AI has been the relentless driver of markets for several years now. Over the last few weeks, however, the tone has changed, and investors are dumping stocks in companies that may be at risk from AI tools. “Shoot first and ask questions later” is how analysts describe the action.

What is happening?

The AI scare trade is the rapid repricing of companies based on the perceived risk that generative AI will destroy their business model.

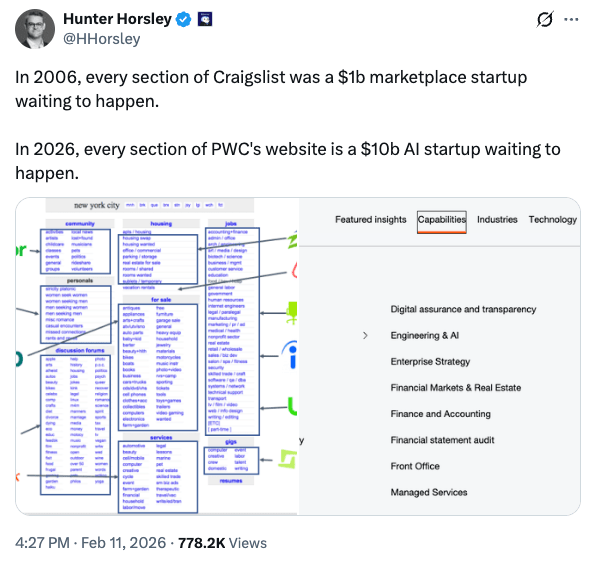

The narrative has shifted noticeably from AI as a productivity driver to AI as ruthless disruptor of whole swathes of the corporate landscape. First, it was software companies, then payments. Now, consulting and even cybersecurity are apparently on the brink of obsolescence.

Much of this is clearly overdone. And some of it probably isn’t. The job now seems to be to identify which services are genuinely under threat and which are merely suffering collateral damage. IBM shares plunged -13% on 24 February after Anthropic said its Claude Code tool could modernise Cobol, an old programming language running on IBM machines. So, is IBM done now?

IGV (the iShares software ETF) is down almost -20% in the last month. In Japan, Sansan Inc (4443) is down -36% over the same period. Are these stocks falling because earnings will collapse? Or because multiples are contracting due to uncertainty?

Regardless of your level of buy-in to the AI story, humans are writing some interesting pieces. Matt Shumer’s “Something Big is Happening” caused quite a stir. Citrini’s “2028 Global Intelligence Crisis” scenario actually moved the market!

I think it’s important to read this stuff because, whether it’s big or not, something is definitely happening.

The Citrini article in particular struck a nerve. It was deliberately positioned as a possible scenario, rather than a prediction. The people writing it off as doomerism are probably more afraid than they will admit. What makes the AI scare trade different from past sector rotations is that many investors feel personally exposed. When the technology threatens your own profession, the fear feels more real.

And the market hates the uncertainty.

How to position

So how should we, as investors, navigate these uncharted waters? Shooting first and asking questions later is probably not a smart approach. I don’t necessarily have the answers, but here are a few thoughts:

If you are in the accumulation phase and mostly averaging into index funds and passive ETFs, there is no need to make any big changes. The indices themselves do a good job of allocating more cash to the winners than the losers. A few software companies may drop out of the S&P 500 over time, but they will be replaced by growing companies.

For more active investors, particularly those who like to pick stocks, it’s a good idea to separate out the genuine risks and opportunities:

- Direct displacement risk – code generation, content creation (ouch!), basic legal/admin work

- Margin compression risk – services that become cheaper, but not obsolete

- AI beneficiaries – infrastructure, energy, chips, data centres, automation

It’s productive to focus on number 3, I think. If AI makes software 10x cheaper, demand for compute, electricity and physical infrastructure likely rises rather than falls.

In the chaos of the last few weeks, I heard about logistics stocks selling off. These are exactly the kind of companies that are likely to incorporate AI and deploy it to streamline processes and boost efficiency.

I saw a client last week whose company does commissioning for data centres. They are the guys who go in and check that everything works before the operation begins. They are jammed with work and can barely keep up.

Where is the power going to come from to run these places? What infrastructure needs to be built? Who makes the wiring, and where do the raw materials come from?

What stocks have been oversold, but clearly are not going away? Meta, Microsoft and Amazon have all weakened on concerns about their massive AI capex. Is the concern justified, or is this just another buy-the-dip opportunity? It’s not the first time these companies’ heavy investment has been called into question, but look at their long-term performance.

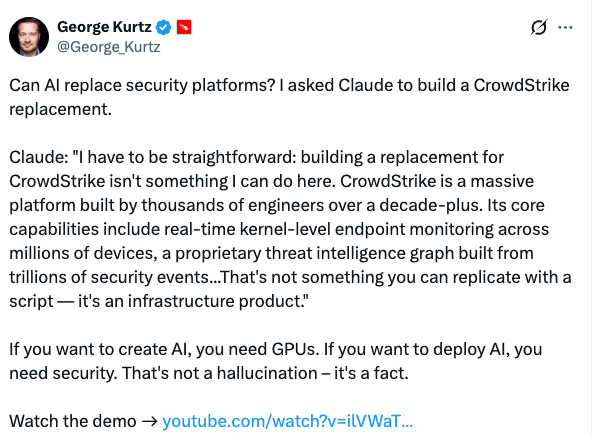

That’s the Crowdstrike CEO, by the way. He might be sweating the stock price a bit, but surely we’re a long way off from vibe-coding cybersecurity platforms.

As always, diversification is the name of the game for large sums of money.

In many ways, the AI scare trade reminds me of last year’s Sell America trade. It was a thing for a while, but then the panic died down.

Stay curious, keep reading, and don’t get too bearish.

It’s one thing to outline extreme scenarios. It’s quite another to position your entire portfolio around them.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.