As I type, the Nikkei 225 index is over ¥44,000 after closing on 10 September at a fresh all-time high. Do you think this market looks tired?

It’s a great feeling as I know that many readers are invested in Japanese companies, whether by picking stocks or simply buying the index.

For those who feel they don’t have enough exposure, where do the opportunities lie? Is it a little late, or does this bull have longer to run?

Why own Japanese stocks?

There are many reasons to own Japanese stocks. Not least, the fact that the Tokyo Stock Exchange’s campaign to pressure/shame companies trading below book value to improve their P/B ratio is paying dividends – literally! Corporate governance has improved significantly and share buybacks have been another major market catalyst.

Personally, I have been accumulating Japanese stocks for the last few years for three main reasons:

- As a long-term Japan resident, I have a future base currency need in JPY

- With the yen so weak, I have been less inclined to convert JPY to buy overseas stocks

- With inflation at around 3%, plus the effects of currency debasement, stocks that pay solid dividends are a massive improvement on cash in the bank

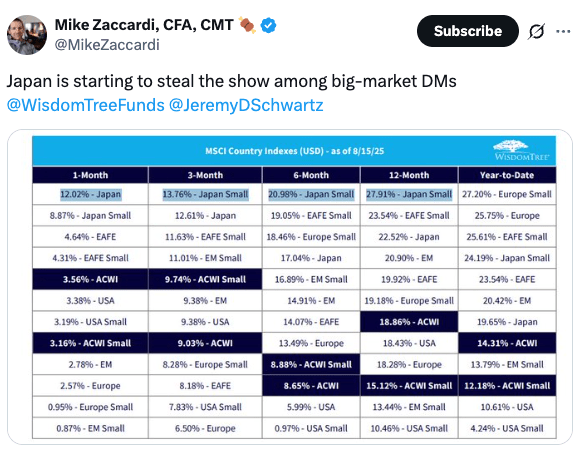

Money is flowing into Japan from overseas due to the powerful combination of the weak yen and a booming stock market. Japan is hot right now!

As ever, the long-term economic situation here is cause for concern. High debt, rising long-term yields, and poor demographics. The problems are well-known. Investing in Japan from overseas still carries that ‘picking up dimes in front of a bulldozer’ kind of vibe. The big boys like Warren Buffett, of course, are borrowing cheaply in yen and collecting dividends above their borrowing cost. They can stomach some volatility. However, for an individual planning to spend their money outside Japan, the currency risk is a genuine concern.

Of all the things that might derail this bull market, the Prime Minister quitting doesn’t seem to be an issue! That’s good to know, given the revolving door nature of that role.

Buy the index or pick stocks?

For most people, buying the Nikkei 225 index is the best advice. I also like the JPX Nikkei 400 index for more investor-focused companies. You may remember that 1489 High Dividend is a favourite of mine, and I also like the 1624 Machinery ETF.

Along with these ETFs, I like to pick a few stocks. Owning the index is great, but you are missing out on a lot of golden opportunities and can get dragged down by large caps struggling with global issues, such as US tariffs. Smaller-cap value stocks are outperforming the indices and generally come with a lower volatility profile.

I’m no securities analyst, and I’m well aware of the fact that we are in a bull market. You could pretty much throw darts at the Nikkei Shinbun and make money over the last 3 years. That won’t last forever. Keep that in mind if you are just getting into this market.

I maintain a Japan Stocks list on X. There are some excellent accounts in there doing valuable work. Try to use it as a source of ideas for research rather than just aping into whatever they write up. (although we’ve all done that!)

I love this Trading View list of cash-rich stocks – that’s been a great hunting ground for me. I also like this list from Simply Wall Street: Japanese net-cash stocks with a growth track record.

A little googling turned up a couple of Japan market outlooks that are worth a read, one from a Japanese asset manager and the other from an overseas manager:

Sumitomo Mitsui DS Asset Management

JP Morgan Asset Management (from May 2025)

The Federal Reserve and Bank of Japan both meet next week, with the Fed expected to cut rates and the BOJ, well… who knows what the BOJ will do, but there’s a chance they could hike. That could affect USD/JPY, although I’m in the camp that longer-term rates will be the drivers of currency moves over time. A sudden stock market correction is always a possibility, and those dips offer buying opportunities.

In summary:

- Japanese stocks are hot; be aware that we are pushing all-time highs

- Dividends alone are a good reason to own Japanese stocks

- Think about your base currency before making decisions

- A combination of index funds and individual stocks is a good approach, but if you are not sure, stick to the index

- US stocks will start to look more attractive from a Japanese resident’s perspective if the yen strengthens over the next few months

- Keeping a little dry powder to buy dips is always a good strategy

- Don’t worry too much about politics!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.