Wash your hands, don’t touch your face, and there’s plenty of toilet paper!

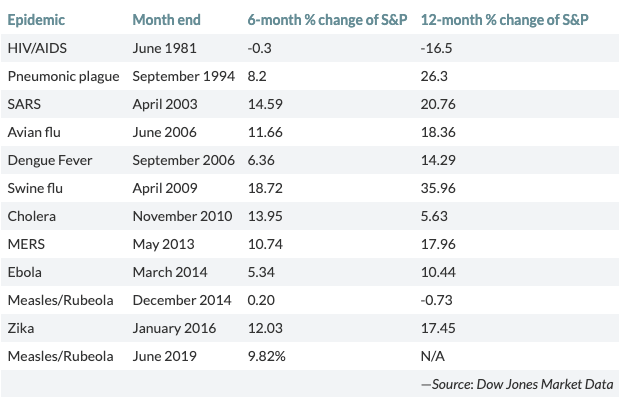

When panic sets in, it’s good to take a step back and focus on the simple things you can do, rather than joining the stampede for the exit. And panic certainly set in last week in global stock markets. You may remember that a correction is defined as a 10% decline in market value. The one last week was one of the fastest ever, and the drop is now approaching 15%. 20% is bear market territory.

Furthermore, it wasn’t just stocks that fell. The 3%+ fall in the gold price on Friday (likely profit taking) shows that being well diversified means having more than one defensive strategy in your portfolio. Even truly diversified portfolios were down between 3% and 8% from their highs last week, depending on risk profile.

Clearly we don’t know where we are heading now in terms of the spread of Covid-19. It seems likely we will see a significant increase in cases worldwide over the next few weeks. However, it is interesting to note that in China, where the virus originated, infection rates are slowing and business is slowly starting to resume. With luck, the rest of the world will follow a similar pattern. If it does, then more market panic followed by a quick recovery is not an unreasonable expectation, particularly as central banks are likely to respond with further easing.

So what should we be doing? I’m certainly not offering trading advice at a time like this but there are certain common sense actions worth considering:

- If you were already well diversified, relax. You were setup correctly and have done the best you can. Perhaps look at rebalancing when the panic dies down.

- Same if you are investing monthly and averaging into the market. You get to buy cheaper this month!

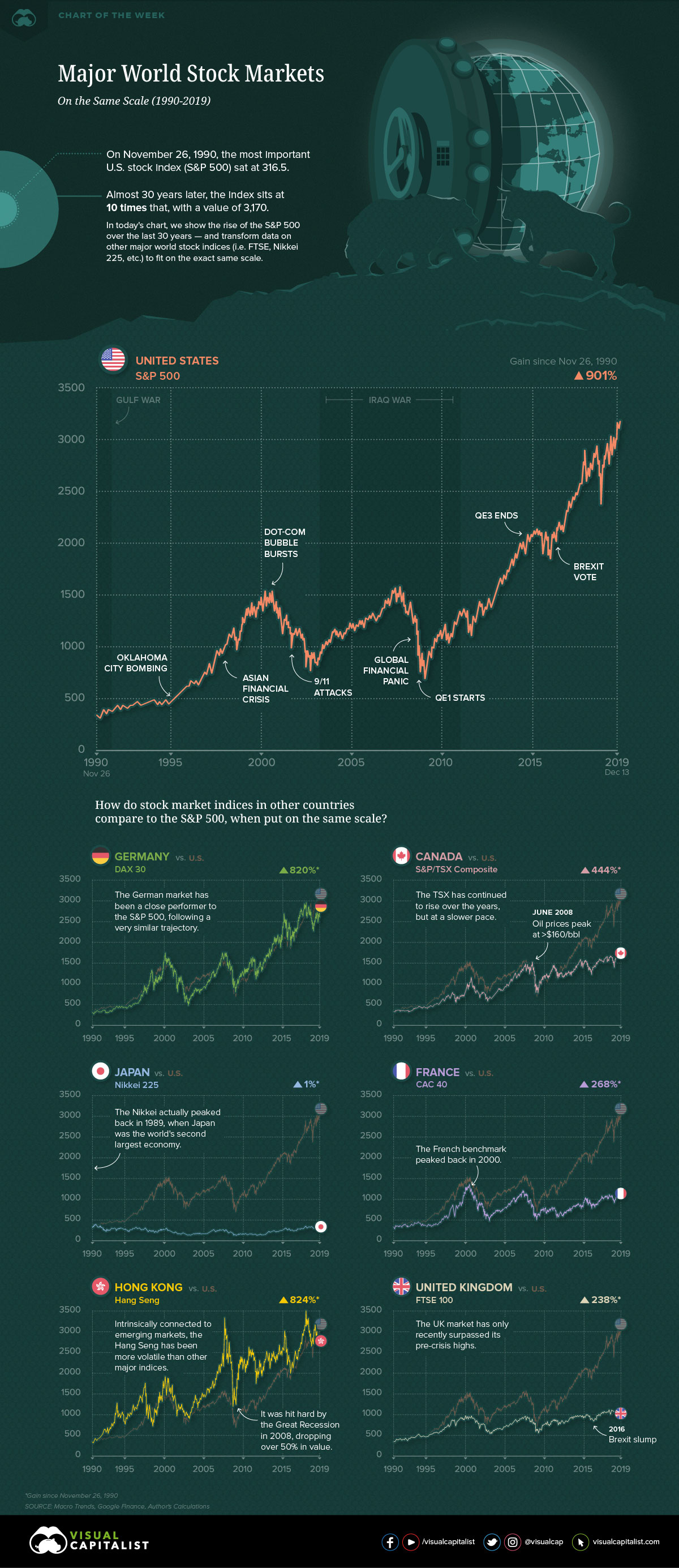

- If you were heavily invested in stocks, how much have you really “lost”? The S&P was near all time highs before last week, so a pullback would not have been out of the ordinary, even without the Covid-19 panic. If you invested capital recently your timing was not good, but do you want to sell into the panic and book the loss? Learn your lesson and move on.

- If you are looking at the current drop as a buying opportunity, good for you. Get your capital into position – if it’s just a simple domestic transfer to your investment account then no problem. If you have to send money overseas it may take a little longer to organise.

- Even pros will struggle to call the bottom. Let the panic subside and buy slowly. Maybe allocate a little each week. Markets could always fall further.

Most of all, look after your health and stay sensible. Without pointing fingers at the reactions in particular countries, I saw footage of hundreds of people lining up, bunched close together, to buy masks. It’s probably not a good time to follow the herd…

And yes, Japan makes its own toilet paper and there are warehouses full of it waiting to be delivered to stores soon!

Disclaimer: This should go without saying, but the information contained in this blog is not investment advice, or an incentive to invest, and should not be considered as such. This is for information only.