misunderstood tech may be the biggest opportunity of the next decade. pic.twitter.com/6Ko1IoyhB8

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I watched the David Beckham documentary on Netflix a while back. I highly recommend it, even for Liverpool fans like myself!

One thing that struck me was his beekeeping hobby. Of all the things a guy like that has money to spend on, he is clearly getting a lot of joy out of keeping bees and producing honey. The reason I remember this is that I met up with an old friend not long ago and he gave me some of his homemade honey. He has a full-on beehive that he is working on with his kids. What a great way to spend time and money!

I recently saw a few posts about spending money well. It’s something that Ben at Retire Japan has discussed, too. Many of the posts I saw were from crypto bros discussing how to spend their winnings from the bull market. (yes, this is a sign we are near the top!)

The fact is that many people who are good at saving and investing (or trading crypto) struggle with actually enjoying their money. I think it requires a shift in mindset to spending as an investment.

Spending isn’t the opposite of saving; it’s about aligning money with values

A well-chosen expense can yield returns in happiness, health and memories

Maybe you can consider a “joy budget” alongside your savings and investing goals

With that in mind, I have pilfered, borrowed, adapted and brainstormed some ideas on how to spend money well:

Experiences worth spending on

a. Travel and exploration

Hardly an original idea, but we Japan residents are blessed with an abundance of options for holidays and weekend trips, not to mention first-rate public transport if we don’t want to drive

Consider seasonal highlights such as autumn leaves, cherry blossoms, and summer matsuri

Don’t let the weak yen stop you from having fun; you can take a beach holiday in Okinawa or snowboard in Hokkaido without even breaking out the passport

If you want to go to the next level, look into getting a holiday home in the mountains or on the coast

My one piece of advice as a parent of young kids: when you book that family-friendly hotel trip, you need at least two nights. Otherwise, you don’t get to check in until 3pm, and then you have about 2 hours to have fun before it’s dinner time, bath time, bedtime. And then at 10am the next morning, they kick you out! Some places will let you use the facilities before check-in, but for those that don’t, you need the extra night so you can enjoy a full day of fun!

b. Unique cultural activities

Tea ceremony, ikebana, calligraphy, martial arts

These are one-of-a-kind experiences not easily replicated elsewhere

c. Learning and growth

Hire a coach for your hobby. Whether it’s tennis or language study, why not accelerate your learning?

Online learning: from Excel basics to digital marketing and investment banking, Udemy offers a course for nearly everything. It’s also very affordable compared to going back to school!

Hire a cleaner, either regularly or spot cleaning for the bathroom, kitchen, air-con, etc. That kitchen extractor fan gets gnarly!

Cooking service – we use this one as my wife and I both work. We have a lady come once a week for three hours, and she cooks around four meals. Then we just set the rice cooker and heat up the food after work

Material possessions that add value

a. Home comforts

Good quality mattress and pillow

Ergonomic desk chair, if you have a home office/study

Artwork – buy some nice paintings to hang in your home

Kitchen gadgets

Home gym equipment

Home sauna – yes, some people have done this, and in a Japanese house! (not my thing, but it’s a baller move)

b. Clothing and gear

Throw out all your socks and underwear and buy new ones

Upgrade your wardrobe – go full American Psycho if you have to!

Decent rainwear

Nice winter coat

High-quality shoes

Get that Omega Speedmaster that Noah Lyles is wearing! (I just noticed this watching the World Athletics Championships, although I don’t think I can bring myself to spend that much on a watch…)

c. Tech upgrades

Upgrade your Zoom set-up – nice camera, microphone, lighting (this is high on my list right now)

That new orange iPhone (yes, I am tempted…)

Noise-cancelling headphones for train commutes

Personally, I’ll pass on those smart home devices. Tech companies are spying on me enough already!

d. Hobby investments

Musical instruments, art supplies, outdoor gear

Sports equipment (new golf clubs, yeah!)

Spending on relationships

Host dinners or gatherings – throw a party!

Trips to visit family, or to fly them to you

Join clubs or networks to expand your circle

Date nights (where’s the best babysitter service???)

Random other feel-good stuff

Take private cars to the airport instead of lugging all your stuff on the train

Keep your haircuts on a tight schedule, keep it fresh instead of waiting until it gets shaggy

If you’re not into personal finance/investing, hire someone to help (coaching service here!)

Buy some Bitcoin for a young family member in the next bear market and keep it for them (substitute for gold or stocks if you prefer)

Some of the best lifestyle advice I ever came across was from Jim Rohn. He published an audio book called The Art of Exceptional Living in 20023 (CD or cassette, yes, it’s old school! I’m sure you can find a digital version somewhere)

I still listen to it now and then. It’s important to remember that it’s not the money, it’s the style that counts!

Being good with money is not just about saving; it’s about knowing how and when to spend. The best spending aligns with your values and enhances your life. Use your money not just to build wealth, but to build a life you will look back on with joy.

Did you find anything interesting? What else have you got? Please feel free to drop other great suggestions for spending money well in the comments.

And, finally, a disclaimer: none of this is spending advice. Do what makes you happy. I will not be responsible for arguments with your significant other following the purchase of any of the items mentioned above!