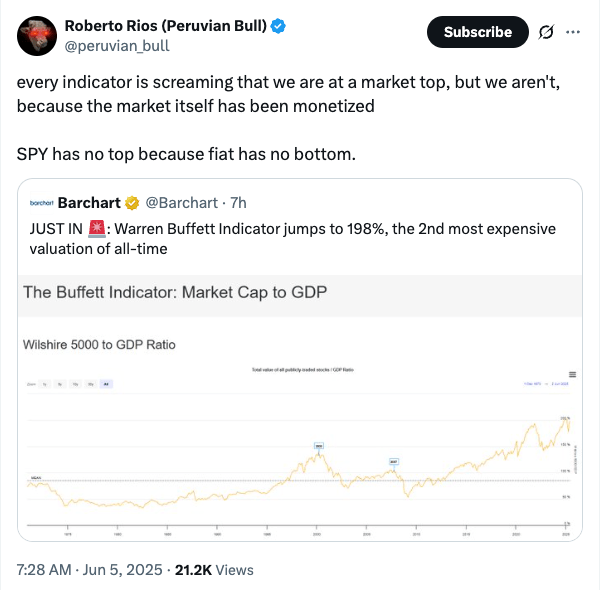

I am starting to see people discussing the idea that the stock market has been so pumped up on debt steroids that it simply won’t be allowed to go down for an extended period again. Normally, this kind of talk would be a massive flashing sell signal, but it’s not an idea that is being broadly discussed. It’s just popping up in pockets here and there.

Of course, stock markets go up and down. In fact, the mighty US market took a hit in April due to the Liberation Day tariff malarkey. But did you notice how quickly it bounced back? Pretty much a V-shaped recovery. Same in March 2020.

I’ve said it before: the money has been funny since the 2008 global financial crisis. Many institutions that should have gone under were propped up at the expense of taxpayers and we’ve been getting screwed ever since. Economies and big business have become addicted to liquidity.

Sounds like tin foil hat stuff?

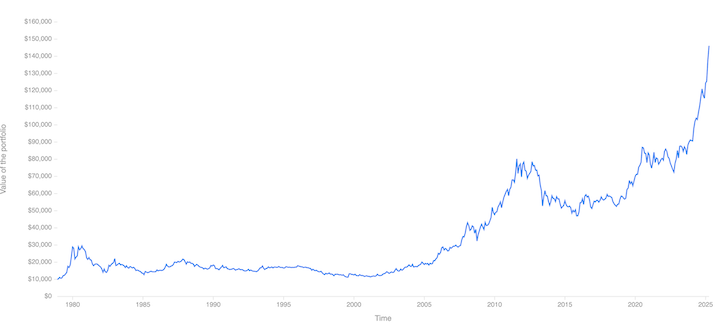

That’s the MSCI World Index. See what happens after the 2008 crash?

Here’s the gold chart for comparison.

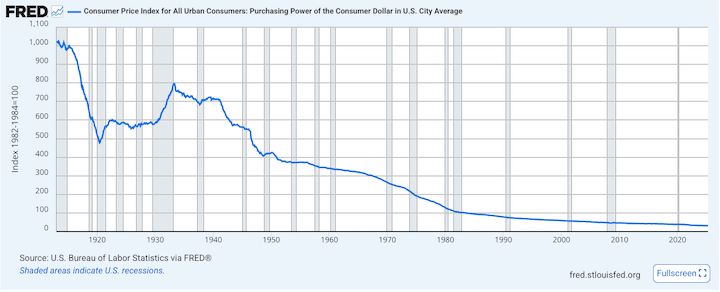

So, are the assets going up, or is the unit of account going down? Check out the purchasing power of a dollar over time.

Ding ding ding ding ding! So, 2008 clearly wasn’t the start of the pattern. It just intensified after that.

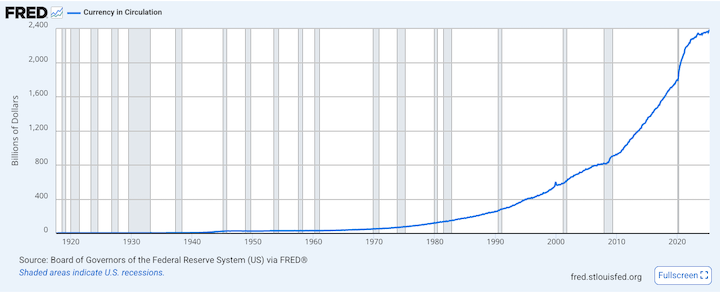

The Federal Reserve of St. Louis puts together some pretty charts, doesn’t it?

Take a look at this one – currency in circulation:

Hello! So, if you keep creating more dollars, the purchasing power of a dollar goes down, and the value of assets and other stuff goes up against your inflated currency. I’m picking on USD here, but everywhere else looks the same. Probably worse.

Here’s a question I get asked a lot: “How do I convince my very conservative partner that we need to invest more?”

Answer: Just teach them that the market is going up forever!

If assets are going up forever, you’d better own some! You probably don’t need to fret too much about timing the market. Just make sure you keep a nice cash reserve so you don’t have to dip into your investments in a crisis, and yolo the rest into stocks, commodities, real estate, bitcoin and anything else that isn’t cash in the bank.

Of course, this is all somewhat tongue-in-cheek. But is it really much more complicated than that?

Please don’t misunderstand. Stocks can still go down 30-50% at any time. Bitcoin can still dump 50-80% and probably will next year. You should be prepared for these outcomes and never let yourself become a forced seller. But, over the long term, these assets go up and to the right because the denominator is cooked. Did you notice how long the whole DOGE ‘let’s reduce wasteful government spending’ drive lasted? It’s not even June, and Elon and Trump are melting down in public.

If you’re wondering why you have to become a money manager just to break even with inflation, here you go:

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

You might have noticed an uptick in articles covering bonds recently. In particular, bond yields and bond auctions. Bonds are confusing, and it’s often easier to just go and read something else, but you might be getting the sense that something is happening in the bond market. Like it’s trying to tell us something.

The market always finds something to worry about, and usually, those worries are temporary. This year alone, we’ve had inflation, stagflation, recession, tariffs, and trade wars, and the sky hasn’t fallen yet. But now the market is worried about bonds. And it’s not just worried about US treasuries. The same concerns surround UK gilts, Euro bonds, and Japanese government bonds.

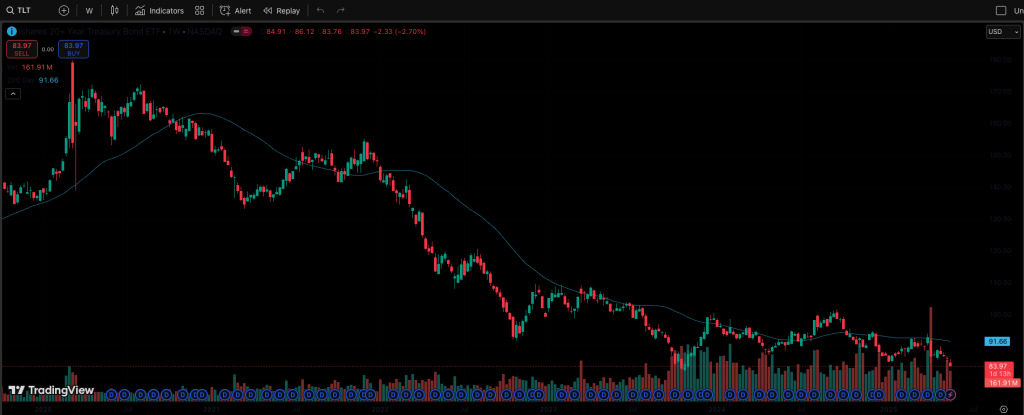

This week, the US 30-year treasury yield has been flirting with the closely watched 5% level. Last Friday’s Moody’s US credit downgrade got things rolling. Then, on 21 May, there was a weak treasury auction, and the 30-year closed at 5.09%.

As yields move inversely to price, rising yields indicate that investors are selling bonds. The weak treasury auction, like recent weak gilt and JGB auctions, illustrates a lack of appetite for new bonds. So why are people so worried about bonds these days?

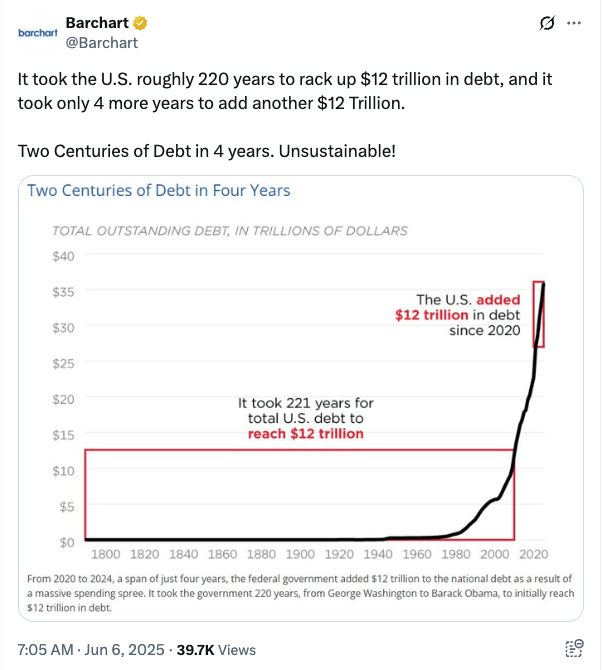

It’s the debt, stupid

At 237%, Japan is the heavyweight champion in debt-to-GDP. The UK is at 96% and the US is at 124%. None of these figures is encouraging. Japan is clearly not paying that back. The UK economy is in disarray, and you may remember Liz Truss almost blowing up the bond market in September 2022.

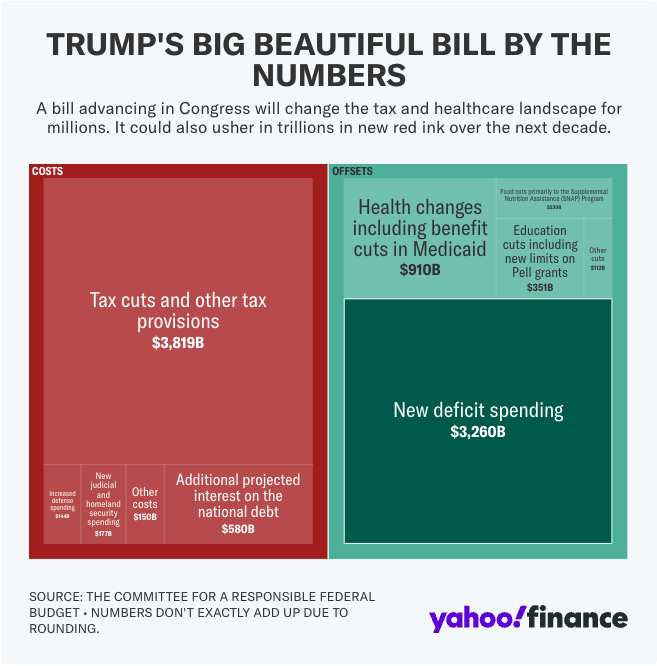

Trump talks a lot of smack, but his big beautiful tax bill is only going to inflate the problem over time. Anyone who believes he is going to cut deficit spending lives in MAGA fantasyland.

The bond market clearly doesn’t like it.

Is it happening?

The macro-heads I read are all fixated on yields, deficit spending and the massive risk flashing in the bond market. But is something really going to break, or is this just another worry that will soon make way for the next thing?

I’m not going to macro larp here, and I dislike doomers, so here’s a solid thread from Capital Flows on why we could be at an inflection point. It’s recommended reading for anyone trying to get their head around the current situation.

The tldr: Central banks are behind the curve – surprise! Meanwhile, banks are issuing debt like there’s no tomorrow. These big credit deals are feeding money into the economy and preventing a slowdown in growth. When central banks fall behind in a credit cycle like this, bond markets can crash because growth and inflation risewhile everyone expects a recession.

Does this mean I should not own bonds?

This is an important question. For traders, the trade is definitely sell long-term bonds. (TLT)

For investors with a diversified portfolio, should they be dumping their bonds and buying gold, copper, bitcoin, etc? I don’t think so. This is short-term tactical thinking and only for people who know what they are doing. By nature, a strategically diversified portfolio is always going to contain some assets that aren’t doing so well. Right now, it’s just the turn of bonds. Unless your time frame has changed dramatically, you can just sit tight.

Big developed economies losing control of yields is a scary proposition, and they are likely to do whatever they can to kick the can down the road and avoid the pain. Just last month, a surge in treasury yields caused Trump to back down on tariffs, remember?

Is this why Bitcoin is ripping?

It’s one of the reasons, yes. BTC is fundamentally a release valve for macro liquidity (I was dying to say that, but I got it from Capital Flows too!) What it means is, the more liquidity that gets pumped into the system, the higher the BTC price goes.

BTC is also going up because it’s at that stage of its own 4-year cycle. But it’s funny how that seems to align so well with global liquidity cycles. There’s probably a bit of mileage left in this bull market yet!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

“It never was my thinking that made the big money for me. It always was my sitting. Got that? My sitting tight! It is no trick at all to be right on the market. You always find lots of early bulls in bull markets and early bears in bear markets. I’ve known many men who were right at exactly the right time, and began buying or selling stocks when prices were at the very level which should show the greatest profit. And their experience invariably matched mine–that is, they made no real money out of it. Men who can both be right and sit tight are uncommon.” – Jesse Livermore, in Edwin Lefèvre’s “Reminiscences of a Stock Operator”

We are so back!

Little more than 6 weeks after Donald Trump nuked markets with his “Liberation Day” blusterf**k, stock indices are right back where they started. Congratulations on surviving! The circus is far from over, but it feels like we just went through boot camp on how to operate under this administration. My personal goal from now on is to ignore every word the man says and focus on what actually gets done. There is way too much noise!

Anyway, check in on the doomers. They probably need to come out of the bunker, touch some grass and catch some Vitamin D.

The great dealmaker is in Saudi Arabia now, doing deals, I presume. Note the presence of Nvidia’s Jensen Huang among the tech CEOs there with him – I would not bet against that company to emerge from the chaos stronger than ever.

So what’s going on?

Checking on the news, Nvidia isn’t the only AI/semiconductor play catching a bid. Advantest, Tokyo Electron and Disco are all perking up too.

Softbank Group is also on the rise after posting its first full-year profit in four years.

Department store operator Mitsukoshi Isetan announced an expected net profit of ¥60 billion for the current fiscal year, up 14% year-on-year. Those tourists must be spending hard while we plebs struggle to buy rice!

Things don’t look so rosy for the Japanese auto industry, though, with Honda and Nissan crumbling under the uncertainty around tariffs. There is more than tariffs at play here as both have struggled with sales in the US and China. The two companies abandoned plans to join forces earlier this year and who knows where they go from here. Nissan is clearly worse off and will shut 7 vehicle plants and cut 20,000 jobs globally.

Come for the global recession fears, stay for the long-term debasement of the yen!

USD/JPY is back around ¥147 after the BOJ needed a breather from raising rates. If they are planning to wait for some respite from global economic uncertainty before hiking further, we will be back in the ¥150s soon.

Wakey wakey

“If you own crypto, I can’t stress this enough: the best thing you can do is go to sleep for about 3 months. Block out the noise.” – I wrote this in my opening post of the year in January. There have been many dips and ‘it’s so overs’ since then, and yet here we sit in mid-May with Bitcoin back over $100k.

It’s probably time to start paying attention again. Metaplanet is creeping back towards the highs. I sold half of my holding in the run-up in Jan/Feb, and it’s looking like time to start averaging out the rest. Maybe take out half in the next few weeks and save the rest for Valhalla?

Even Ethereum has woken up!

Alts have been battered in the dips. With a tidal wave of ETF inflows, BTC dominance shows no sign of slowing down. Alt holders would like to see the orange coin break the all-time high and then chill for a while. Will they get their alt season? The exit is narrow and it won’t be open for long…

Where does BTC top? Gun to my head, I say we get a run now, followed by a quiet summer, then one more assault on the summit in autumn.

However, if you are looking to take profit, don’t listen to me or any other people on the internet. Nobody knows anything. The smart money is scaling out already. Execute your plan.

If you are a long-term BTC investor, and for at least part of your stack you should be, all you gotta do is sit tight!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Remember when everyone thought a Trump presidency would be business-friendly?

I admit to belonging to that camp initially. Stocks soared the first time he was elected, when most people expected them to tank. They also ripped between the election and the beginning of his second term, as people bet on a golden age of deregulation. Remember all the tech CEOs at the inauguration?

And then the madness began.

I’m not interested in getting into political commentary, but I will say this: it really couldn’t have been handled much worse. Anyone who has read Chris Voss’s book knows that you don’t start a negotiation with belligerence and threats and expect everyone to come meekly to the table. Anyway, my opinion doesn’t matter. The markets have spoken. So far, Trump 2.0 has been an unmitigated disaster.

Wall Street is openly disussing a “Sell America” trade. The great dealmaker must hate that one. It’s happening, though – look at treasury yields, look at the S&P 500, look at the dollar. And look at gold!

Gold isn’t just a safety trade here. It represents a stampede away from USD-denominated assets. European and emerging market stocks are also seeing inflows, but they come with their own risks as the haphazard tariff ‘negotiations’ blunder ahead.

So what happens now?

Is America really done? Does gold go up forever?

No and no are the short answers. However, the world is clearly changing before our eyes. Here’s an excellent thread summarising Howard Marks’ recent comments on what is happening. Like it or not, globalisation made a lot of things cheaper. As countries become more inward-looking and focus on domestic production, prices will rise. America is still expected to outperform in the long run, but it will need to work harder to attract capital. It is no longer the obvious go-to market, at least while all this chaos is raging.

Can gold still go higher? For sure, but it’s starting to look like Bitcoin does in blow-off top phases. Weekly cycles also suggest it is close to a top. If you’re a long-term diversified investor, continue to hold it. If you’re looking for the next trade, then digital gold is where it’s at.

Even the macro guys are starting to agree that Bitcoin looks good right now. This article from @fejau_inc puts it all together nicely and is a must read.

Here’s the conclusion from that piece for easy reference: “And so, for me, a risk-seeking macro trader, Bitcoin feels like the cleanest trade after the trade here. You can’t tariff bitcoin, it doesn’t care about what border it resides in, it provides high beta to a portfolio without the current tail risks associated with US tech, I don’t have to take a view on the European Union getting their shit together, and provides a clean exposure to global liquidity, not just american liquidity.

This market regime is what Bitcoin was built for. Once the degrossing dust settles, it will be the fastest horse out of the gate. Accelerate.”

Meanwhile, the Financial Times reported that Howard Lutnick’s son, Brandon is cooking up a $3 billion Bitcoin acquisition investment vehicle with Cantor Fitzgerald, Softbank Group, Tether and Bitfinex. Reuters summary here.

Is the yen strengthening going to hold?

If you are looking for proof that capital is flowing out of America, it’s right there in the exchange rate, currently around ¥142 to the dollar. It’s quite possible the yen could strengthen further from here, but beware the orange man running his mouth. If Bessent can put the gag on him for a while and they get a few wins on the board in terms of trade deals, then the picture can change very quickly.

Yes, I’m aware that the typical trade deal takes around 18 months to complete. Most likely Trump extracts a few concessions from the major partners, including Japan, and declares some ‘tremendous trade deals’. Then he can move onto pumping the markets back up before the mid-terms.

Long term, I believe the yen is cooked. Nothing has changed there. Short term, we could be at ¥120 just as easily as ¥160 in a month or two. Who knows?

So, sell America or not?

Traders gotta trade, and right now the trade is sell America for anything else you can lay your hands on. For long-term investors, I would view cheaper US asset prices as an opportunity to accumulate. Don’t change your monthly investment allocation too hastily!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

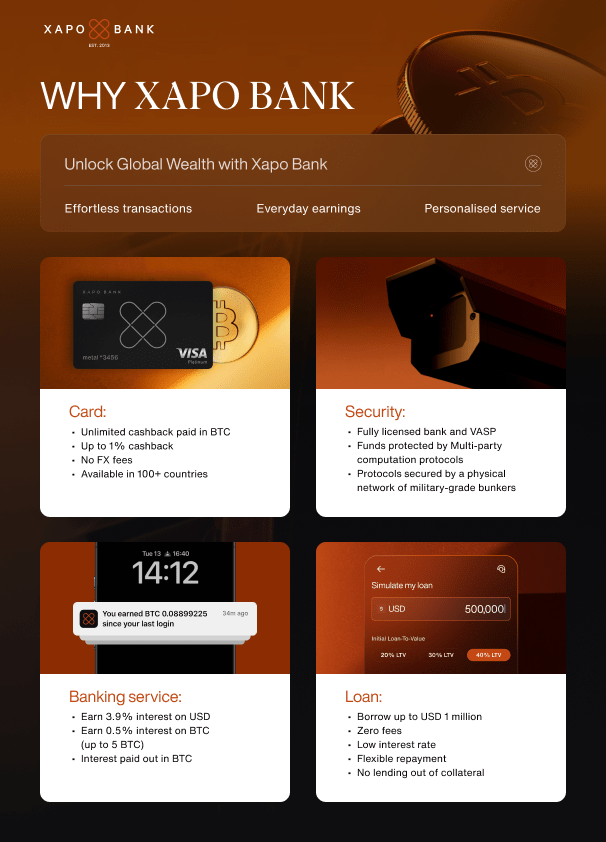

One of the major obstacles to wider Bitcoin adoption has always been the issue of storing and spending coins. Fortunately, it is getting easier to do both.

I bought my first Bitcoin on Xapo in 2017 and have been storing part of my holdings there ever since. Back then, Xapo served as both a super safe custodian wallet and a trusted platform to buy, sell and store Bitcoin. In the last few years, it has become much more than that.

There are many ways to manage Bitcoin storage, but here is my strategy:

Do not leave Bitcoin sitting on an exchange

Learn how to self-custody securely

Diversify risk by storing some BTC with a trusted custodian

Bitcoin purists will likely agree wholeheartedly with points 1 and 2 while vociferously objecting to point 3. That’s fine; I get it. However, I live in a wooden house in an earthquake-prone country, and I’m not entirely comfortable having all of my BTC in one place.

Also, I like to have the option to spend some of my Bitcoin or borrow against it if I want to. That’s not so easy to do with the keys sitting on a hardware device.

Furthermore, I value having a functional USD account. I have plenty of experience with offshore banks, and none have been as easy to use as Xapo Bank.

That’s why I’m still using Xapo Bank today.

Xapo Bank’s history

Xapo was first founded in 2013 and provided a secure cold-storage product using a distributed network of physical bunkers. Yes, you read that correctly! Xapo combined cutting-edge key technology and good old underground physical vaults to protect its clients’ coins. In 2021, Xapo expanded its services, founding Xapo Bank. Headquartered in Gibraltar, the company is licensed as a bank and Virtual Asset Service Provider (VASP) by the Gibraltar Financial Services Commission.

Xapo Bank’s services

Xapo Bank’s account is entirely app-based and enables Bitcoin customers to hodl, transact, earn, grow and borrow. It also now offers stock and ETF trading.

Users control a main BTC and USD account, which can be used for day-to-day transactions. Then there is the savings account, which pays interest on USD and Bitcoin holdings. And finally, there is the BTC vault for secure cold storage.

The USD savings account currently pays 3.5% annual interest, and the BTC savings account pays 0.5% per year. (rates are subject to change)

Xapo Bank has also just launched a new BTC Credit Fund, offering a simple way for people to grow their Bitcoin by earning up to 4% APY on their holdings.

The Bitcoin trading fees are very competitive, and both Bitcoin and USD can be transferred easily and inexpensively from the app.

Users can opt for both physical and virtual debit cards, issued by Mastercard and VISA (depending on their country of residence). The cards pay 1.00% cashback, and the really neat thing is you can choose whether to spend your USD balance or your BTC balance. People often complain that you can’t pay for stuff in Bitcoin – well, now you can!

ATM withdrawals are also free up to some thresholds.

Along with BTC, users can also access S&P 500 and NASDAQ stocks and ETFs to grow their balance.

Customers who need cash but don’t want to sell their Bitcoin can borrow against their BTC holdings at an initial loan-to-value of 20%. The cash arrives in under a minute, ready to use through debit cards, bank or crypto transfers.

Borrowing against Bitcoin may also be a clever way to avoid triggering a taxable event. I have been trying to find confirmation of this for Japan tax residents and have not been able to find anything so far. Selling or spending crypto creates a taxable event. However, it seems likely that borrowing against crypto does not – please note, this is not tax advice, and readers should do their own research before taking action.

One thing is for sure: borrowing against Bitcoin is a smart way to avoid selling at inopportune times, when the market is down, and still benefit from future asset appreciation.

Ok, it sounds amazing, but what does it cost?

Of course, all of these services come at a cost. Membership is USD 1,000 per year.

Some people struggle to come to terms with paying the annual fee. My take on it is that it’s worth it for an easy-to-set-up and use overseas USD account alone. I have used several offshore banks previously, and the transaction fees were significant. Many have a minimum balance requirement with higher costs if you fall below the threshold.

With debit cards, savings accounts and the BTC vault, Xapo Bank is offering a premium banking service at a manageable cost. I can tell you that the app is very smooth and easy to use, and for a hodler like me, the appreciation of BTC over time easily covers the fees. If BTC trades at over USD 100,000, then 1 BTC in the savings account earning 0.5% annual interest already pays half the cost!

The customer service is top-notch, too. Customers have a dedicated Account Manager, whom they can contact by email or chat on the app. If there is a security issue and a bad actor tries to take control of your account, the account manager will get on a call with you to verify your identity and take action to protect your account.

How to open an account

Opening an account is simple: Click here, and all you need is an ID or passport and a quick selfie. Personal information is verified using your mobile phone.

Referral program: Use this link or referral code XRP-HFF-MR and receive US$42 per month in BTC for 12 months. (To qualify each month, you must have an active paid membership and maintain a minimum of USD 5000 or its BTC equivalent balance in an eligible Xapo Bank account during the cycle)

Any questions?

I am a satisfied customer and have been using Xapo since 2017. Feel free to ask me anything in the replies or via the contact form.

If you have questions for Xapo Bank, check out the FAQs on the website and get in touch with them directly!

If you use the referral link/code to sign up as a member with Xapo Bank, I may receive a small commission, at no additional cost to you.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s been a long week. Is it me, or are +/-9% swings on the Nikkei 225 index starting to feel normal? Traders must be loving this – at least the good ones.

I’m not so impressed. Of course, there are buying opportunities, but it gets a bit tiresome when markets swing this wildly based on the pronouncements of one guy who just can’t STFU for 5 minutes.

Click it, I dare you! And don’t get me started with the Simpsons memes.

Where was I? Tapping the sign, right. The free lunch quote has been attributed to Harry Markowitz, although I have heard Ray Dalio say something similar. It’s a drum I have been banging for years, sometimes with minimal effect.

When the stock market is going up, nobody cares about diversification. Why would I want to own bonds and gold and other stuff when stocks are on a tear? Just buy the index and chill, right? It’s easy to forget that stocks take the stairs up and the elevator down.

Until you get a reminder.

In 2002, psychologist Daniel Kahneman won the Nobel Memorial Prize in Economic Sciences for his work on the psychology of judgement and decision making. Kahneman points out that individuals are more depressed with investment losses than they are satisfied with equivalent returns. In other words, people hate losing money considerably more than they like making money.

Big liquidation events are like waking up after a party. It was fun, but now it’s time to sober up and review your time horizon, risk profile and asset allocation.

Are you diversified enough?

If recent events haven’t troubled you, and you have barely looked at your investments, the answer to this question is probably yes. Carry on!

If things have been a little nervy, then maybe you were over-exposed.

Don’t get me wrong, I’m all for buying stock indices and holding them forever. It’s not a bad strategy, as long as you can stomach the downturns. And as long as you don’t need the money soon. And, it’s not like a diversified portfolio doesn’t go down in times like these either. When panic sets in, people will sell anything they can get their hands on, but pretty soon you will see a flight to safety.

An underappreciated aspect of diversification is the opportunity to tactically rebalance and take advantage of market events. I sold some of a gold ETF this week near all-time highs and bought stocks while everyone was puking them. I didn’t need dry powder. Just a little reallocation.

You can’t do that if you don’t own the gold in the first place. You have to find more cash.

A quick thought experiment

If you are reasonably young and earning good money, then the recent market gyrations are just a blip, but do me a favour: imagine you are 65 years old, about to retire, with a nice fat nest egg invested in the MSCI World Stock index.

And the market dumps 20% in a couple of days. It takes a breather over the weekend and then resumes dumping in earnest. 30% of your retirement pot is gone. Financial media is screaming about recession, trade war, deleveraging or whatever it is this time. Remember in March 2020, when the market crashed and we faced the reality that the entire world was about to shut down? The doomer economists are running victory laps, and the market looks like it is never coming back from this.

How do you feel?

Remember that feeling when you are making future investment decisions, especially as you get closer to spending the money.

Of course, what happened after March 2020 was that central banks slashed interest rates and unleashed a tidal wave of stimulus, and the markets came roaring back before the year was even over. But that type of thing comes at a cost – that’s why your hard-earned cash doesn’t buy as much stuff any more…

Ok, so how do we do this diversificationthing?

There are various ways to get yourself a diversified portfolio. How hands-on do you want to be?

For the people who want to put as little effort as possible into it, you can simply buy multi-asset ‘balanced’ mutual funds. I recently came across a collection of Japanese funds that are divided up by age group: “Happy Aging 40”, “Happy Aging 50”, “Happy Aging 60”. The allocations get more conservative the higher the age. These types of funds are available everywhere. Simply dump your money into the fund that fits your time horizon and get back to whatever you’d rather be doing.

In my advisory business, for larger chunks of money, I recommend professionally managed investment portfolios fitted to the client’s base currency and risk profile. Yes, they cost more than an ETF, but they are incredibly well diversified. The asset allocation is reviewed annually, and every quarter the managers implement a ‘tactical overlay’ and buy more of the assets they like and sell some of those they don’t. These guys don’t just buy a broad stock index – they are breaking equity holdings down by style: value, growth, small/large cap, etc. Of course, the entire portfolio is rebalanced annually.

I also recommend a core/satellite approach for even broader diversification. That’s how you slot in the algorithmic trend following strategy that trades stocks, interest rates, currencies, metals and other commodities with very little correlation to any one market. Funnily enough, it likes volatile times like this.

For coaching clients, I take the knowledge I have gained from watching professional money managers and help them develop their own asset allocation using low-cost ETFs. Click the coaching link to find out more.

Keep it simple

Here are a few action points if you want to take on this job yourself:

Separate regular and lump sum money. Regular is the money you invest every month in a pension, savings plan or Tsumitate NISA. If you are relatively young, you can just allocate all of this to stock indices/funds. Let Dollar Cost Averaging do the work for you.

Lump sum money is a chunk of cash you have saved up that you are looking for a better return on. Here, you are going to want more diversification, and you should focus on the currency you are most likely to spend the money in (your base currency). The asset classes you want to look at are: cash, domestic (base currency) bonds, overseas bonds, domestic stocks, overseas stocks, property, and commodities. Hold more stocks if you are young, and more bonds and cash if you plan to spend the money soon. Allocate 70-80% of the lump sum to this broad portfolio, and the remainder can go into satellite holdings to beef up the areas you are most bullish on. For example, if you like Bitcoin, that’s a great satellite holding.

If you are gonna get really serious though, you are going to want to diversify your bonds.

Peace out!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I like to treat readers to something different from time to time, and today, we have a guest post from Adrien Pichon of Bonsai Collectors. I must admit, I had never thought about bonsai as an investment. However, after talking with Adrien, I realised the trees are collectables, just like artwork or fine wine. (You may remember the six asset classes are cash, bonds, equities, property, commodities and collectables)

So, please read on and enjoy. This is not a sponsored post, and there are no affiliate links. Just a fascinating new asset to learn about.

Most people think of bonsai as delicate little trees, something more at home in a museum or a Zen garden than in an investment portfolio. But what if I told you that some of these trees sell for the price of a luxury car, or more, and that a curated bonsai collection can become a store of value, just like fine art or rare whisky? That’s the world we’re opening up at Bonsai Collectors.

Why Bonsai?

Bonsai are not just decorative plants. In Japan, they are considered living cultural assets. A single tree can be 100, 300, or even 800 years old, meticulously cared for over generations. The craftsmanship, historical value, and scarcity make certain bonsai highly sought after by collectors worldwide, especially as interest in tangible, alternative investments grows.

Prices for museum-grade bonsai can range from $10,000 to over $500,000. And, unlike stocks or crypto, each tree is unique and deeply tied to Japanese tradition and craftsmanship. When properly maintained, they appreciate in value over time, especially as the supply of high-quality, old bonsai continues to shrink.

Making the Market Accessible

Until recently, collecting high-value bonsai was limited to insiders: traditional Japanese gardens, dealers, and a tight-knit community of experts. Foreign investors had limited access not just to the trees, but to the knowledge and care needed to preserve their value.

That’s where Bonsai Collectors comes in.

We’ve built a curated online marketplace where collectors and investors can explore, buy, and preserve authentic bonsai trees grown and maintained in professional gardens in Japan. Each tree is authenticated and tracked with secure ID cards, including its age, artist certificates, and maintenance history.

We work with renowned bonsai artists and export professionals to ensure the trees are properly cared for and legally exportable when needed. Some clients display their bonsai in Japan and enjoy the cultural prestige; others bring them home or include them in exhibitions and events.

Beyond the Tree: Real Asset, Real Care

Owning a bonsai is like owning a living sculpture, but it’s not passive. Maintenance is key to keeping and increasing its value. That’s why all trees on our platform are maintained by licensed Japanese professionals in registered bonsai gardens.

Collectors can also create their own “bonsai collections” through our platform, combining historical trees with expert care and display options. This isn’t a speculative flip; it’s a long-term asset you can watch grow and evolve.

Serious About Preservation and Return

Bonsai Collectors is not just about buying trees. It’s about preserving cultural heritage while opening up a new, stable asset class. We’re targeting a new generation of collectors and investors who care about where their money goes and what it preserves.

Think of it as part art fund, part heritage protection, and part tangible asset. As wealth continues to shift toward alternative and meaningful investments, bonsai is becoming a new way to express values and build value.

Curious to learn more? Visit www.bonsai-collectors.com to explore the marketplace, learn about bonsai investment, and start your own collection.

Disclaimer: This post is for information only. It should not be considered personal financial advice and does not constitute an offer or solicitation to invest in any of Bonsai Collectors’ projects. Investments like these carry specific risks and readers should conduct their own research before proceeding.

“The line between gambling and investing is artificial and thin. The soundest investment has the defining trait of a bet (you losing all of your money in hopes of making a bit more), and the wildest speculation has the salient characteristic of an investment (you might get your money back with interest). Maybe the best definition of “investing” is “gambling with the odds in your favor.” ― Michael Lewis, The Big Short: Inside the Doomsday Machine

“Most investing apps aren’t for investing. They are dopamine-fueled casinos — flashing charts, fake “free” trades, and endless FOMO to keep you chasing.”

There is probably some truth to this. Certainly, investment products look quite different these days from when I started in the advisory business. However, here’s a funny thing: I’m currently reading an old classic, Jack D. Schwager’s ‘Market Wizards’, and it’s shocking to find how many of the ‘wizards’ have a background in gambling. What’s more, almost all of them use gambling analogies in relation to trading.

In case you don’t know the book, which was published in 1989, it is a series of interviews with top traders, exploring how they made their money. Despite being a little dated, it’s a fascinating read if you like that sort of thing. I haven’t finished it yet and am making some notes as I go. Here is a note I made from the interview with Gary Bielfeldt, who was known for his sizable trades in treasury bonds in the 1980s:

On poker and the concept of playing the percentage hands:

You don’t just play every hand and stay through every card, because if you do, you will have a much higher probability of losing. You should play the good hands and drop out of the poor hands, forfeiting the ante. When more of the cards are on the table and you have a very strong hand – in other words, when the percentages are skewed in your favor – you raise and play that hand to the hilt.

Apply the same principles to trading.Wait for the right trade. If a trade doesn’t look right, you get out and take a small loss; it’s precisely equivalent to forfeiting the ante by dropping out of a poor hand in poker.

When the percentages seem to be strongly in your favor, be aggressive and really try to leverage the trade, similar to the way you raise on the good hands in poker.

Of course, not all gamblers are made the same. Those who understand probability fare much better than those just out to have some fun.

“If you do not manage the risk, eventually it will carry you out” – Larry Hite

One of the recurring themes from the book is risk management. This is a broad subject, but almost all of the traders talk about how they scale back their activity when they are trading poorly. In golf parlance, a bogey is one bad shot; a double bogey is a bad shot followed by a stupid shot.

Cutting losers quickly while letting winners run is another common theme. Ed Seykota’s three golden rules are: Cut losses, cut losses, cut losses! Paul Tudor Jones’ mantra is “never average losers”.

Jones says: “Never trade in situations where you don’t have control. For example, I don’t risk significant amounts of money in front of key reports, since that is gambling and not trading.” That’s an interesting comment considering the number of people I see trying to trade the latest inflation report or Fed meeting.

Bruce Kovner’s first rule of trading is “Don’t get caught in a situation in which you can lose a great deal of money for reasons you don’t understand”.

All of these great traders stress that making mistakes is not only normal, but an important part of the process. PTJ is known for catching major turning points in markets however, he is not the sniper that many people imagine. He may try repeated trades over a period of weeks, getting out as the market moves against him before probing again until he finally finds that turning point.

Larry Hite notes: “You can lose money even on a good bet. If the odds of the bet are 50/50 and the payoff is $2 versus a $1 risk, that is a good bet, even if you lose. The important point is that if you do enough of those trades or bets, eventually you have to come out ahead.”

Trading vs investing

Schwager makes two key distinctions between trading and investing: First, a trader will go short as readily as long. In contrast, the investor – for example, the portfolio manager of a mutual fund – will always be long. If he is uncertain about the market, he may only be 70% invested, but he is always long.

Second, a trader is primarily concerned about the direction of the market. Is it going up or down? The investor is more concerned about picking the best stocks to invest in.

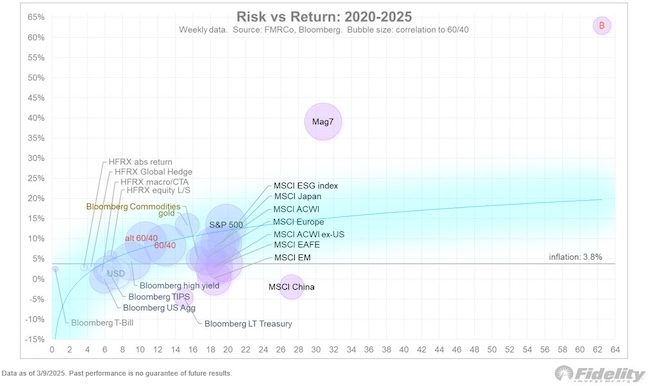

Of course, neither traders nor investors are limited to stocks only. Take a look at this absolutely insane chart from @TimmerFidelity

The chart shows the annualised volatility vs annualized return of various assets since 2020. Notice anything funny?

If you like the Magnificent 7 stocks outperformance, you’re gonna love Bitcoin!

Many will look at the asset in the top right corner and assume that is where the investing/trading ends and gambling begins. Those in the know will note the efficient frontier line you get when you own everything in the chart. My investing philosophy is that’s exactly what you want to do. The only question is how you weight each asset.

Just FYI, Paul Tudor Jones’ largest holding these days is the iShares Bitcoin Trust (IBIT). It’s around 4.5% of his total portfolio.

“Don’t be a hero. Don’t have an ego. Always question yourself and your ability. Don’t ever feel that you are very good. The second you do, you are dead.” – Paul Tudor Jones

Finally, a somewhat sobering message. Two quotes so far stopped me in my tracks and made me think of Japan and its mountain of debt (although they were actually about another economy):

“And you are saying that people look at the deficit year after year and think, “Well, it can’t be so bad, the economy is strong,” and one day everyone wakes up. It is like having termites in the foundation of your house. You may not notice them until one day they gnaw away a big chunk and the house collapses. I don’t think anybody should take a large amount of comfort in the fact that things appear to be holding together.” – Richard Dennis

“If the economy starts to go with the kind of leverage that is in it, it will deteriorate so fast that people’s heads will spin. I hate to believe it, but in my gut that is what I think is going to happen. I know from studying history that credit eventually kills all great societies.” – Paul Tudor Jones

If you do not manage the risk, eventually it will carry you out.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Are we winning yet? It’s tricky explaining to people why investing isn’t gambling when the markets continue to exhibit the qualities of a casino. Where to start?

Even my favourite investing question, ‘Are we in a bull market or a bear market?’ is a tough one to answer right now. Maybe we can get there by the end of this post!

US stocks first

I know many people doubt that Trump actually has a plan, and crediting him for deliberately cooling down the US stock rally seems a bit of a stretch. But you have to remember that he’s got Scott Bessent sitting in the treasury. I lean towards there being method in the madness.

We should listen to what they are telling us. Both Trump and Bessent have been quoted as saying we should expect some turbulence. The sharp drop on Monday was a warning shot. I sit in the camp that says we get 3 to 4 months of significant uncertainty before they start focusing on pumping things up before the midterms in November.

Markets hate uncertainty. It’s going to be a bumpy ride.

The cooler US CPI print last night provided some welcome relief. We are moving towards an economy that is ready for more rate cuts. However, tariffs won’t show up in inflation numbers until next month. Trump & Co. can’t force Powell to cut short-term rates, but Bessent has said that they are focused on bringing down the 10-year bond yield. Something to keep an eye on.

Talk of a recession seems overblown. The US economy is slowing, not sputtering.

“For the first time, Japanese companies truly belong to their shareholders. That’s a massive structural shift—a revolution.”

“Yes, risks remain. But this governance transformation is so significant that it outweighs them. That’s why, even if a crash comes, I focus on making money from the rebound rather than betting on the decline.”

“Put simply: If share buybacks and dividend hikes continue, stock prices will rise.”

“I’ve said before that I’m terrible at predicting markets, but if we zoom out, I’m bullish on Japan.”

The TSE campaign to make life better for Japanese stock investors has been a roaring success. Who says things never change in Japan?

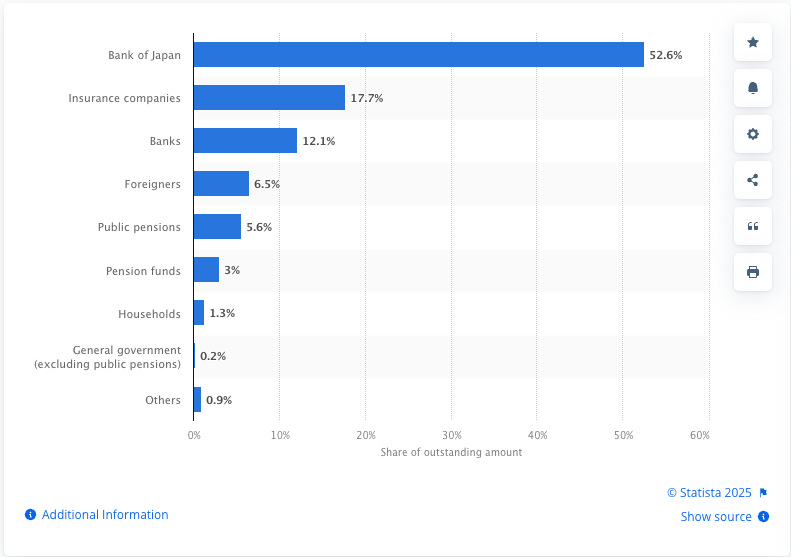

Much as I like Japanese stocks, the macro outlook terrifies me! Long-term bond yields are rising, and you have to wonder how much higher they can go before the Bank of Japan loses control. If the BOJ is not going to continue Yield Curve Control to reign in yields, then it is going to endure the full force of the crash in bond prices when yields get away from it. Maybe the BOJ can endure and hold to maturity, albeit with massive damage to its credibility. But who else is going to suffer?

Statista: Distribution of Japanese Government Bond (JGB) holders as of September 2024

This Japanese stock vs. macro dilemma reminds me of the ever-present earthquake risk. It’s really nice living in Japan, but your house could get destroyed tomorrow! The difference is that the Japanese bond market will take the rest of the world with it if it falls. Fun times!

Crypto

You knew I would get into crypto soon enough, right? More specifically, Bitcoin, seeing as everything else has been trashed. I distinctly remember that, about three weeks ago, we were on a nice trend back towards $100k – there was this beautiful procession of green candles, and I went to bed that night feeling quite confident that I would wake up to six figures again in the morning.

Bybit got hacked by North Korea that night.

Most crypto thing ever lol…

Then we had a poor reaction to Trump’s strategic reserve announcements, and before you knew it, we were fighting to hold $80k.

It is what it is.

I see this going much the same way as US stocks: a few months of ‘It’s so over’ and then ‘We are so back!’.

Follow the money supply. I will cover the Strategic Reserve and US regulation changes in a future post. Suffice it to say that most people are offsides and bearish. I would be concerned if it were any other way.

So, bull or bear?

US stocks – mini bear inside a bull

Japanese stocks – bull

Japanese bonds – don’t look up!

Bitcoin – bull

That’s how I see it. Red days on US stocks are for buying. I will treat the next 3 to 4 months as an opportunity to accumulate.

Japanese stocks, particularly value/dividend stocks, are a great tool to counter JPY inflation.

Diversification across asset classes for serious money.

USD, Bitcoin and gold are insurance policies on the macro risk. Fingers crossed on the earthquakes!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

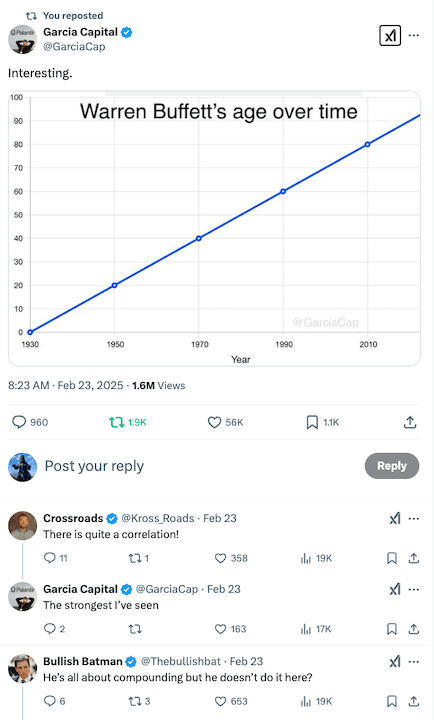

With markets looking a little shaky of late, it’s worth remembering the old saying that time in the market beats timing the market. With Warren Buffett once more making news in Japan this week, this post and Bullish Batman’s comment tickled me:

I think readers of this site will have at least a basic understanding of the benefits of compounding on investments. That said, it can take some time to actually experience its power. I have noticed that one of my accounts, which started small and took a while to grow, has picked up momentum in the last 12 months. I haven’t added new money to it for a while but have been diligently reinvesting capital gains and dividends, resulting in a significant acceleration in growth.

Here’s the Investopedia definition of compounding:

It’s a great reminder that, although short-term price moves make headlines, we should focus on investing for the long term. Accumulate good assets and hold onto them!

Is Uncle Warren coming back?

Warren Buffett has mastered the art of buying quality stocks and allowing them to compound over the long term. In his recent letter to shareholders, the Berkshire Hathaway CEO commented that he is keen to increase his investment in Japan’s big five trading companies. You may remember that Buffett has been playing a very smart game in Japan, issuing debt at around 1% in yen to buy solid companies that pay around 4% income. Shares in those trading companies surged this week in anticipation that Buffett may be coming back for more.

Despite The Oracle of Omaha’s endorsement, the trading houses still face significant headwinds related to yen movements and Donald Trump’s tariff policies. The US President’s aggressive stance on that issue is unsettling for companies that rely on smooth international trade. It doesn’t seem to worry Buffett too much, though.

Speaking of the yen, on 25 February it hit a four-and-a-half-month high of ¥148 to the dollar. With inflation on the rise, the Bank of Japan will come under pressure to continue to raise rates while the US Federal Reserve has rate cuts on pause for now.

The Corolla index reaches 50%

This is new to me, but this Nikkei Article refers to a Toyota Corolla index. It measures the affordability of a typical mass-produced Japanese car by dividing the price by the average annual income. During the good times, it has been as low as 20% but currently stands at a whopping 50%. For comparison, in the US it is 30%.

This clearly illustrates that, although wages are rising, they are failing to keep pace with inflation in Japan.

Nvidia beats on earnings again

In the US this morning, Nvidia might well have saved markets from severe pain, at least in the short term. The chip powerhouse once more beat analyst’s expectations and issued solid Q1 guidance. The company reported Q4 revenue of $39.3 billion and expects $43 billion plus or minus 2% in Q1. Shares were up +3.7% in anticipation of the report but are down in after-hours trading.

It seems to take a lot to get investors excited these days. Trump is talking about a 25% tariff on chip imports and the AI behemoth is still weathering the DeepSeek storm. You may remember that Nvidia’s previous earnings also beat expectations but the stock fell afterwards.

Is the US economy slowing?

Despite the S&P 500 trading near all-time highs, sentiment in the US is increasingly muted. The downbeat mood is generally attributed to Trump’s tariff talk, however, in this Yahoo Finance article, Neil Dutta argues that it is more likely because the US economy is slowing down. He points to weaker economic data coupled with the Fed’s pause on rate cuts acting as a “passive tightening of monetary policy”.

That argument makes a lot of sense and could also explain why, despite a slew of good news, Bitcoin failed to break back above $100k and has now broken down instead. People who have been ‘waiting for a dip’ are not so keen now they have one. We may have to endure some economic pain to push the Fed to start cutting again before the bull market resumes. (no, I don’t think it’s over)

Also, it’s notable that hedge-fund manager Steve Cohen recently struck a bearish tone for the first time in a few years. You can see a snippet of his interview here. (in case the embedded link below doesn’t work)

Sounds like this is a time to be cautious: cash, bonds, defensive equities with low valuations pic.twitter.com/FCZqCSMvFD

— Michael Fritzell (Asian Century Stocks) (@MikeFritzell) February 24, 2025

Cohen states that he isn’t expecting a disaster, but things could be difficult over the next year or so, and it wouldn’t surprise him to see a significant correction.

All the more reason to keep a long-term view and focus on compounding those assets over time!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.