There is still a lot of uncertainty about the the severity and duration of the current coronavirus epidemic, with some health experts predicting it will all be over by April, while others see a large proportion of the global population at risk of infection. When it comes to the effect on markets, it’s logical to take a look the impact of the SARS crisis for guidance. However, it’s important to remember that, not only are we talking about two distinct disease profiles, but we are living in a different world economically from seventeen years ago.

The SARS epidemic, which originated in Guangdong province in China, ran from November 2002 to July 2003. It had a significant, but relatively short term, market and economic impact. The most heavily hit sectors were tourism, retail (particularly luxury), airlines, casino and property. For 2003 GDP growth fell about 1% for China and 2.5% for Hong Kong. Hong Kong’s economy went into recession in April 2003 before recovering substantially.

The MSCI China fell 8.6% on the SARS outbreak, but rebounded by more than 30% in the three months after April 2003. Stocks in Hong Kong fell by a fifth but also came back strongly. Cathay Pacific shares dropped almost 30% from December 2002 to April 2003, before bouncing back to almost double through the next year. In Japan the Nikkei 225 also dropped by almost 6% but was quickly restored once the crisis was deemed over.

The Hong Kong property market was already suffering the after-effects of the Asian financial crisis, and SARS extended the decline by a year or so. Home prices fell by 8% in the first seven months of the SARS epidemic before rebounding for the rest of the year. Conversely the current coronavirus has come along at a high point in the housing cycle.

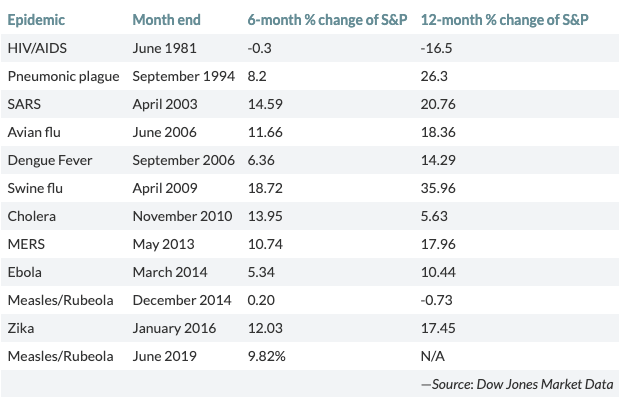

The US stock market tends to shrug off epidemics somewhat easily. The table below, taken from Dow Jones Market Data in this MarketWatch article, shows how the S&P 500 has reacted over 6 months and 12 months in previous outbreaks:

When assessing the likely impact of the current Covid-19 coronavirus, it is important to note some major differences in the Chinese and global economies between now and 2003:

- In 2003 China’s GDP was 4% of the global total. Now it stands at 17%.

- China’s economy was largely manufacturing and trade seventeen years ago, compared to consumption and services / tourism today. Government-imposed bans on travel will hurt more in the current environment. This is a blow to Japan’s inbound tourism boom for example.

- In 2003 the Chinese currency was still pegged to the dollar. Now currency markets are freer, which could mean a weakening of the Yuan.

- The global economy in 2003 was in a much earlier phase of the business cycle and global cooperation in trade was increasing, in contrast to the “trade wars” that have characterised the last 12 months.

- On the other hand, monetary policy in both China and the west is now far more supportive than it was in 2003.

Clearly the economic impact this time around will depend on how long the epidemic lasts and how far it spreads. Countries close to China will obviously be impacted more severely. Typically the effect of a disease outbreak on market confidence can far exceed it’s actual impact. Once things are under control the recovery should be fairly swift, although there are plenty of other factors that could influence markets in the coming months.

Once again, refraining from panic decisions and staying diversified is perhaps the best advice for investors.

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.