Welcome to another fun-packed week in crypto. This week, Metaplanet reached ¥6,880 per share and game company Gumi Inc (3903) announced plans to purchase $6.6 million worth of Bitcoin. As I edit this post, I note that GME is considering buying BTC and other crypto.

I am hearing more rumours that Japanese regulators are considering reclassifying crypto as security, paving the way for ETFs and sensible tax treatment. My guess is that it’s likely to take until 2026 but this is a reasonably high probability outcome.

As we approach the sharp end of the Bitcoin bull market, here are a few thoughts and observations:

It’s truly a Bitcoin-driven market

The last 12 months in crypto have clearly been all about Bitcoin. Meme coins had a hot moment in Q1 of 2024 but that market is now saturated and the attention span on new coins is down to a few hours. People are talking about being in “the trenches” when really they are just at the casino.

Similarly, altcoins have mostly struggled to live up to expectations. There are simply too many coins and not enough money to make them all go up at once. AI coins never really had any tech and utility coins never really did much.

Ethereum continues to disappoint. Among the other L1s, Solana has had its moments, mostly driven by the memecoin casino. Hyperliquid and SUI have also shown periods of strength. Binance seems to be toying with launching memes on BNB, which has driven up the price in the last week or so.

If you don’t follow crypto Twitter, I can tell you the mood has been downright depressed for weeks. Many of these people have been hyping the bull market for the last two years and don’t even own any Bitcoin. They are knee-deep in trash and crying for alt season or central bank quantitative easing. (QE)

Meanwhile, Bitcoin is at $96k. It’s up almost 350% from the same time two years ago.

Are you not entertained?

The debate about Bitcoin’s institutional appeal is over

It has been fun frontrunning mainstream adoption but now the suits are here. Blackrock is here, tradfi is here. The US has a crypto-friendly administration that is just picking up steam. 16 US states are debating creating strategic Bitcoin reserves and a federal SBR is under consideration.

Read that last part again.

Institutional money is pumping into Bitcoin. It is not flowing down into other crypto assets like in previous bull markets. It goes into the spot ETFs and stays there.

Serious money is not coming to buy your altcoin bags.

I sound like one of those sanctimonious Bitcoin maxis, don’t I? But identifying what is actually happening is the key, not being right about this coin or that coin.

The harsh truth

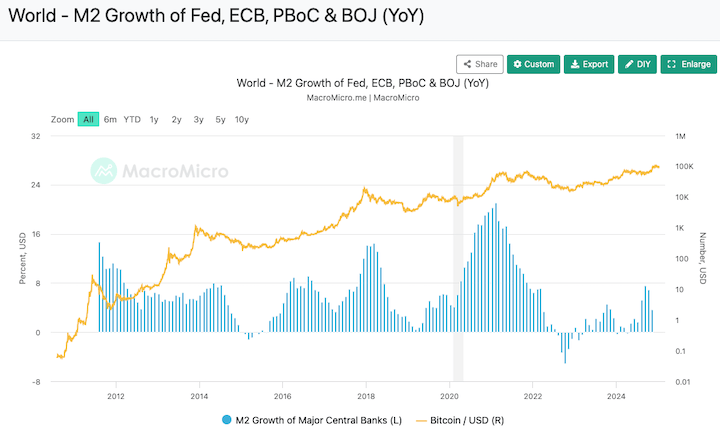

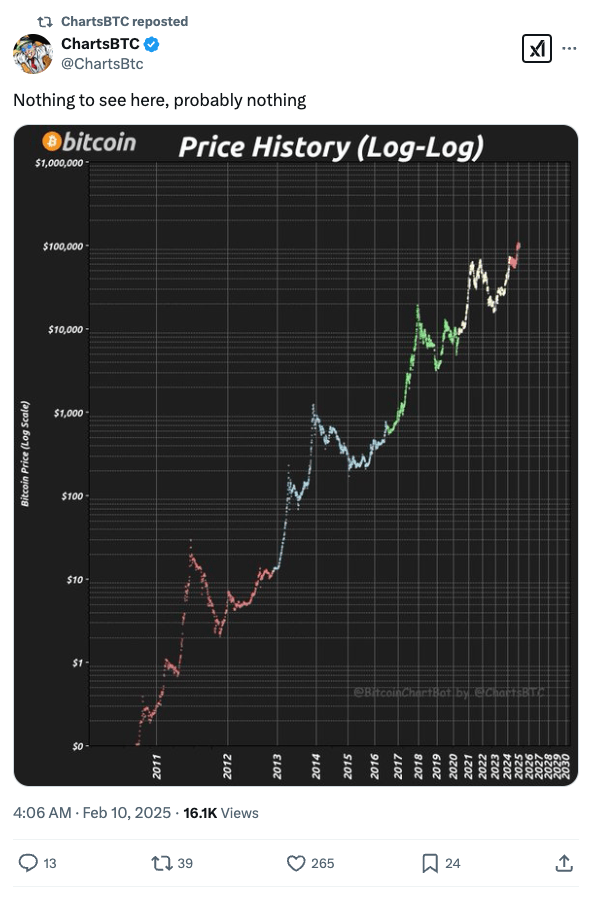

Most people looked at this chart for the last 10 years and failed to act because they couldn’t figure out what the use case was, or it just seemed silly to them. “If Bitcoin is money, why can’t I buy my coffee at Starbucks with it?” It must have taken an incredible amount of overthinking not to buy the asset going up and to the right faster than anything else, but people managed it somehow.

Bitcoin began as a solution looking for a problem. Much mental gymnastics have been performed in defining what it is actually useful for, but years of ZIRP (Zero Interest Rate Policy) and QE (Quantitive Easing) eventually provided the answer: Like gold, Bitcoin is the countertrade to the wanton destruction of Fiat currency by governments and central banks.

It’s the hardest of the hard assets. And now the big boys are buying it.

You may think the crypto people were either lucky or very clever, but the reality is so much funnier:

It’s only a 10x to $1 million per Bitcoin. Do you know how many times this thing has 10x’d? If I sound like the left-curve guy here, it’s because I am.

The volatility will continue to fall and Bitcoin will become another boring tradfi asset, albeit one you can’t afford not to own. Expect diminishing returns from here on.

It’s still going to a million, though. That outcome is right there if you can discipline yourself to accumulate and then sit on your hands for 5-10 years. How much do you need to own to change your financial life?

Study up on the state of global liquidity. This Raoul Pal interview with @crossbordercap is worth a watch. (particularly 27:22 Japan’s Role in US-China Financial Tensions)

FOMO

“Am I too late to on crypto?”

“What do you think about Metaplanet?”

I’ve been getting more of these messages recently. People who couldn’t bring themselves to buy before are now scared they are going to miss out. It’s the signal that we are down to the last couple of innings of this bull market.

Hell, we may already have topped, but I doubt it. For those looking to take profit, the next leg up will offer an opportunity to start moving towards the exit. And there’s only one door, remember.

Beware of unit bias. The big mistake that people make at this stage is deciding that Bitcoin is too expensive at $96k so they need to buy something cheaper to catch up.

The people who own those “cheap alts” have a name for you guys: Exit liquidity

It’s their last chance to offload their bags to a newbie with FOMO.

Be smart.

It’s not too late

This post is meant as a warning but here’s some encouragement:

There will still be opportunities to get on the train. When the dust settles, sometime in 2026, Bitcoin will once again lurk in the buy zone. Below $80k is cheap. Below $50k is deep value.

That’s the chance to get on the train. While it is stationary. Getting on now is like trying to jump on a moving Shinkansen. Just understand that next year everyone else will be getting off and puking on the platform as you try to board…

If you really want to get started now, it’s ok, but go slow. Average in and prepare for the next bear market to really deploy capital.

And stick to Bitcoin. Don’t become some gambler’s exit liquidity.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.