So, here we are. Overnight, the Federal Reserve announced a rate cut of 50bps, the first cut in four years. Projections imply a further 50bps later this year and another 100 bps in 2025. Welcome to the rate cut cycle.

US markets reacted cautiously, with stocks rising ahead of the announcement only to give back those gains and close down slightly. 50bps is considered a big initial cut, so it will be interesting to see how markets behave over the next few days as they digest the news.

Surprisingly, the yen fell against the dollar to the upper ¥143 range and Japanese stocks were up strongly this morning. Again, time will tell if the initial reaction is the correct one.

The macro gurus will no doubt be fighting it out as to whether the US economy is coming in for the much-vaunted soft landing or heading for recession. Jerome Powell sounded upbeat on America’s economic prospects and made clear that he views the larger cut as a move to prevent the Fed from falling behind.

We will find out in due course.

Sometimes the most obvious take is the correct one: rate cuts are generally bullish for risk assets over time, although we may need to ride out some volatility in the short term. The doomers will keep dooming but optimists make more money in the long run:

“Bulls make more than bears, so if anything being an optimist about life and about things in general is a great attribute as an investor. You just can’t be starry-eyed and naive.” — Stanley Druckenmiller

Deja vu

Three assets that are a hot topic in this new environment are gold, silver and bitcoin. It’s funny because I remember these three getting a lot of attention four years ago. Granted, the post-Covid crash environment in 2020 was very different from today – for a start, the Fed funds rate was already at zero in September 2020. However, it’s interesting how things move in cycles. Gold is around all-time highs now and silver enthusiasts are clamouring for a breakout. It has a strong 2020 feel to me, so I thought I would take a look back and see what happened four years ago.

Observe the five-year charts:

As you can see, both gold and silver reacted quickly to the stimulus injection that followed the March 2020 Covid shock. Liquidity is generally good for hard assets. Bitcoin took longer to catch alight but when it did, the fireworks were spectacular as it took out the previous all-time high of $20k and then marched right on to $60k and then $69k in 2021. That move started at $6k at the end of March 2020 and BTC was still only $11k on 19 September 2020.

I like all three of these assets in the current environment, but I like one much more than the others.

Game time soon, anon.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

As another quarter rolls around, it’s that time again. Yes, the main event this week is, of course, the Nvidia Corp (NVDA) earnings report. Once more, expectations are sky-high and, if the chipmaker fails to meet them, the market mood could sour in a hurry. We find out if the AI bull market narrative remains intact on Wednesday night.

Q1 revenue was a whopping $26 billion with guidance of $28 billion for Q2. Wall Street is expecting even more than that with the average analyst estimate coming in around $28.6 billion. Questions have been asked of this company before – can it deliver again?

US tech stocks are trading warily ahead of the report but the Dow Jones Industrial Average managed to put in another record-high close on 26 August.

In Japan, a Nikkei report says that Resonac Holdings Corp (4004) will make a ¥30 billion investment to improve the performance of power semiconductors used in electric vehicles and other devices. This follows the announcement in early July that Resonac will form a consortium with nine other Japanese and US firms to collaborate on the development of semiconductor technologies for generative AI.

Shares in IOT service developer Future Innovation Group Inc. (4392) went limit up today. The jump follows an announcement that FIG’s subsidiary Realize’s transport robot will be deployed in a semiconductor factory run by Rapidus. Rapidus is working on the domestic production of cutting-edge logic semiconductors.

Online banks are picking up customers

The Nikkei also reported today that online banks have doubled their total number of accounts over the last five years. The six major online banks now boast over 40 million accounts as of the end of March 2024, up 13% from the previous fiscal year. The net banks are taking on traditional banks by linking up with point-based ecosystems and smartphone payments and are also providing systems to external companies.

Rakuten Bank Ltd (5838) and SBI Sumishin Net Bank Ltd (7163) gained +5.2% and +5.3% respectively today on the news.

Selling megabank shares to buy net banks could be an interesting trade. However, investors need to keep in mind that rising interest rates and increased competition could slow the growth of the online banks, particularly those that are reliant on low-interest home loans.

Meanwhile, Paypal’s Solana-based stablecoin, PayPal USD (PYUSD) reached a $1 billion market cap just 383 days after its launch, making it the sixth-largest stablecoin.

In other business

If semiconductors and online banks are too flashy for your risk profile, take note that purveyor of high fashion (ok, I jest), Shimamura Co Ltd (8227) reported a 5.5% increase in same-store sales for August compared to the same month last year. This marks 10 consecutive months in which sales have beaten the previous year’s results. Shimamura’s five-year chart isn’t too shabby and it pays a 2.4% dividend. Money in the bank!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

I hope you are enjoying Obon and the summer holiday. After a market crash and a Nankai Trough earthquake warning, things feel a little calmer this week. Hopefully, there won’t be any more ‘big events’ in August other than the local matsuri.

However, September is approaching and it feels like that will be the time to get locked in and focused. So here are a few thoughts as we speed into the last four months of the year!

US markets

There is a slew of economic data coming out of America this week, with the Producer Price Index (PPI) coming in a little softer than expected last night. CPI is tonight and another soft print will heighten expectations of a Fed rate cut in September. Toys will be thrown if Chair Powell does not deliver, but I’m also becoming a little more cautious about the outlook for stocks if he does go ahead and cut. History favours a recession scenario at the end of a hiking cycle. A lot of effort has gone into the soft landing narrative, so we should be on our guard. No reason to make adjustments to long-term investments but things rarely go as smoothly as the crowd expects.

That said, the completion of the US election will remove a lot of uncertainty, regardless of who wins.

Yen / Japan stocks

After starting August with a bang, the Bank of Japan has swiftly backed down from any plan to raise rates again this year. They got as far as 0.25% and the stock market melted down. They didn’t even get to the bond market jitters part of the project. I would love to hear from anyone who can explain how the BOJ will go about a meaningful tightening from here. Imagine what rates at 0.5% would look like. How about 1%?

I just saw a Bloomberg headline that said that PM Kishida is stepping down in favour of a leader who is supportive of the central bank’s efforts to normalise policy. Best of luck to whoever picks up that poison chalice!

Let’s just call BS, shall we? You can’t normalise a ponzi.

Nonetheless, if the Fed does begin to cut, the yen should strengthen. I don’t know how far it will get. 130? 120? 100? It doesn’t matter, because once that cycle is over it is only going the other way. You can save the bond market or the currency and no one is sacrificing the bond market.

I have said it before but I’m nothing if not a broken record: if you are going to spend your future money outside of Japan, you should forget about those alluringly cheap Japanese value stocks and get your money out of yen and into your base currency while you have the opportunity.

If you are here for the long haul, by all means, have at it. In the shorter term, Japanese stocks should do ok and I would even be tempted to look for names that will benefit from a stronger yen. Exporters that did well under the weak yen don’t seem such a great idea going forward.

Getting hard

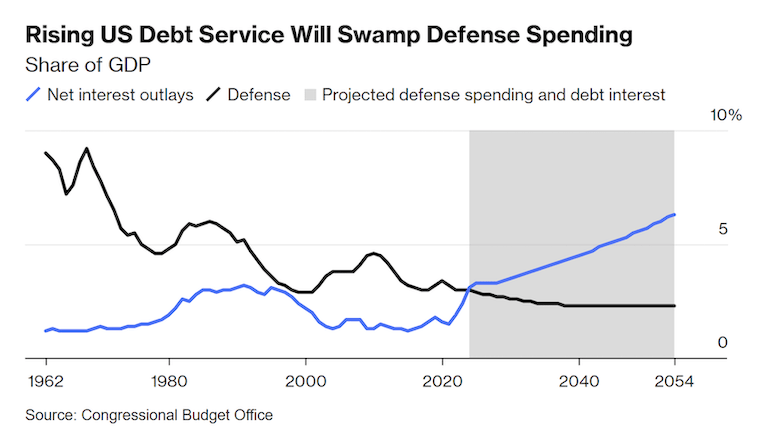

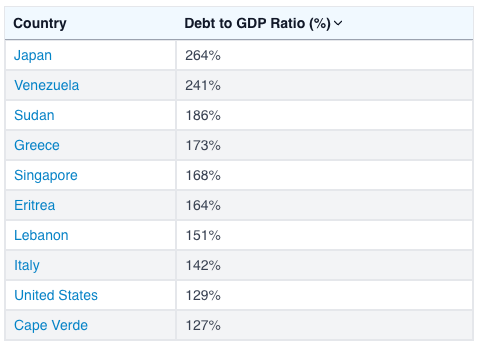

With the US election looming, the cynical among us would be watching out for a liquidity boost to pump up the US stock market. Rather than the Fed, we should probably be looking at the treasury to provide the liquid refreshment. This ‘Bad Gurl Yellen’ piece by Arthur Hayes goes deep into the fountain of liquidity that is about to spring forth. In short, the treasury needs to lower the debt-to-GDP ratio, and it will do so by issuing yet more debt.

The Congressional Budget Office projects that interest payments on America’s debt will total $892 billion in fiscal 2024 and rise significantly in the next decade.

If you are wondering what that looks like, get a load of this chart:

Tell me you’re gonna print more money without saying you’re gonna print more money…

I wrote about currency debasement and and how to protect yourself in Harden up your assets! If you are looking at stocks to plough your hard-earned money into right now, that’s one way to do it but maybe there is a better option.

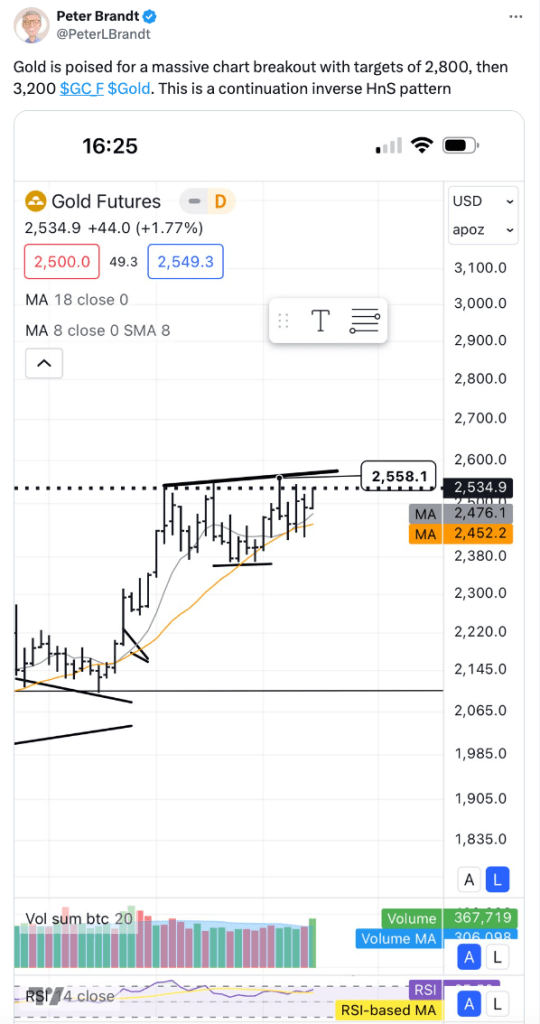

As you can see, some technical traders are getting excited about gold. JP Morgan agrees, arguing that the structural bull market remains intact and forecasting an average price of $2,500 in Q4 and $2,600 in 2025. Geopolitical tensions, rate cut expectations, central bank buying and ETF flows all point to elevated gold prices – report here.

Of course, those are short-term targets and the real point of owning gold is to protect against currency debasement over time. Remember, this is what you’re up against:

Digital gold

Ever the broken record, allow me to point out once more that the boring phase of the Bitcoin bull market is drawing to a close. We probably bounce around for a few more weeks, maybe even a couple of months. The timing is difficult to predict but I expect significantly higher prices by the end of the year. And more to come in 2025. If you are thinking of getting on the train, you don’t have long left…

Despite a reshuffle of the Democratic nominee, pretty much everything I wrote in the Bitcoin bull market update still stands. All aboard!

If you are still trying to get your head around the hardest asset on the planet, the presentations from Michael Saylor’s keynotes are a great resource.

Don’t say I didn’t warn you!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

The haters said I couldn’t do it. And they were right. Honestly, great call by the haters.

Stairs up, elevator down.

If you have been diligently investing in stocks these last few years, especially Japanese stocks, you are probably not feeling too great right now. You are probably feeling a little sick in the stomach. And maybe a bit stupid. I’m here to tell you it’s alright to feel bad for a while but don’t beat yourself up too much. Nobody saw a crash like this coming. Hell, the day the BOJ raised rates, the market went up! Don’t listen to the smart-asses who tell you they knew this would happen and traded it perfectly – most of them didn’t even have any skin in the game.

However, if you are going to take a beating in the markets, you better learn something from it. Otherwise, it really was all for nothing. Welcome to the Hansei-kai.

The Google translation is kind of cute. Whenever I hear this word actually used, it’s more like: ‘We screwed up, now we have to examine why and drown our sorrows’. Maybe it’s just the company I keep!

The purpose of this post is not to bore you with another deep-dive analysis of the unwinding of the yen carry trade. You have probably had enough of that already and there are people more qualified to talk about it than me. The idea is to try and learn something from the experience that will be helpful in the future.

There are always signs!

I haven’t lost my shirt in this crash and I hope you haven’t either. However, I was sitting on some rather profitable satellite positions, mostly in Japanese stocks, and I was thinking about selling some of them. I know this because I wrote about it just six weeks ago in Are we shaking?

What’s worse, I had figured out that if anything was going to derail the Japanese equity bull market, it would be the Bank of Japan. I know this because I wrote about it in January: 2024 – Here goes nothing!

The call was coming from inside the house!

Aren’t I the clever one! I had it all figured out and I didn’t sell.

I am a regular viewer of the Nikkei News Next program on BS TV Tokyo. These last few months, I couldn’t shake this nagging impression of hubris as the presenters and guests lauded the performance of the Japanese stock market and talked about the prospects of the BOJ raising rates like it would be just another positive. Don’t get me wrong, it’s a serious news program asking the right questions, but my feeling was that they were a little too caught up in the hype.

And I didn’t sell!

Ok, ok. I said we weren’t going to beat ourselves up. But you get the picture. The signs were there. And of course, they are a hundred times more obvious in hindsight. I’m not even that mad at myself. I never had any intention of touching my core investments and I have dry powder at the ready to allocate once the panic subsides. My point is that if your gut is telling you something, maybe you should listen to it.

Sell euphoria. Sell euphoria. Sell euphoria. I’m not going to get the tattoo but it has been imprinted on my brain.

What happens next?

After the Hansei-kai, it’s time to move forward. It’s still a little early for me to think about how to allocate money. US futures are down bad and it’s probably going to be a long week. I don’t feel the need to dive in immediately and any stocks I buy will be with a minimum 5-year timeframe. I’m a lot better at buying fear than I am at selling euphoria!

So, more on that at a later date. For now, go easy on yourself, learn the lessons and get ready to step up to the next level.

And f**k the BOJ lol!!!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s the 1st of August. The two big central bank decisions are behind us and summer is in full swing. So what comes next? Where will markets be at the end of this year? Nobody knows the answer to that question but I can almost guarantee you one thing: there is turbulence ahead.

Just like Japanese summer, the volatility already got started in July. However, we seem to have entered a new phase and central banks are the main drivers of the momentum shift.

Having hiked rates to levels unseen in 15 years, there is little doubt that the BOJ has entered a tightening cycle. Governor Ueda did not rule out another hike this year and the yen responded quickly to his comments, rising to 150 against the dollar. Today it is trading at around 149. Weston Nakamura sees 152 as the most important price level in global macro right now and we are already well beyond it.

Japanese stocks reacted positively to yesterday’s decision, pumping across the board. However, the Nikkei 225 index slumped -2.5% today as exporters felt the pinch of a stronger yen.

US tech investors rotate into small caps

In the US, Fed chair Powell left rates unchanged while hinting that he is getting closer to a cut. The market fully expects this to happen in September and there will be visible disappointment in people’s brokerage accounts if it doesn’t. Volatility is already rearing its head. Tech stocks have sold off over the past month amid fears that the AI bubble might be bursting. Nvidia has been trending down from its 6 June high of $140.76 and a -7% dump on 29 July seemed ominous, but last night it pumped +12.7% after AMD’s better-than-expected earnings release. Go figure…

Hats off to strategist Tom Lee for calling the rotation into small caps. IWM has been the main beneficiary of the tech selloff.

The crypto coaster rolls on

Not to be outdone by chipmakers, crypto remains unpredictable over short time frames. At the Bitcoin conference in Nashville last week, none other than Donald Trump showed up to play to the crowd. His list of “promises” included: keeping the Bitcoin the US government has seized as a strategic reserve, (yes, wow!) firing Gary Gensler on day 1, ending the democrat’s war on crypto and making the US a leader in mining.

The air quotes around “promises” don’t need much explanation. Trump has zero interest in crypto and is plainly exploiting the dem’s antagonistic stance toward the industry for votes. But don’t let that distract you from the bigger picture: governments are examining Bitcoin as a strategic hedge against their own money-printing excess. The fact that this conversation is even happening is remarkable. Bitcoin game theory is going to get very interesting in the months and years ahead.

Trump to the Bitcoin Bros: “Have a good time with your Bitcoin and your Crypto and everything else you’re playing with.”pic.twitter.com/9Mf1zr1mGX

Bitcoin is back in the $64,000 range today, as it appears that the Biden/Harris camp may be selling off the reserve that Trump promised to keep. It’s never boring. See my Bitcoin bull market update for more.

Meanwhile, investors in Japan received a lesson in FOMO from Bitcoin proxy Metaplanet Inc. this week. Shares went on a tear after the company announced its Bitcoin treasury strategy in April and many people piled in late. Now the stock is coming back down to earth with a bang as the excitement wears off. Shares are down over -70% from their 24 July high and the move down doesn’t look done yet. Of course, every man and his dog wanted the stock when it was skyrocketing and nobody is interested now. There’s a clear lesson there. That said, I wouldn’t be surprised if Metaplanet makes another run if/when Bitcoin makes a decisive break above its previous all-time high and enters the parabolic phase of the cycle. Timing is everything in narrative-driven trades.

So, what to do?

I have noticed an uptick in clients trying to position and trade some of these macro moves, particularly the USD/JPY angle. The problem with access to unlimited information, content and opinion is the urge to react to it and do something. So here’s my two cents:

The summer, and perhaps the rest of the year, will see some turbulence. Volatility goes both up and down. Overall, the backdrop keeps me optimistic. Rate cuts in the US are coming – it’s just a question of when. As things currently stand, it would not be a panic cut, which is constructive for risk assets. US stocks, gold and crypto should react accordingly. Regardless of who wins, the US election will remove a lot of uncertainty. If you are broadly diversified, you could do a lot worse than fastening your seatbelt and taking a nap for a while.

If the BOJ is tightening and the Fed is loosening, the yen should continue to strengthen. This is going to put some strain on export-related Japanese stocks and the market as a whole looks more unpredictable than the US. Governor Ueda said he doesn’t think the rate hike will damage the Japanese economy. He’s probably right for now, but let’s see what kind of toll a series of hikes will take. The last time the BOJ tried to hike was 2007/2008 and that move was reversed in a hurry…

If you have been waiting for your chance to escape JPY and get into your base currency, that window is opening. Don’t miss it – long term it does not look good for the yen.

Stay hydrated folks!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

After showing signs of wobbling the last few weeks, US markets slumped on 24 July with big tech shares leading the move down. Tesla Inc (TSLA) fell -12.3% after a Q2 earnings miss while Alphabet Inc (GOOGL) dropped -5% despite beating earnings expectations. That was enough to trigger an avalanche and the NASDAQ ended -3.6% lower and the S&P 500 endured its worst day since 15 December 2022, falling -2.2%.

Correction territory

Japanese shares followed the US market down, with the Nikkei 225 index falling -3.3% today as exporters laboured under a strengthening yen. The benchmark index peaked on 11 July at ¥42,426 and has trended downwards since then. It turns out that I wasn’t imagining things when I asked Are we shaking? at the end of June.

Investors will now be wondering if this is simply a healthy correction after a big run-up or the start of a larger move downwards. It is too early to begin talking about a bear market but we are certainly in correction territory. A correction is defined as a fall of -10% from a recent high and the Nikkei closed today down -10.7% from the 11 July peak.

At 3pm today, USD/JPY was trading at ¥152.7. The current rebound in the yen is being driven by expectations that the Bank of Japan will raise rates at its policy meeting next week. In addition, the US Federal Reserve appears to be moving in the direction of rate cuts starting in September. A sustained sell-off in stocks may well need confirmation of rate cuts in order to stabilise.

Semiconductor stocks fall hard, Lawson delisted

Semiconductor-related stocks are bearing the brunt of the current selloff with Disco Corporation (6146) falling for seven straight days. Disco fell a further -4% today to close at ¥46,850, well off its peak of ¥68,850 set on 11 July.

In other news, convenience store operator Lawson Inc. was delisted from the TSE on 24 July following a successful tender offer from KDDI Corp. KDDI will partner with Lawson’s parent company, Mitsubishi Corp to take the company private.

A stock to watch

Crypto followed the trend in traditional markets with Bitcoin falling to around the $64,200 mark. Ethereum is down around -8% despite the successful launch of the Ethereum ETFs in the US on 23 July.

Meanwhile, Japanese Bitcoin proxy Metaplanet Inc. (3350) has been on a wild ride. The stock has risen more than +1,100% since the company announced its Bitcoin treasury strategy in early April. However, the FOMO really kicked in this week with shares accelerating to ¥300 on 24 July. Metaplanet is back trading around ¥220 today but is still a stock to watch as investors try to front-run the potential decisive break of Bitcoin’s all-time high in the coming months.

It seems likely that traders view Metaplanet as a tax-efficient way to gain exposure to Bitcoin price moves. Crypto in Japan is taxed as miscellaneous income, whereas stocks are taxed as capital gains.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

It’s pretty incredible that the US Federal Reserve has gone through a 27-month hiking cycle and US stock markets are at all-time highs. Unless you’ve been living under a rock during this time, you are probably aware that the main growth driver has been the intense hype surrounding artificial intelligence (AI) and more specifically, generative AI.

What is AI?

The Encyclopedia Britannica defines AI as ‘the ability of a digital computer or a computer-controlled robot to perform tasks commonly associated with intelligent beings’. The US company Nvidia says AI is ‘the capability of a computer program or a machine to think and learn and take actions without being explicitly encoded with commands’.

In March 2023, Bill Gates published a blog post titled ‘The Age of AI has begun’. In it, he says: ‘The development of AI is as fundamental as the creation of the microprocessor, the personal computer, the Internet, and the mobile phone. It will change the way people work, learn, travel, get health care, and communicate with each other. Entire industries will reorient around it. Businesses will distinguish themselves by how well they use it.

Technological revolution or a waste of resources?

I read a couple of interesting threads about AI last week. The first one by David Mattin considers the recent UK election as the last ‘pre-AI’ election we will hold. He sees a world entering a period of deep economic transformation that will change how we live and work and accelerate the process of scientific discovery. Rather depressingly, he expects this transformation to split society into two camps: enthusiasts/accelerationists, who want to lean into this new technology and sceptics/decelerationists, who want to resist the incursion of technology into daily life. This split is not hard to imagine when you look at how divided the Western world has been on almost every issue of late.

The second thread, by Ed Zitron, summarises a recent Goldman Sachs report on generative AI, which brutally dismisses Chat-GPT and its ilk as unreliable and power-hungry. The report concludes that generative AI is unprofitable, unsustainable and fundamentally limited. Moreover, the huge surge in AI-related stocks is a bubble that will soon burst. Original report here.

I don’t think my opinion on the first part is worth much, but I am not really interested in taking sides. There are clearly opportunities for massive positive change and there are also equally glaring risks. In a perfect world, these would be balanced sensibly but that world doesn’t exist. Things are about to get interesting…

As far as generative AI goes, time will tell. I think the most common complaint people have is that they don’t want gen-AI to write stories, produce art and know everything. They want it to do all the boring jobs that we humans don’t want to do and free us up to be more creative.

Investing in AI

From an investment standpoint, I don’t think AI can be ignored. It seems imprudent to dismiss the whole field as a bubble. However, if some parts of the industry are in a bubble, the key question is how long can the bubble continue inflating? As George Soros has pointed out, there is a lot of money to be made by rushing into a bubble. The tricky part is getting out before it bursts.

There are relatively few pure-play AI stocks to invest in. However, many great companies are using AI technology and making investments in AI. I have picked up a few below that I think are worth watching. This is neither an exhaustive list nor a recommendation to invest. Just some ideas to get you started so you can do your own research. (performance is quoted up to 15 July 2024)

Nvidia Corp (NVDA) and Super Micro Computer Inc (SMCI)

If I asked you what the best-performing AI-related stock is over the past 12 months, you could be forgiven for answering Nvidia. However, Nvidia has actually been beaten by a company it is partnered with – Super Micro.

The Motley Fool did a nice write-up on these two companies here: Essentially, they aren’t really competitors, they complement each other. NVDA designs graphics processing units (GPUs) which, among other things, are used for AI model training. SMCI designs servers and it takes Nvidia’s GPUs and other components to make them and sell them to its clients. These are what some people refer to as ‘pick and shovel’ investments in AI.

Of all the big-name tech companies, Microsoft is perhaps the most bullish on AI. The company is accelerating its own AI commitments and has invested some $13 billion in OpenAI in a partnership that dates back to 2019. Microsoft has integrated all of its generative AI assistants into a single AI product named Microsoft Copilot. Copilot offers both free and paid versions and is integrated into a wide range of Microsoft applications providing access to Chat GPT-4 and DALL-E 3.

Investors can keep up with Microsoft’s AI developments here.

Shares are up +21.2% in 2024 so far.

Arm Holdings ADR (ARM)and Softbank Group Corp (9984)

Majority owned by Softbank Group, Arm Holdings was listed on the NASDAQ in September 2023 and has quickly established itself as a major force in AI. The company architects, develops and licenses central processing unit (CPU) products and related technology which semiconductor companies and original equipment manufacturers (OEMs) rely on to develop their products. 99% of smartphones run on Arm-based processors and Arm has shipped 287 billion chips to date.

In Q4 of fiscal 2024, Arm reported its highest-ever revenue of $928 million, up 47% year-on-year. Shares are up +216.5% since listing and +136.3% year-to-date.

Softbank Group has had its ups and downs but is recovering in 2024. Led by the charismatic and controversial Masayoshi Son, Softbank Group has aggressively invested in a broad range of fields including robotics, AI, real estate, e-commerce, telecoms and more. It would be fair to say that the company has backed more than its fair share of losers, but Arm is proving to be one of its better bets.

AI stands at the forefront of Softbank Group’s vision and strategy so investors should expect the heavy investment in AI-related companies to continue. CEO Masayoshi Son says: ‘We are heading for an AI revolution, and we will be the investment company for the AI revolution’.

Softbank Group shares are up +81.1 % so far in 2024.

These are just a few ideas to get you started. There are many more companies involved in AI that are worth considering. Both Amazon and Meta are making huge investments in AI. Arista Networks (ANET) AI networking has driven impressive returns over the past five years. In Japan, NEC Corp is developing a range of AI technologies under the banner of ‘NEC the Wise’. And, of course, the huge boom in semiconductors has largely been driven by demand from AI.

The majority of investors will already have a larger allocation to AI-related stocks than they probably realise. Any S&P 500 or NASDAQ tracker will have significant exposure, so it isn’t always necessary to make an effort to dig out the next big name.

As for timing, returns over the last 3 years have been extraordinary. It remains to be seen if this is a bubble that is soon to burst, but sudden deep corrections can occur at any time. If you are a long-term believer in the AI narrative, there is no rush to pile money into the space in one go. Dollar-cost averaging is a solid strategy, and so is adding on significant dips.

Whether you are allocating passively or building a portfolio of AI satellite holdings, things are going to get interesting and maybe just a little weird.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

The all-time highs keep coming. On Monday 9 July, the Nikkei 225 index made its highest ever close at ¥41,580.17. Semiconductor-related stocks led the way, while other notable movers included Hitachi Ltd (6501) and Fujikura Ltd (5803).

Not to be outdone, the S&P 500 and NASDAQ Composite also closed at record highs on 9 July. Gains were heavily weighted to big tech stocks as the AI narrative continues to drive market sentiment. Fed Chair Jerome Powell stuck to the script during his first day of testimony, reiterating that the Fed’s objective is to cool the economy and progress towards the 2% inflation target without cooling it too much. Market consensus continues to favour a soft landing scenario, with one or two rate cuts expected later this year. CPI data is due on Thursday and if that comes in line with expectations, the positive mood should continue.

Meanwhile, Tesla Inc (TSLA) continued its rebound, closing higher for the 10th consecutive day.

Japan’s real wages fall again, BOJ discussing cuts in bond purchases

Despite the good times in the stock market, much of Japan’s economy still looks relatively weak. Real wages fell by 1.4% in May, marking a record 26th month in decline. Wages are actually rising at the fastest pace in 31 years, but the increases are being offset by inflation, meaning households have less purchasing power.

USD/JPY is trading around ¥161.47 with no end to yen weakness in sight.

This week sees the Bank of Japan meeting with major market players to discuss the tapering of the central bank’s bond purchases. Some market participants are calling on the BOJ to cut bond purchases in half while others favour a more gradual reduction. The final plan is expected to be revealed at the BOJ’s end-of-July meeting.

Semiconductor shares remain strong, Hitachi and Fujikura impress

Chip stocks are once more powering ahead with Advantest Corp (6857) and Tokyo Electron Ltd (8035) gaining +4.1% and +3.8% respectively on 9 July. Chip materials maker Resonac Holdings Corp (4004) announced that it will form a consortium with nine other Japanese and US firms to collaborate on the development of semiconductor technologies for generative AI. Resonac shares surged +8.7% on the news.

Hitachi shares jumped +5.2% on reports that the company is increasingly focused on improving shareholder returns. On 2 July, the electronics giant provided an update on the progress of its buyback of up to 21 million shares at a cost of up to ¥200 billion. The company is targeting a total return ratio of around 50%, including dividends and buybacks – that would be on an expected net profit of 600 billion this fiscal year. Hitachi shares are up +89% year-to-date.

Another big mover was Fujikura Ltd, which jumped +11.4% on 9 July. Fujikura is an electrical equipment manufacturer that develops a range of telecommunication system products, including devices for optical fibres. It appears that Fujikura’s surge was spurred by a 12% move by Corning Inc (GLW) on 8 July after the company revised its sales forecast upward. Fujikura gained a little more today and is now up +228% in 2024.

Japanese stocks rose again today with the Nikkei 225 closing at another record high of ¥41,831.99. Financial stocks were up again on hopes that higher interest rates would bring improved profits. Mitsubishi UFJ Financial Group (8306) has gained over +8% in the past month and almost +50% year-to-date.

Bitcoin also bounced back from its current correction somewhat, moving from around $57,000 to $59,000 despite an increase in market supply from Mt Gox and the German government. Bitcoin ETF flows were positive again and traders eagerly await the SEC decision on Ethereum ETFs.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Being a financial planner by trade, I try to organise our financial future as efficiently as possible without going overboard. My wife and I both work and we have a reasonable income. We have a plan, we know what our numbers are for later in life and the big events in between. Most of all, we are flexible in that plan – our core investments are set and forget, but they can be adjusted easily. The tactical stuff is fun for me and I see it as a bit of a challenge.

Of course, things can go wrong: ill health, accidents, economic change and shifts in specific industries. You prepare for these as best you can and get on with living. Eat well, exercise, look both ways crossing the street, buy insurance etc. etc.

However, there are a few bigger things that bother me. I don’t think about them all the time, but they lurk in the back of my mind. For example, I don’t think AI is going to take over my job, but it could change the world considerably – gotta keep up with developments there. I could classify these things as outliers and conspiracies. Some may or may not have a meaningful impact and others feel a little ‘out there’. The best conspiracy theories have an element of truth, though, don’t they?

So, here are a few things I think about and how they relate to money, investing and how big your number should be:

Climate

I must confess, I don’t allow myself to dwell on what we are doing to the planet. We are clearly having an adverse impact and most of the damage is being done by big business interests who will not stop. The paper straws are cute, but they are hardly going to offset the widespread burning of fossil fuels and other environmental destruction. It’s not that I don’t think it’s important – it’s crucial to our survival as a species. I just know there isn’t much I can do about it. I separate our garbage, cut down on plastic and try not to waste resources, but I’m not losing sleep. Half the people in the developed world don’t even believe climate change exists so good luck to us coming together and taking action as a species. Do you remember the Covid mask and vaccine debates?

It is certainly getting hotter though! And it’s hotter for longer than it was before. After 27 years in Japan, it’s noticeable how spring and autumn are shrinking while summer gets longer year by year. What’s that going to be like in 10 years? How about 20?

I hardly think Yokohama will become unlivable in our lifetime but it could become pretty unpleasant. Imagine Japanese summer from April to October! Would that change your planning? Could it mean your ‘number’ needs to be bigger? The ability to escape Kanto, and maybe even Japan, for several months a year could become a key lifestyle choice. Maybe some people will want to escape for good. Wouldn’t that mean that the cooler, more livable climates in the world are going to see an influx of people who can afford to move? Parts of India are already hitting 50°C as a matter of course. That kind of temperature is more manageable in the developed world with aircon but doesn’t higher demand for a cool place mean higher prices?

As we move from climate change to climate crisis, how are governments going to address it? Again, remember Covid? It was all the people’s fault that it was spreading. They had to be stopped from travelling and confined to their homes in some countries.

Climate lockdowns anyone? Do you think they won’t do it?

It’s a dark thought, but people with flexibility financially will fare better than those who are struggling for money. Does that change your number?

Japan’s economic decline

Honestly, this one would bother me more if I was younger. I’m not sure Japan is a place I would be trying to build a life, career or business given the demographics and the economic outlook if I was in my twenties. But I’m not that young any more and I’m happy where I am. I would, however, want my kids to have the opportunity to live and work overseas if they choose.

The yen is a major concern though. My view is that short term it should recover somewhat when America begins cutting rates. I can see it getting to ¥130 or even ¥120 in the next year or so. However, longer term I expect the yen to steadily lose ground, particularly against the dollar. I talked about it in my ‘How screwed is the yen?’ post a year and a half ago. Staying alert for opportunities to earn in other currencies, investing in a combination of domestic and overseas assets and accumulating Bitcoin remain priorities for me.

Financial shenanigans

Grab your tinfoil hats for this one! In simple terms, the money has been funny since the 2008 global financial crisis. A lot of institutions that should have died were propped up at the expense of taxpayers and we’ve been getting screwed ever since. Economies and big business have become addicted to liquidity: cheap money, low rates. Low interest rates foster inflation, which is a tax on us all, but especially a tax on people who do not own financial assets.

Countries have too much debt and are not producing enough to pay it back. Japan is perhaps the worst offender, at least in the developed world. The debt spiral is probably terminal. That’s why the yen is doomed, and after that so are the pound, the euro and the dollar. I covered currency debasement in ‘Harden up your assets.’ There are tools to fight it that need to be deployed. Otherwise, your money buys less and less.

This is why governments are getting interested in the idea of Central Bank Digital Currencies. (CBDCs) At some point, they are going to need to perform a reset and substitute the current failing money with an alternative. And the powers that be never want to waste an opportunity to seize more control.

In essence, CBDCs are just another form of fiat money. But they come with a whole new opportunity for manipulation. Here’s an interesting video of Rishi Sunak being asked how he would enforce national service in the UK:

Controlling ‘access to finance’ is a government wet dream and CBDCs will make it easy. If you think that the possibility of losing permanent residence due to unpaid taxes is bad, wait until they freeze your bank account or apply a negative interest rate to your money until you pay up.

The public is sleepwalking into this one. You can already imagine how half the population won’t have any issue with it at all. ‘If you don’t have anything to hide, why would you need to keep your money private?’ will be the refrain. People who are well off have no concept of how less fortunate people can run into money trouble and fall behind on bills and taxes. The rich just don’t want to pay for a bunch of ‘layabouts and immigrants’.

The Bank of Japan already has a page on its website about Central Bank Digital Currency by the way. Cute, huh? No plans to implement it at present, but they are looking into it…

CBDC is one thing I think is really worth fighting against, but it will most likely be a losing battle. Sooner or later some crisis will come along and CBDC will have to be implemented ‘for our protection’. You can already see it happening with the AML/CFT mission creep.

Call me crazy, but I think that accumulating Bitcoin and other crypto is the best we can do to prepare for what is coming. Any money sitting in the fiat system will be caught in the net. In many countries, people who want to withdraw a few thousand dollars in cash already have to explain to the bank what they are planning to do with it.

Assuming the number will go up

So there it is. Like you didn’t have enough to worry about! From a financial planning perspective, my take on this is that whatever your number is, you will probably need more.

That’s to say, whatever amount of money you think will be enough to secure your future, maybe add another 10-20% for safety.

This is why I recommend dividing investments into core/strategic and satellite/tactical. The long-term strategic investments are focused on hitting the number. The tactical assets are aiming for a little extra. The crypto holdings are a shot at f**k you money.

Number go up. Act accordingly.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.

Anyone who has lived in Japan for a while knows the feeling: a faint tremor, something moving in your peripherals, like the train next to yours slowly pulling away and you’re not sure which carriage is moving. You look up at your partner/friend/co-worker…

Are we shaking?

Earthquakes are not always so subtle of course. Sometimes that faint rumble becomes something bigger. And sometimes, it’s just a heavy truck passing by outside.

Did you feel that? Maybe it was just me? Of course, the market is not just one stock but, if you had to pick a name that has driven US markets to new highs this year, it would be Nvidia. Sure, your Apples and your Microsofts have been strong too, but nothing quite like this. And last week we finally saw a hint of weakness. It would hardly be the first dip this year – questions were asked in mid-February and again in mid-April. What we haven’t really seen is a broadening out of the stock rally into other industries. Charlie Bilello points out here that the top 5 holdings in the S&P 500 now make up 27% of the index, the highest concentration since 1980. He also notes here that the index’s P/E ratio moved above 25 last week, the highest level since Q1 2021.

So, the AI hype-driven tech boom (or is it a bubble?) is still the dominant narrative driving the US market. George Soros once said: ‘When I see a bubble forming, I rush to buy, adding fuel to the fire.’ This is precisely what less savvy investors do too. However, they are rarely as clever as Soros when it comes time to take profits and get out.

Pockets of recession

US economic data continues to come in better than expected. Certainly better than small businesses and low-income families are feeling at this point. To wildly misquote one of my favourite writers, William Gibson: ‘Recession is already here – it’s just not evenly distributed.’

This one-hour podcast with James Lavish is worth a listen if you want to get a better understanding of the impending US debt crisis. He talks about how pockets of recession are already forming, they just haven’t spread broadly across the economy yet.

Are Japanese stocks stalling?

Speaking of debt crises, how is Japan doing? USD/JPY is creeping ever closer to the ¥160 level. Rubbing salt into the wound, the US has just put Japan back on the currency manipulator watch list. This could all be solved by the Bank of Japan raising rates in a hurry but it’s the debt that makes that rather difficult. Bad demographics, sky-high debt to GDP and a doomed currency – good thing we choose to live here for the harmony and the mild weather, desho?

After a fantastic run, there are signs that Japanese stocks are stalling too. (are we shaking?) Foreign investors, who played a significant role in driving the market to post-bubble highs, have largely been unloading in the last couple of weeks in the face of lacklustre economic data and persistent yen weakness. The Bank of Japan can no longer be relied on to buy ETFs on down days either. Stocks take the stairs up but they’re known to take the elevator back down…

Meanwhile, the Norinchukin Bank has gotten itself into quite a pickle. The fishers, farmers and foresters cooperative was long US treasuries and, trying to be sensible, it was currency hedged. That meant it endured the two-year rout in US bonds without any of the benefit of the strong dollar when converting holdings back into yen. As a result, it is having to fire sale around $60 billion of its $310 billion in foreign assets and eat the loss. I have preached for some time that currency is the biggest risk most investors don’t know they are taking, but I never considered getting burned like this by being currency hedged – ouch!!!

To sell or not to sell?

This is beginning to sound like a terribly negative post, but it’s really just a reflection of my thoughts about taking some profit and de-risking for a while. Just to be clear here, I am talking about adjusting tactical or satellite holdings. I don’t see any reason to make any changes to my long-term core investments. I own US tech stocks and a range of Japanese stocks in my core portfolio and am happy to keep them. However, I also own some of these same assets tactically – that’s to say I bought them at an opportune time with a shorter time frame in mind. Those are the ones I am getting tempted to sell.

Everyone is a genius in a bull market. You will notice though, that no one wants to tell you when to sell. Except maybe the macro doomers, but they’ve been telling you to sell the whole time markets have been rising, so let’s leave them out of this. For sure, it is smart not to fight the trend, and in US tech and Japanese equities, the trend has been unmistakably upward. There is also the fear of leaving money on the table and looking silly if markets pump after what turned out to be a minor correction.

However, we are talking tactical and that means buy low, sell high. If you are yen base currency and you bought US tech stocks a couple of years ago, not only have you made nice gains in the stocks, but the weak yen has boosted your profits significantly. You could be forgiven for cashing out back to yen and taking the win. The same can be said if you got trapped in yen and instead bought Japanese stocks to counter inflation and the market then went off to the races. That’s a nice win too, but you have to sell before you take the victory lap.

The big question is, supposing you sell, what do you do with the money next? If you are going to spend it on a sports car or a nice holiday, good for you! But if you still have to worry about keeping pace with inflation and currency debasement, you are going to have to find a suitable home for it. Sitting in cash for a few months and then catching a big drop in markets would be ideal, but we are not playing on easy mode here.

These are the thoughts I have on a Monday afternoon with the Nikkei up +0.5% to ¥38,804 and US stock futures looking steady. Perhaps I’ll just sit on this one for a while. Doing nothing is frequently the smartest play, but did you feel that? Maybe we are shaking?

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.